Do You Know What Your Home Is Really Worth Today?

Meta Description:

Uncover how much your home may have grown in value. Learn how to calculate equity, tap into it wisely, and make your home work for you.

Introduction

Do you ever wonder, “How much is my house worth right now?” If you haven’t asked yourself that question recently, you’re not alone. Most homeowners don’t get a fresh professional valuation often—yet doing so could uncover hidden value.

Why does it matter? Because your home is likely your largest asset. Over time, it quietly builds wealth—which you might not even realize until you check. Whether you plan to move, borrow, renovate, or simply gain peace of mind, knowing your home’s real worth is a smart move.

In this article, you’ll learn:

-

What home equity is and how to estimate it

-

Why your home probably has more value than you expect

-

What recent market data tells us about equity today

-

Ways you can use your equity as a financial tool

-

Risks, strategies, and next steps for homeowners

Let’s get into it.

What Is Home Equity?

Home equity is the portion of your home you truly “own”—the value that remains after subtracting what you still owe on your mortgage.

The Equity Formula

Home Equity = Current Market Value of Your Home – Outstanding Mortgage Balance

-

Current Market Value: What buyers would pay today

-

Outstanding Mortgage Balance: What you still owe

Example:

If your home is appraised (or estimated) at $500,000, and your remaining mortgage balance is $200,000, then your equity is $300,000.

That’s not just an abstract number. It’s real financial power you’ve built up through time, market growth, and paying down debt.

Why Equity Builds Over Time

Your equity doesn’t stay static. It tends to grow because of:

-

Home price appreciation — your property becomes more valuable over time

-

Mortgage principal reduction — your payments chip away at the loan balance

-

Improvements & maintenance — upgrades that increase home value

-

Forced savings effect — as you pay, you’re building net worth

In other words, home equity is a blend of market performance and disciplined repayment.

How Much Has Home Value Grown, Historically?

To appreciate what your home might be worth now, it helps to understand how home values tend to change over time.

Average Appreciation Rates

-

Over long periods, U.S. home prices typically appreciate around 3%–5% annually (though local rates vary) point.com+1

-

Historical data since 1891 shows nominal gains of ~3.4% per year, though inflation-adjusted (“real”) gains are lower Charlie Bilello’s Blog

-

Some sources place a long-term average closer to 4.3% or 4.27% per year Griffin Funding+1

-

In 2023–2024, home price growth picked up: for example, U.S. home prices rose 4.5% year over year between Q4 2023 and Q4 2024 (FHFA data) FHFA.gov

-

In the fourth quarter of 2024, FHFA reported annual gains of ~5.4% over the prior year eyeonhousing.org

These numbers show that while annual appreciation can fluctuate, over decades the upward trend is notable.

Regional Variation Is Big

-

Some housing markets have seen 50%–100% growth over 20 years. Visual Capitalist

-

In fast-growing states or metro areas (e.g. Florida, Idaho), median home prices have soared over a decade or more. Construction Coverage

-

Local factors—such as population growth, job markets, school quality, zoning, infrastructure, and scarcity—can massively amplify or dampen growth.

Because of this variation, using national averages gives you a benchmark—but your specific market may outperform or underperform that.

Equity in 2025: What the Data Says

Let’s look at some up-to-date data to see how much equity homeowners currently hold, and trends that matter.

Record-High Aggregate Equity

-

As of mid-2025, mortgaged residential properties across the U.S. carry an estimated $17.6 trillion in home equity (aggregate) CBS News

-

That’s up a strong 4% (~$690 billion) from 2024 levels CBS News

-

Meanwhile, in Q1 2025, homeowners gained $115 billion in equity—an average of about $302,000 per homeowner with a mortgage The Mortgage Reports

-

However, not all homes are equal: some saw minor dips. Between Q1 2024 and Q1 2025, the average homeowner’s equity declined by ~$4,200 — likely due to slowing price growth, rising costs, or local volatility lumberbluebook.com

Equity-Rich & Underwater Homes

-

In Q1 2025, 46.2% of mortgaged homes were considered “equity-rich” (i.e. loan balance ≤ 50% of market value) ATTOM+1

-

The percent of homes seriously underwater (loan balance ≥ 125% of value) ticked up to 2.8% ATTOM

-

Over time, those underwater rates are historically low—but still something to monitor in weaker markets. ATTOM

Home Equity Borrowing Activity

-

In Q1 2025, homeowners tapped ~$25 billion in equity through second mortgages/HELOCs — the highest volume in over 17 years for that quarter HousingWire

-

Increases in borrowing often follow when equity is high and borrowing costs (rates) drop. Experian

-

That said, caution is needed: tapping too much equity may over-leverage your home.

These data points confirm that equity remains a powerful resource—even amid market shifts and slower appreciation.

Why You Probably Have More Equity Than You Realize

If you’ve owned your home for several years, especially in a growing area, you might be pleasantly surprised by how much equity you’ve built—more than what your last check-in suggested. Here’s why:

-

Appreciation compounds over time.

Even modest yearly gains multiply: 4% growth gives ~22% gain over 5 years (compounded). -

Each mortgage payment chipped away at principal.

As interest declines over time, more of each payment goes to principal, accelerating your equity build. -

You stayed despite market volatility.

Markets fluctuate, but over longer spans, growth tends to overcome downturns. -

Some homes improved more than average.

Renovations, upgrades, and good maintenance amplify value beyond what raw market metrics suggest. -

Listings & comp sales have likely reset your area’s baseline.

As nearby homes sell for more, that raises what buyers are willing to pay for yours.

In short: your equity is the sum of time + market + effort. You may have a lot more than you think.

How Much Equity Could You Have? Let’s Walk Through Examples

Let’s see real-world scenarios to help you picture where you might stand:

Example A: Moderate Growth Market

-

You bought your home 10 years ago for $300,000

-

Annual average appreciation has been ~4%

-

Over 10 years, compounded, the home’s value would be about $445,000

-

Suppose your mortgage balance now is $150,000

-

Equity = $445,000 – $150,000 = $295,000

Example B: Strong Growth Market

-

Bought for $400,000

-

Growth averaged 6% per year (a high-growth market)

-

After 10 years, value would rise to ~$716,000

-

Mortgage now at $220,000

-

Equity = $716,000 – $220,000 = $496,000

Example C: Slower or Flat Market

-

Bought for $350,000 8 years ago

-

Market growth averaged 1–2% (sluggish area)

-

Value now ~$425,000

-

Mortgage maybe $180,000

-

Equity = $425,000 – $180,000 = $245,000

These are hypothetical, but they show that even in slower markets you may still build substantial equity over time. The stronger your local market, the more dramatic your gain.

What You Can Do with Your Equity

Your home equity isn’t just dormant value—it can be a strategic financial tool if used wisely. Here are different ways to unlock or leverage it:

1. Fund a Down Payment on a New Home

If you want to upgrade, move, or change locations, your equity could finance the down payment. In the strongest cases, it may allow a low- or no-cash move.

2. Home Renovations & Upgrades

You can borrow against your equity to invest back into the home: kitchen remodels, bathroom upgrades, energy-efficient additions, landscaping, etc. Smart renovations not only improve your quality of life but may further increase your home’s resale value.

3. Start or Grow a Business

Launching a business often requires capital. Equity can help you finance startup costs, equipment, inventory, marketing—potentially growing your income and long-term wealth.

4. Debt Consolidation / Lower-Rate Borrowing

If you have higher-interest debts (credit cards, personal loans), tapping low-cost equity (via a home equity loan or line) to pay them off can reduce your overall interest burden—provided you do so carefully.

5. Emergency Reserve / Life Events

Large expenses—education, healthcare, family needs—sometimes demand funds you don’t have on hand. Accessing equity can help in emergencies (though it’s best handled cautiously).

6. Cash-Out Refinance / Equity Extraction

You could refinance your existing mortgage to take cash out — that is, borrow a bit extra than your current balance and pocket the difference. But this increases your mortgage size and monthly payment, so it must be done carefully.

Risks & Pitfalls to Be Aware Of

Leveraging equity can be powerful—but only if you understand the risks:

-

Overleveraging: Borrowing too much against your home can leave you vulnerable if markets dip.

-

Higher interest or longer terms: Cash-out refinancing or equity loans often come with higher rates or extended terms.

-

Closing/appraisal costs: The costs of refinancing or opening HELOCs matter.

-

Market downturns: If your area’s value falls, equity can shrink—especially if you’ve borrowed heavily.

-

Foreclosure risk: If you fail to repay equity-based loans, your home can be at risk.

-

Liquidity and timing: Using equity is not instant. Appraisals, underwriting, and processing take time.

Use equity wisely—treat it as a resource, not free money.

Step-by-Step: How to Estimate & Confirm Your Home’s Value

Here’s a roadmap you can follow to get a solid estimate (or full appraisal) of your home’s current value:

1. Look at Recent Comparable Sales (“Comps”)

-

Find homes in your neighborhood with similar size, features, lot size, and condition

-

Look at sales in the last 3–6 months

-

Adjust for differences (e.g. if your home has a new roof or extra bathroom)

2. Use Online Valuation Tools

-

Zillow, Redfin, Realtor.com, local MLS tools can give ballpark estimates

-

Treat these as guides, not final answers

3. Hire a Licensed Appraiser or Realtor

-

A professional appraisal gives a reliable, defensible value

-

Realtors can run a Comparative Market Analysis (CMA)

4. Check Your Loan’s Recent Statement

-

Know your outstanding mortgage balance, including any secondary loans

-

Factor in closing costs or liens

5. Use the Equity Formula

-

Subtract your loan balance(s) from your estimated home value

-

That gives your current approximate equity

6. Track Market Trends

-

Keep an eye on local price indices, housing reports, and broad trends (e.g. FHFA, local real estate boards)

-

Understand whether your area is appreciating faster or slower than national averages

7. Reassess Regularly

-

Markets change. Check every 1–2 years, especially if you intend to sell, refinance, or borrow against equity

By doing this, you’ll have a realistic, up-to-date view of what your home is worth—and how much equity you really hold.

Voice Search & SEO Tips Embedded (for This Topic)

To help this article perform well for voice searches and SEO, I’ve embedded strategies like:

-

Question-based headers (e.g. “What Is Home Equity?”)

-

Natural phrasing, conversational tone

-

Use of “how to,” “why,” “what does it mean” — typical voice queries

-

Short paragraphs and bulleted lists (which voice assistants can parse easily)

-

Data, credible figures, and narrative examples

-

Calls to action (“If you want me to … let me know”)

These help match common voice queries like, “How much is my house worth?” or “What is home equity?”

FAQ Section (common questions people ask via voice / search)

Q1: How often should I check my home’s value?

A: Every 1 to 2 years is a good interval, or anytime you’re planning to sell, refinance, or use equity. Market conditions and local changes (zoning, development) can shift values more often in some areas.

Q2: Can I borrow 100% of my equity?

A: Not usually. Lenders often require you to keep some equity (e.g. your total loan-to-value ratio may not exceed 80%–90%). Each lender’s policies and your credit will determine how much you can access.

Q3: Does the interest I pay affect equity?

A: Yes. In early years of many mortgages, more of your payment goes toward interest, so equity builds slowly. As the loan matures, more goes toward repayment of principal.

Q4: Will home improvements guarantee value increase?

A: Not always. To add value, renovations should match neighborhood standards and be cost-effective. High-end upgrades might not pay off in areas where buyers don’t expect them.

Q5: Should I do a cash-out refinance or HELOC?

A: It depends. A cash-out refinance replaces your mortgage and often resets the interest rate and term. A HELOC adds a second lien. Choose based on rate differences, fees, flexibility, and your risk tolerance.

Q6: What happens to equity if home prices decline?

A: Your equity shrinks. If the market drops significantly, you could end up with less equity or even negative equity in extreme cases—especially if you borrowed heavily against your home.

Q7: Is home equity taxed?

A: No—equity itself is not taxed. But interest you pay on a home equity loan or HELOC may or may not be tax-deductible (depending on tax laws and how funds are used).

Q8: Can I tap equity without selling my home?

A: Yes. Through tools like HELOCs, home equity loans, or cash-out refinancing, you can borrow against your equity while continuing to live in the house.

Q9: What’s the difference between “market value” and “appraised value”?

A: Market value is what a buyer is willing to pay. Appraised value is determined by a licensed appraiser (based on comps, condition, etc.). They often align but may differ in certain conditions.

Q10: How much does an appraisal cost?

A: Costs vary by region and home complexity, but a typical residential appraisal may range from a few hundred to over a thousand dollars. Always get quotes from certified appraisers.

Conclusion / Next Steps

Your home is more than a place to live—it’s a living asset. Its value likely exceeds what you last checked, and the equity you’ve built could be a powerful financial resource.

Here’s what you can do now:

-

Estimate your home’s current value using comps, online tools, or a professional appraisal.

-

Subtract your mortgage balance from that estimated value to see your equity.

-

Decide whether and how to use your equity (e.g. home upgrade, down payment, business funding).

-

Proceed cautiously, keeping risks in mind, especially local trend changes and borrowing terms.

-

Reevaluate regularly, especially before big financial decisions (selling, refinancing, borrowing).

![]()

Do You Know How Much Your House Is Really Worth?

Want to know something important you probably don’t have a professional check for you nearly as often as you should? Spoiler alert: it’s the value of your home.

Because here’s the reality. Your house is likely the biggest financial asset you have. And if you’ve lived in it for a few years or more, chances are it’s been quietly building wealth for you in the background – even if you haven’t been keeping tabs on it.

You might be surprised by just how much it’s grown, even as the market has shifted over the past few months.

What Is Home Equity?

That hidden wealth in your home is called equity. It’s the difference between what your house is worth today and what you still owe on your mortgage. Your equity grows over time as home values rise and as you make your monthly payments. Here’s an example to help you really understand how the math works.

Let’s say your house is now worth $500,000, and you have $200,000 left to pay off on your loan. That means you have $300,000 in equity. And that’s right in line with what the typical homeowner has right now.

According to Cotality, the average homeowner with a mortgage has about $302,000 in equity.

Why You Probably Have More Than You Think

Here are the two main reasons homeowners like you have near record amounts of equity right now:

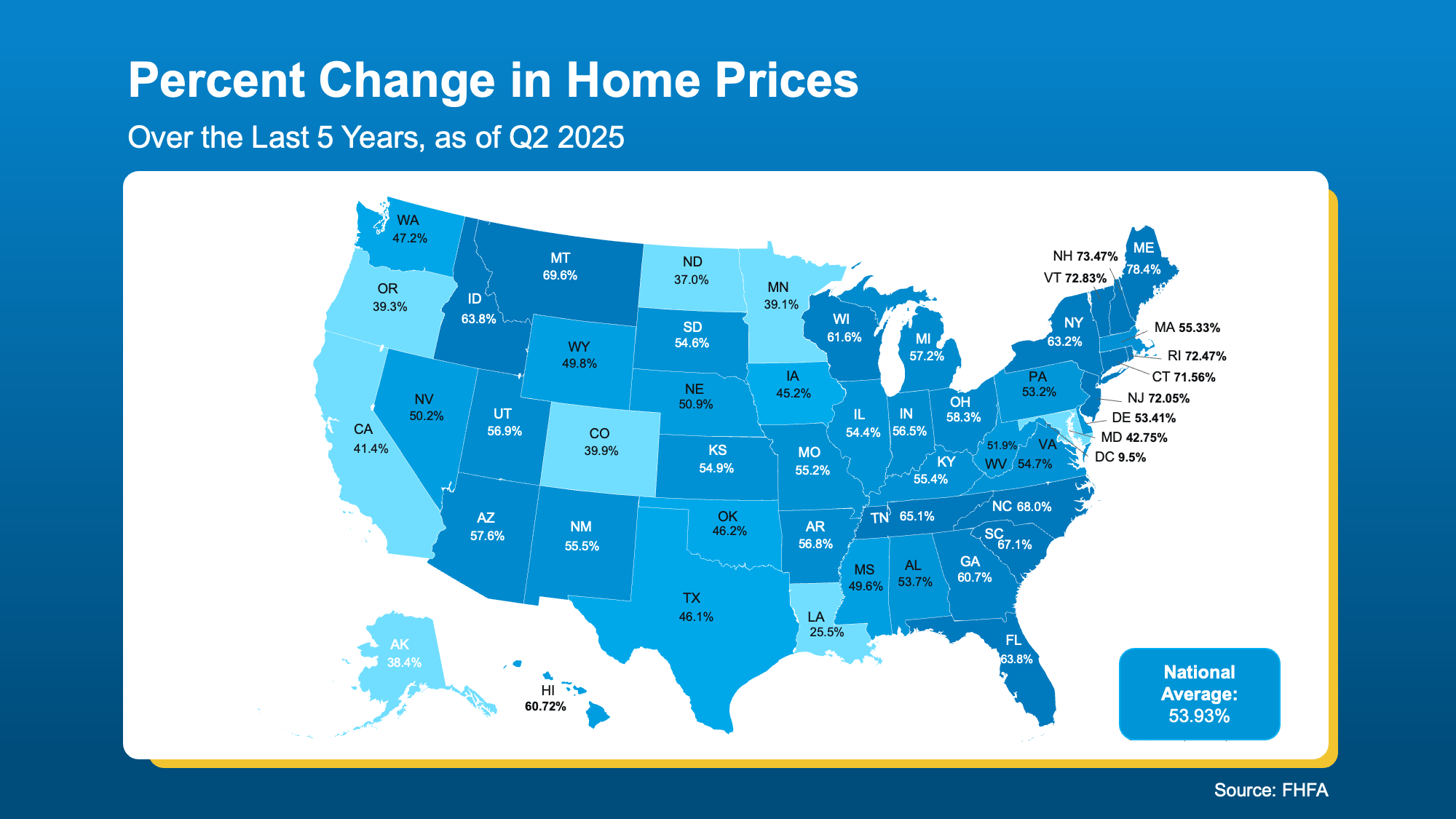

1. Significant Home Price Growth. According to the Federal Housing Finance Agency (FHFA), home prices have jumped by nearly 54% nationwide over the last five years (see map below):

This means your house is likely worth much more now than when you first bought it, thanks to how much prices have climbed over time. And if you’re worried because you’ve heard prices are flattening or even coming down in some markets, just know if you’ve been in your house for a few years (or more) you very likely have enough equity to sell and still come out ahead.

This means your house is likely worth much more now than when you first bought it, thanks to how much prices have climbed over time. And if you’re worried because you’ve heard prices are flattening or even coming down in some markets, just know if you’ve been in your house for a few years (or more) you very likely have enough equity to sell and still come out ahead.

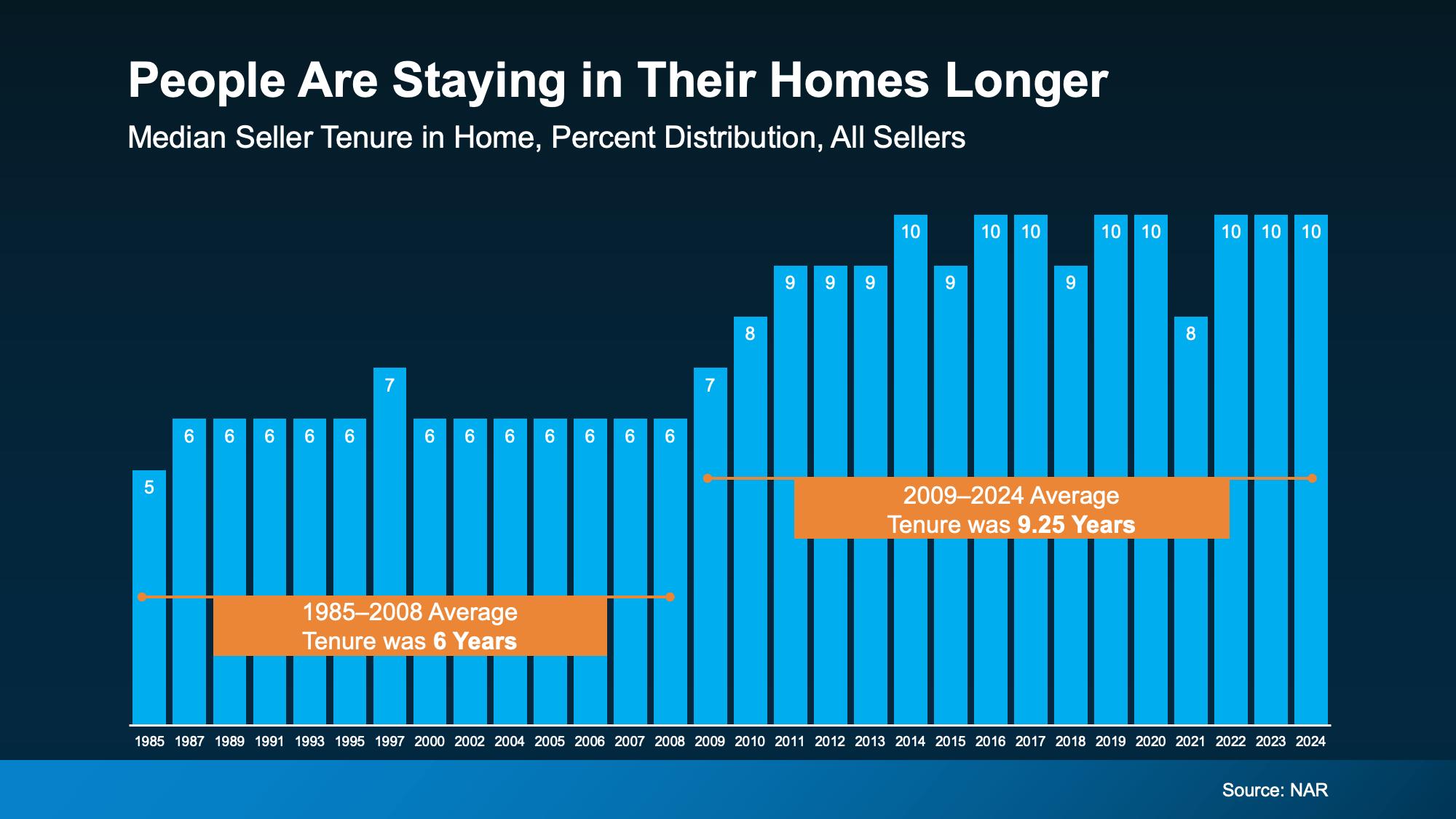

2. People Are Living in Their Homes Longer. Data from the National Association of Realtors (NAR), shows the average homeowner stays in their home for about 10 years now (see graph below):

That’s longer than it used to be. And over that decade? You’ve built equity just by making your mortgage payments and riding the wave of rising home values. Because the financial side of homeownership is about playing the long game, not worrying about little ups and downs in the market here and there. And over time, that means you’re winning.

That’s longer than it used to be. And over that decade? You’ve built equity just by making your mortgage payments and riding the wave of rising home values. Because the financial side of homeownership is about playing the long game, not worrying about little ups and downs in the market here and there. And over time, that means you’re winning.

So, if you’re one of those people who’s been in their home for a bit, here’s how much the behind-the-scenes price growth has helped you out. According to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

What Could You Actually Do with That Equity?

Your equity isn’t just a number. It’s a tool you can use to unlock your next big move. Depending on your goals, you could:

- Use it to help buy your next home. Your equity could help you cover the down payment on your next home. In some cases, it might even mean you can buy your next house in all cash.

- Renovate your current house to better suit your life now. And, if you’re strategic about your projects, they could add even more value to your home if you do sell later on.

- Start the business you’ve always dreamed of. Your equity could be exactly what you need for startup costs, equipment, software, or marketing. And that could help increase your earning potential, so you’re getting yet another financial boost.

Bottom Line

Chances are, your house is worth quite a bit right now. If you’re curious about the value of your home, let’s connect. We’ll run the numbers and give you a professional equity assessment report, so you know what you’re working with and where you can go from here.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Get Pre-Approved Today