Downsizing Without Debt: How More Homeowners Are Buying Their Next Home in Cash

Meta Title: Downsizing Without Debt: Buy Your Next Home in Cash & Escape Mortgage Stress

Meta Description: Discover how equity-rich homeowners are downsizing by paying cash—no mortgage, no monthly payments. Learn the trend, strategies, risks, and how to make it work for you.

Introduction: Rethinking “Downsizing” as Financial Freedom

When many people hear “downsizing,” they imagine giving up comfort, cutting corners, or moving into something lesser. But what if downsizing could mean freedom — especially freedom from debt?

More homeowners are now choosing to fund their next home entirely with cash. No mortgage. No monthly principal and interest payments. Instead, they use the equity they’ve built in their current home to reposition themselves for a lower-stress, more flexible lifestyle.

If you’ve owned your home for a long time, have equity, and are looking for less burden (less maintenance, less cost, less stress), this trend offers a compelling path forward.

In this article, we’ll explore:

-

Why more homeowners are mortgage-free than ever

-

How the all-cash purchase trend is evolving

-

How to turn your equity into buying power

-

Step-by-step strategies to downsize using cash

-

Risks, pitfalls, and practical considerations

-

Real-world examples, voice search phrasing, and FAQs

Let’s dive in.

1. The Rise of Mortgage-Free Homeownership

1.1 A Historic Share of Mortgage-Free Homes

Owning your home outright (i.e., having no mortgage) was once seen as a rare luxury. But in recent years, the proportion of U.S. homeowners in that position has grown significantly.

-

Analysis of census and housing data indicates that over 40% of U.S. owner-occupied homes are now mortgage-free — the highest recorded share in this series. BAM – The Key To Thriving in Real Estate+1

-

In 2023, the share was around 39.8%, indicating a steady upward trend. BAM – The Key To Thriving in Real Estate

-

Historically, in 2010, that figure was about 32.8% — meaning the mortgage-free share has climbed by nearly 8 points over 15 years. BAM – The Key To Thriving in Real Estate+1

-

Among older homeowners, the rates are even higher: for those age 65 and above, about 64% own their homes outright. BAM – The Key To Thriving in Real Estate

That growth is driven largely by demographics: as Baby Boomers and older Gen Xers age, many have had time and stable income to fully pay down their mortgages.

Voice Search / User Query Examples

-

“What percentage of U.S. homeowners have paid off their mortgage?”

-

“How many homes in the U.S. are mortgage-free in 2025?”

-

“Why are more people owning homes outright?”

1.2 Why the Mortgage-Free Trend Matters

The increasing share of mortgage-free homes has broader implications:

-

Greater buying power: These homeowners can tap into equity more flexibly.

-

Reduced financial vulnerability: With no mortgage, they are less exposed to rate shocks, refinancing risk, or credit shifts.

-

Downsizing potential: When the time comes to move, these owners carry more flexibility to make bold moves, like all-cash purchases.

-

Demographic momentum: As the population ages, more households will reach this mortgage-free status.

In short: as more people fully own their homes, more are entering a position of strength when it comes to their next move.

2. The Surge (and Shifts) in All-Cash Home Purchases

2.1 Recent Data & Trends

All-cash purchasing is not new, but its scale and implications have evolved. Let’s review key trends:

-

According to the National Association of Realtors, 32% of home sales in January 2024 were all-cash transactions — the highest rate since 2014. National Association of REALTORS®+1

-

In 2024, all-cash purchases made up 32.6% of U.S. home sales—down slightly from 35.1% in 2023, marking the lowest share in three years. ProBuilder+3Redfin+3Redfin Real Estate News+3

-

Despite the dip, that 32.6% figure remains well above pre-pandemic levels, when all-cash deals typically ranged from 25% to 30%. Redfin Real Estate News+2ProBuilder+2

-

All-cash transactions are particularly prevalent at the lower and upper ends of the housing price spectrum — creating a U-shaped distribution:

-

Low-priced homes (< $100,000): up to two-thirds sold in cash in many markets. Investopedia+2New York Post+2

-

Luxury / high-end homes ($1M+): 40% or more purchased in cash in many cases. National Association of REALTORS®+3Investopedia+3New York Post+3

-

2.2 Why All-Cash Purchases Are Attractive to Buyers & Sellers

To Buyers (especially equity-rich ones)

-

Speed & certainty: No appraisal financing delays, fewer contingencies.

-

Bargaining power: Some sellers prefer cash offers even at a slight discount over financed ones.

-

Simplicity: Less paperwork, fewer moving parts, fewer lender demands.

-

No mortgage risk: No interest rate risk, no underwriting surprises.

To Sellers

-

Faster closing: Less friction, fewer delays or financing fallouts.

-

Lower risk: No risk that a buyer’s loan falls through.

-

Appeal in competitive markets: Cash offers cut through in bidding wars.

As one recent Investopedia article put it, “There’s one way to beat the sky-high mortgage rates: pay in cash.” Investopedia

2.3 Regional & Price Tier Variations

-

States like West Virginia (41.1%), New York (40.4%), and Delaware (38.9%) report some of the highest shares of all-cash transactions. newamericanfunding.com+2PR Newswire+2

-

In Florida, many metros report all-cash purchase shares between 38–50%, especially for lower-priced homes. Redfin+2Redfin Real Estate News+2

-

Coastal and high-value markets like San Jose, CA, are on the lower end of the cash spectrum (e.g., ~18.1% in 2024). Redfin+2ProBuilder+2

-

In the Washington D.C. region, ~18.9% of homes sold in 2024 were purchased with cash. The Washington Post

-

In many luxury segments (multi-million dollar properties, second homes, vacation homes), cash is the default. New York Post

Thus, while cash deals are widespread, the context (local market, price point, buyer profile) matters a lot.

Voice Search / Query Examples

-

“What percent of homes are sold for cash in 2025?”

-

“Which U.S. states have the most all-cash home purchases?”

-

“Why do sellers prefer cash offers over financed ones?”

3. Turning Home Equity Into Cash Buying Power

If you’re among the growing number of mortgage-free or nearly mortgage-free homeowners, your equity can be your greatest strategic lever. Here’s how to transform it into a powerful tool for your next move.

3.1 Understand Your Equity & Proceeds

Home equity = Current market value of your home minus any outstanding mortgage balance (if any).

If your home is mortgage-free, your equity is (roughly) your home value less any costs or liens.

Net proceeds from selling = Sale price minus:

-

Real estate agent commissions

-

Closing costs (title fees, transfer taxes, etc.)

-

Repairs or concessions

-

Outstanding property taxes, HOA dues, or liens

For example:

If your home sells for $400,000, and your total costs (commission, closing, repairs) are $30,000, you net $370,000.

That $370,000 becomes your “cash war chest” for your next home.

3.2 How Much You Can Use (All vs Partial)

You have options:

-

All-cash purchase: Use most or all of the net proceeds to fully pay for your next home.

-

Cash + small mortgage: Keep some reserves (for emergencies, liquidity) and borrow a small mortgage for the balance.

-

Bridge financing / short-term line: In rare cases, you might use a bridge loan or home equity line while switching homes — though that reintroduces debt (which goes against the “downsizing without debt” philosophy).

Many downsizers pick the all-cash route when their equity suffices to cover their next home comfortably, plus a buffer.

3.3 Why Downsizing Amplifies the Power of Equity

Downsizing often means moving to a smaller, lower-cost home. Because of that:

-

Your equity stretches further

-

You reduce ongoing costs (maintenance, utilities, taxes)

-

You free up more liquid capital for investing, travel, or legacy goals

-

You minimize upkeep stress and complexity

In effect, selling a large, expensive home and applying proceeds to a modest one means the difference becomes your margin of freedom.

3.4 Illustrative Scenario

Suppose:

-

You own a 3,000 sq ft home in suburbia, paid off, worth $600,000

-

After fees and closing, net about $560,000

-

You decide to buy a 1,500 sq ft, lower maintenance home in a nearby area for $350,000 in cash

-

You preserve $210,000 in reserves for emergencies or reinvestment

This gives you:

-

A home you love, with no mortgage

-

A large cash reserve

-

Lower taxes, upkeep, and utility burden

-

Financial peace of mind — especially appealing in retirement

In short: your equity becomes a source of financial flexibility, not just real estate value.

4. Step-by-Step Guide: How to Downsize via Cash Purchase

Here’s a detailed roadmap to help you bring this idea into real life.

4.1 Step 1: Assess Your Current Home’s Value Accurately

-

Engage a licensed appraiser or trusted real estate agent for a comparative market analysis (CMA).

-

Look at recent sales of similar homes in your neighborhood.

-

Factor in your home’s condition, upgrades, age, and local trends.

This helps you set realistic expectations and plan your next steps.

4.2 Step 2: Estimate Net Proceeds

-

Subtract expected commissions, closing costs, and repair allowances

-

Account for capital gains tax, if applicable (or exemptions)

-

Deduct any outstanding liens, unpaid taxes, or HOA balances

Make a conservative estimate to avoid surprises.

4.3 Step 3: Define Your Target Home & Budget

-

Pick your target area, size, amenities, and price range

-

Allow for inflation, property taxes, maintenance, and insurance

-

Decide how much you want to allocate (all cash or a portion)

-

Keep a cash reserve for unexpected needs

4.4 Step 4: Coordinate the Timing & Contingencies

One key challenge is timing — especially avoiding a period where you own two homes or have to rent. Strategies include:

-

Simultaneous closings: Sell your current home the same day you purchase the next home

-

Home sale contingency: Contract purchase contingent on the sale of your current home (but risk losing preferred properties)

-

Bridge financing or interim rent: Rarely used in this context, unless necessary

Your real estate agent’s coordination is vital.

4.5 Step 5: Prepare & Stage Your Current Home

-

Declutter and make necessary repairs

-

Stage it to appeal broadly

-

Price it attractively but realistically

-

Market it aggressively for maximum exposure

A clean, well-positioned listing may fetch a better price and reduce time on market.

4.6 Step 6: Negotiate & Structure the Contract

-

Emphasize your all-cash status — sellers often view cash offers favorably

-

Be flexible (e.g., on closing dates, contingencies)

-

Include inspection, title, and appraisal contingencies (unless you waive some)

-

Be ready to move quickly: cash offers tend to accelerate timelines

4.7 Step 7: Execute the Transaction

-

Work with a reliable title company, escrow agent, and legal counsel

-

Ensure proper title transfer, tax compliance, and closing documents

-

Confirm funds availability and wiring logistics

-

Oversee the move, arrange utilities, and execute on your new home vision

4.8 Step 8: Post-Transaction Checklists

-

Ensure reserves are in accessible form (savings, investments, cash)

-

Adjust your budget to your new home’s costs

-

Review tax implications (property, capital gains, deduction changes)

-

Maintain discipline on your reserve usage

By following each of these steps, you make your transition smoother and safer.

5. Real-World Examples & Use Cases

Seeing how others have done it can make the idea more tangible.

5.1 Retired Couple Moves to Simplicity

-

A couple in their 70s sells their 4,000 sq ft suburban home (paid off) for $500,000

-

After costs, they net $460,000

-

They buy a single-story townhouse for $280,000 in a quiet town

-

They keep $180,000 in savings

-

They use the extra cash to travel, gift to children, and bolster their retirement cushion

Outcomes:

-

No mortgage

-

Lower upkeep, taxes, and utility costs

-

Peace of mind

5.2 Mid-Career Downsizer Seeks Flexibility

-

A 55-year-old professional sells a large family home worth $650,000 (almost paid off)

-

After closing costs, net about $610,000

-

They purchase a newer, smaller home for $400,000 in a community closer to family

-

They place $210,000 in conservative investment instruments

-

They gain location comfort, freedom to travel, and more flexible cash flow

5.3 Luxury or Second Piece Moves

In high-end markets, many buyers (retirees, investors, relocators) routinely purchase properties with cash, especially for vacation or second homes. In Miami, for example:

-

Over 50% of homes priced between $1M and $5M were sold for cash recently. New York Post

-

As price tiers climb, the share of cash purchases rises further. New York Post+1

For those accustomed to equity leverage, cash purchases become a natural tool.

6. Risks, Pitfalls & Important Considerations

No strategy is without tradeoffs. Here are important factors to watch:

6.1 Liquidity & Emergency Cushion

-

Avoid draining all your reserves to make the purchase.

-

Keep enough cash or liquid investments to cover unexpected costs, healthcare, or life changes.

6.2 Timing Risk & Market Fluctuations

-

If the real estate market softens between your sale and purchase, you could lose buying power.

-

Coordinating closings is critical; gaps or overlapping ownership present financial risk.

6.3 Transaction Costs & Hidden Expenses

-

Closing costs, transfer taxes, title insurance, and realtor commissions can eat into your equity.

-

Unexpected repairs or concessions may emerge from inspections or negotiations.

6.4 Opportunity Cost

-

If your cash isn’t earning returns (e.g. stocks, bonds, business), there’s an opportunity cost in tying it up in real estate.

-

Compare the yield you could get from investments vs the “return” from owning the home.

6.5 Loss of Mortgage Interest Deductions (if previously used)

-

If you previously deducted mortgage interest for tax purposes, you’ll lose that benefit.

-

But for many downsizers, that cost is low compared to the benefit of lower debt.

6.6 Estate, Tax & Legal Complexities

-

Capital gains tax: Ensure you use applicable primary residence exemptions.

-

Transfer taxes or local property laws: Be aware of local rules.

-

Estate planning: Large home equity shift may need trust or will adjustments.

6.7 Emotional & Lifestyle Fit

-

Make sure the downsized home matches your needs (mobility, medical, community, proximity to family).

-

Don’t let financial rationality overshadow quality of life — the goal is fulfillment, not just savings.

7. SEO, AEO & Voice Search Integration Tips

Because your article or content will likely live online, here are best practices to ensure it gets found, answers real intent, and resonates in voice search.

7.1 Use Conversational, Question-Based Headers (for Voice & AEO)

Include headers (H2, H3) like:

-

“What percentage of homeowners are mortgage-free today?”

-

“Why do sellers prefer cash offers over financed ones?”

-

“How can I buy a house with cash after selling mine?”

-

“What risks should I watch when downsizing in cash?”

These mirror how people speak in queries (e.g., “Hey Siri, how to buy a house in cash?”).

7.2 Embed “People Also Ask” Questions

Identify common PAA questions (e.g., “Can you sell one house to buy another with cash?”) and provide succinct answers (40–60 words) immediately under a relevant header. This helps your article be pulled into those spotlights.

7.3 Use Schema Markup (FAQPage, HowTo)

-

Add an FAQ schema with 5–10 common questions and short answers

-

Optionally, a HowTo schema for the step-by-step downsizing process

These help search engines show your content as rich results or voice responses.

7.4 Keyword & Semantic Terms (Naturally Placed)

Suggested keywords / phrases:

-

“downsize without debt”

-

“buying next home in cash”

-

“mortgage-free homeowners”

-

“all-cash home purchase trend”

-

“sell and buy home with cash strategy”

-

“cash home transaction risks”

-

“how many homes are mortgage free 2025”

Use these strategically in headers, intro, body, and conclusion — naturally, not forced.

7.5 Use Internal & External Links

-

Link to reliable sources (e.g. NAR, Redfin, Census data)

-

If this is on your site, link to complementary content (tax advice, downsizing tips, home valuation calculators)

-

Use anchor text like “mortgage-free households data” or “all-cash home sale trends 2024”

7.6 Write for Readability & Scannability

-

Keep paragraphs short (~2–4 sentences)

-

Use bold text to highlight key terms or calls to action

-

Use bulleted lists (as above)

-

Add summary boxes or “Key Takeaways” sections

These practices help both humans and algorithms consume your content more easily.

8. Voice Search–Optimized Phrasings & Query Anchors

Throughout the article, we can sprinkle voice search trigger lines that echo how people ask questions:

-

“How many U.S. households own their homes outright?”

-

“Can I buy a house with cash after I sell mine?”

-

“Why are cash offers better than mortgage offers?”

-

“What risks should I consider when paying for a house in cash?”

-

“Steps to downsize using equity without getting a new loan”

When search engines or devices parse your content, these phrases help match spoken queries to your article.

9. FAQs & Voice Search–Friendly Answers (for Schema)

Here are expanded FAQ entries you can embed (also helpful for voice responses):

Q: Can I really buy a house in cash after selling mine?

A: Yes. If your sale nets enough funds, many homeowners use those proceeds to pay cash for their next home—eliminating or minimizing mortgage use.

Q: What percentage of U.S. home sales are cash in 2024?

A: About 32.6%—the lowest share in three years but still significantly above pre-pandemic levels. Redfin+2Redfin Real Estate News+2

Q: Why do sellers prefer cash offers over financed ones?

A: Cash offers reduce risk of appraisal contingencies or loan failures, close faster, and offer more certainty.

Q: What are the main risks in buying a home with cash?

A: Risks include losing liquidity, timing mismatches between sale and purchase, market dips, transaction costs, and opportunity cost of tying up funds.

Q: Should I ever keep some of the equity in cash instead of buying all with it?

A: Yes. Most prudent downsizers keep a reserve for emergencies, unexpected costs, or investment flexibility.

Q: Is downsizing always the better move?

A: Not always. It depends on your lifestyle, mobility, community preferences, and whether your cash yields more value elsewhere.

10. Conclusion: Make the Next Move with Intention and Power

Downsizing without debt isn’t a pipe dream — it’s a growing trend rooted in financial discipline, demographic shifts, and smart use of equity. As more homeowners live mortgage-free, the possibility of using that equity to buy a home outright becomes more real.

The journey isn’t riskless, and it demands planning, timing, and a clear sense of what “home” should mean in your next chapter. But when done well, the rewards are profound: peace of mind, reduced stress, lower costs, and more control over your future.

Next steps you can take today:

-

Get a professional valuation of your current home

-

Estimate your net proceeds if you sold

-

Map out your ideal downsized home (budget, location, features)

-

Line up a trusted real estate agent familiar with all-cash deals

-

Prepare your documentation, liquidity plan, and contingency strategies

![]()

Downsizing Without Debt: How More Homeowners Are Buying Their Next House in Cash

If you’ve been thinking about downsizing to lower your expenses, be closer to family, or just make life easier, here’s a trend worth paying attention to:

More homeowners are buying their next house outright, without taking on a new mortgage. And, if you’ve owned your home for a while, you may be able to do the same. No mortgage. No monthly housing payments.

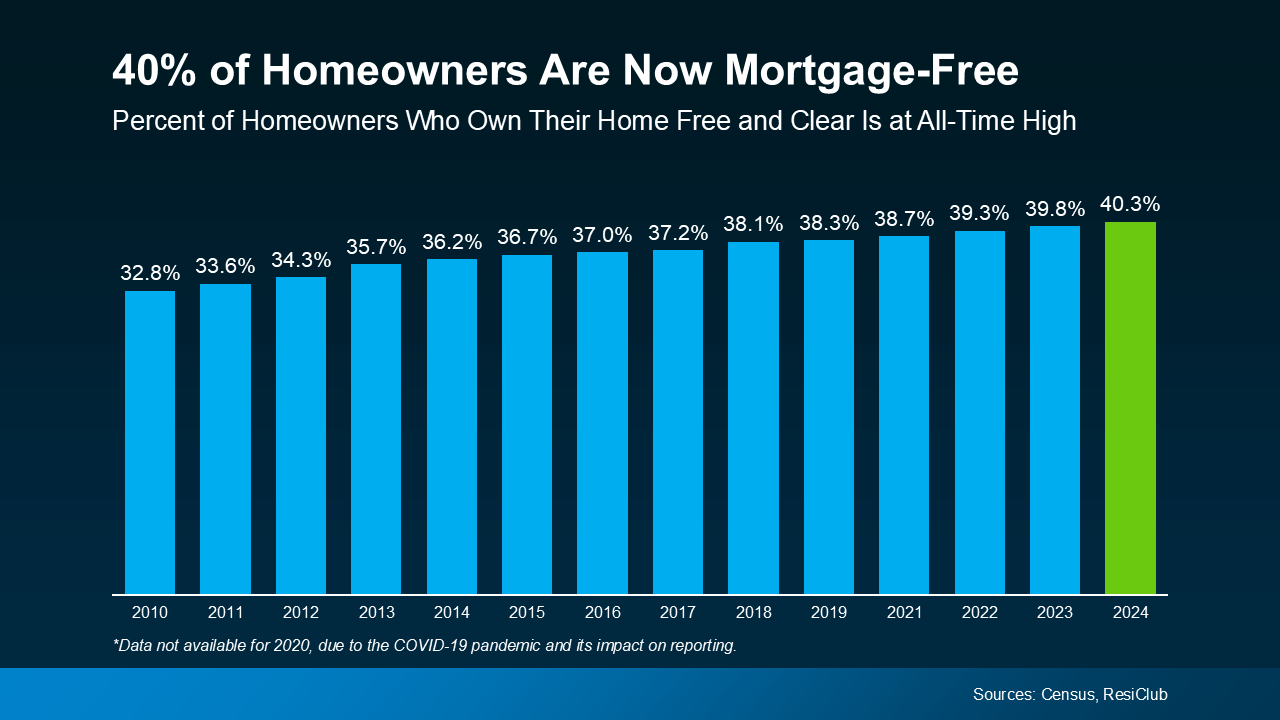

A Record Share of Homeowners Are Mortgage-Free

According to analysis from ResiClub of Census data, more than 40% of U.S. owner-occupied homes are mortgage-free – an all-time high for this data series. That means 4 in 10 homeowners own their homes free and clear (see graph below):

One big reason for this trend? Demographics. As Baby Boomers age and stay in their homes longer, many have had the time to fully pay off their mortgages. You might be in that group too and not even realize just how much buying power you now have. It’s time to change that.

One big reason for this trend? Demographics. As Baby Boomers age and stay in their homes longer, many have had the time to fully pay off their mortgages. You might be in that group too and not even realize just how much buying power you now have. It’s time to change that.

How Downsizers Are Turning Equity into Buying Power

As a homeowner, your equity is your biggest advantage in today’s market. If you’re mortgage-free (or close to it), it could give you the power to buy your next home in cash. That means you’d still have no mortgage payment in retirement, plus:

- Less financial stress as you age

- More cash flow, if you purchase a less expensive home

- And it would likely be a faster, simpler transaction

Here’s how it works. You’d sell your current house and use the proceeds to buy your next house in cash. And while that may sound like something you thought would never be possible for you, it’s more realistic than you may think.

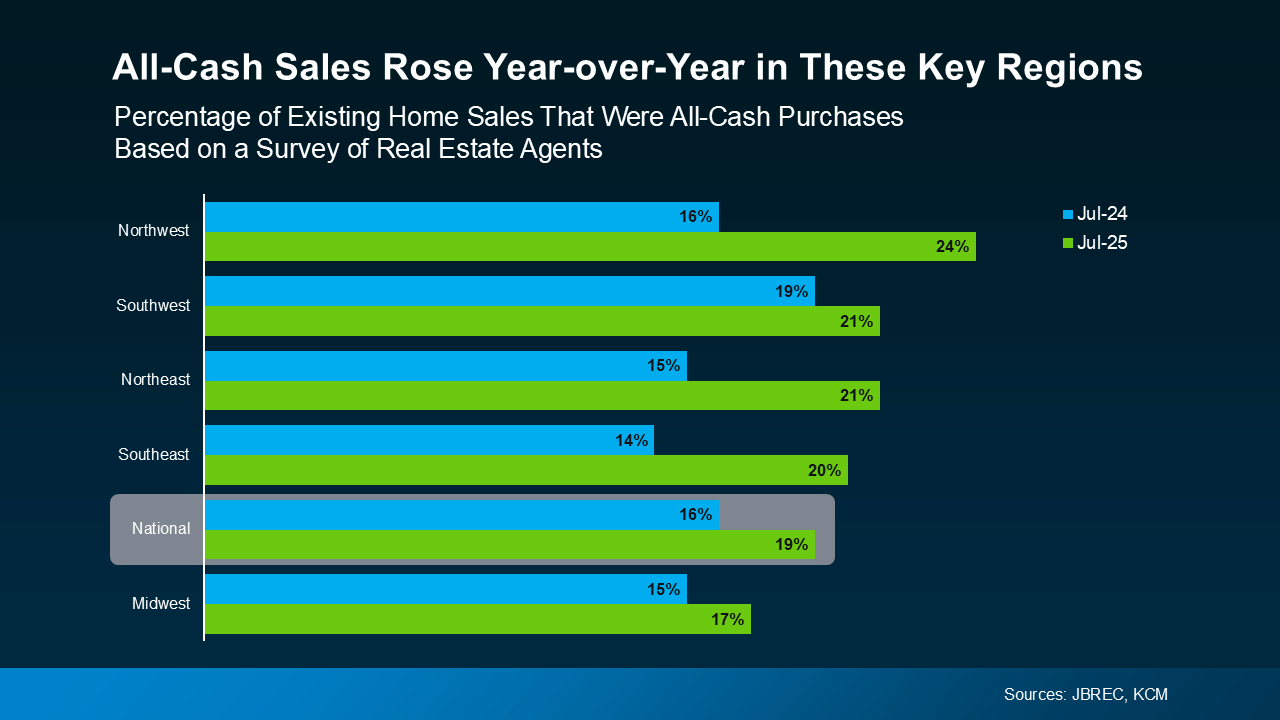

In the latest survey from John Burns Research and Consulting (JBREC) and Keeping Current Matters (KCM), agents reported the share of purchases with all-cash buyers is climbing nationally. And those agents are seeing increases in almost every region of the country (see graph below):

For Baby Boomers especially, buying in cash gives you more control over your next chapter. You could buy a smaller, less expensive home and have lower costs, less upkeep, and more flexibility to enjoy what matters most. All while staying debt and stress free.

For Baby Boomers especially, buying in cash gives you more control over your next chapter. You could buy a smaller, less expensive home and have lower costs, less upkeep, and more flexibility to enjoy what matters most. All while staying debt and stress free.

Because downsizing isn’t about downgrading your home. It’s about upgrading your quality of life. And that’s something worth exploring.

Bottom Line

You’ve worked hard for your home. Now it might be time for it to work hard for you.

Let’s talk about what your house is worth, and what it could unlock for you today. What would your ideal home look like if you were to downsize right now?

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Get Pre-Approved Today