Fannie Mae DU Version 12.1 Breakdown: Credit, Income & Data Changes Affecting Loan Approvals in 2026

Introduction: A Defining Moment in Mortgage Lending

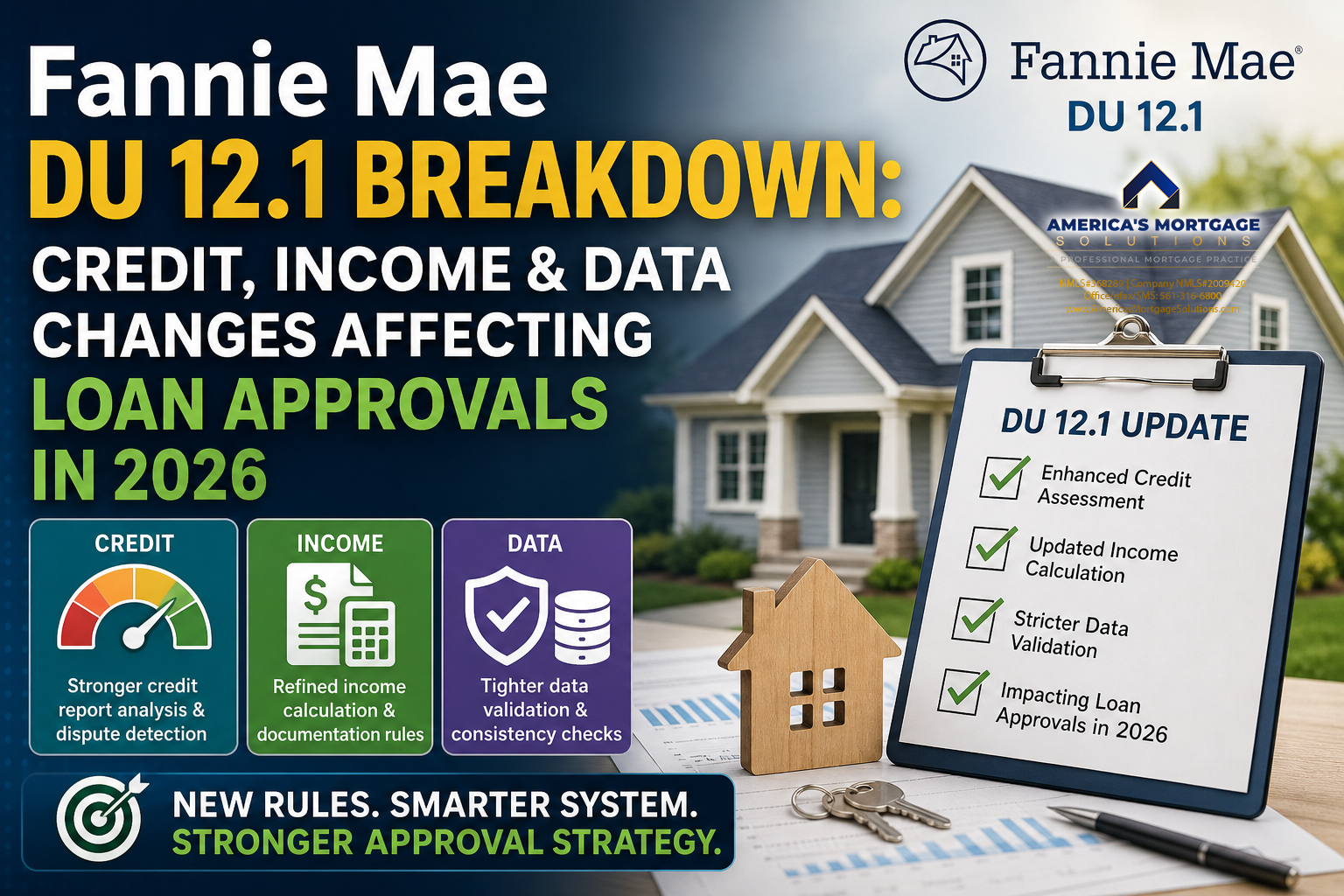

The release of Fannie Mae DU 12.1 in March 2026 marks a turning point in how mortgage approvals are evaluated across the United States—especially in high-demand markets like West Palm Beach, North Palm Beach, and Wellington, Florida (FL).

This is not just another system update.

It’s a shift toward:

- Stricter data validation

- Advanced income analysis

- Automated credit scrutiny

For borrowers, real estate professionals, and lenders, this means one thing:

👉 You must get everything right BEFORE submitting your loan.

According to Christian Penner, a Mortgage Broker, Mortgage Lender, Real Estate Agent, and Real Estate Advisor at America’s Mortgage Solutions (AMS):

“DU 12.1 eliminates guesswork. If your file isn’t clean upfront, the system will reject it instantly.”

What Is DU 12.1 and Why It Matters in 2026

Desktop Underwriter (DU) is Fannie Mae’s automated system used to assess borrower eligibility.

With DU Version 12.1, the system now prioritizes:

- Accuracy over interpretation

- Automation over manual review

- Consistency over flexibility

Core Focus Areas

- Credit report data handling

- Income calculation logic

- Data validation tightening

Why This Matters

In competitive housing markets like Wellington, FL, even minor inconsistencies can delay or deny approvals.

Major Changes in DU 12.1 Explained

1. Credit Report Data Handling Becomes More Advanced

DU 12.1 introduces enhanced algorithms to evaluate borrower credit profiles.

Key Updates

- Structured tradeline parsing

- Stronger detection of disputed accounts

- Improved liability recognition

Impact on Borrowers

- Messy credit reports are flagged instantly

- Disputed accounts carry more risk

- Less flexibility for post-submission corrections

Voice Search Answer

“How does DU 12.1 affect my credit score for a mortgage?”

It doesn’t change your score, but it analyzes your credit report more deeply, identifying risks faster and more accurately.

2. Income Calculation Changes (The Biggest Game-Changer)

This is where DU 12.1 has the most impact.

Updated Income Evaluations

- Variable income (bonuses, commissions)

- Self-employed borrower analysis

- Year-to-date (YTD) income trending

- VOE (Verification of Employment) alignment

What This Means

- Declining income trends are flagged quickly

- Inconsistent earnings reduce approval chances

- Documentation must match perfectly

Expert Insight

Christian Penner (AMS) explains:

“Income now needs to tell a consistent story backed by data. If it doesn’t, DU 12.1 won’t approve it.”

3. Data Validation Tightening and Automation Expansion

DU 12.1 strengthens integration with validation tools like Day 1 Certainty®.

System Enhancements

- Cross-checking multiple data sources

- Identifying inconsistencies instantly

- Reducing manual overrides

Impact

- More “Refer” findings

- More “Incomplete” applications

- Faster approvals for clean files

The Strategic Advantage: DU 12.0 vs DU 12.1

One overlooked rule creates a major opportunity:

👉 Loans submitted under DU 12.0 remain under those guidelines if resubmitted.

Why This Matters

- DU 12.0 offers more flexibility

- DU 12.1 enforces stricter validation

Strategy Tip

Work with experts like Christian Penner at America’s Mortgage Solutions (AMS) to determine whether locking under DU 12.0 provides a strategic advantage.

How Mortgage Strategy Has Changed in Florida

Before DU 12.1

- Adjustments after submission

- Flexible income interpretation

- Greater reliance on underwriters

After DU 12.1

- Precision before submission

- Stronger documentation requirements

- Automated decision dominance

Local Insight

In fast-moving areas like West Palm Beach and North Palm Beach, properly structured files now win deals faster.

Loan Scenarios That Will Struggle Under DU 12.1

High-Risk Borrowers

- Self-employed with declining income

- Commission-based earners

- Inconsistent deposits

- Credit disputes

Voice Search Answer

“Why was my mortgage denied in 2026?”

Most denials are due to inconsistent income, unresolved credit issues, or mismatched financial data.

Loan Profiles That Will Get Approved Faster

Strong Candidates

- W2 employees with stable income

- High asset reserves

- Consistent employment history

- Verified financial data

Key Insight

Clean, simple financial profiles are now rewarded more than ever.

Step-by-Step Strategy to Get Approved Under DU 12.1

Step 1 – Clean Up Your Credit

- Remove disputes

- Verify all tradelines

- Fix inaccuracies

Step 2 – Stabilize Your Income

- Avoid job changes

- Maintain consistency

- Document all income sources

Step 3 – Prepare Documentation

- Tax returns

- Bank statements

- Employment verification

Step 4 – Work with an Expert

Partnering with Christian Penner (AMS) ensures:

- Strategic file structuring

- Optimized submission timing

- Higher approval success

Local Market Impact: Florida Buyers Must Adapt Quickly

In Wellington, West Palm Beach, and North Palm Beach:

- Competition is high

- Speed matters

- Accuracy is critical

What This Means

- Pre-approvals must be fully verified

- Financials must be clean and consistent

- Strategy matters more than ever

June 2026 Update: What Comes Next

DU 12.1 is only the beginning.

March 2026

- Data validation changes

- Income analysis updates

June 2026

- Messaging refinements

- Qualification adjustments

- Policy alignment

Key Insight

This is a multi-phase transformation in mortgage underwriting.

Why Choosing the Right Mortgage Professional Is Critical

As automation increases, expertise becomes more valuable.

About Christian Penner

At America’s Mortgage Solutions (AMS), the focus is:

- Structuring files for approval

- Understanding local Florida markets

- Maximizing borrower success

The Bigger Trend: Automation Is Taking Over

DU 12.1 reflects a broader industry shift:

- From manual underwriting

- To data-driven automation

What This Means

- Less flexibility

- Faster decisions

- Higher accuracy requirements

FAQ Section

What is DU 12.1?

DU 12.1 is Fannie Mae’s updated automated underwriting system focused on stricter credit, income, and data validation.

Is it harder to get approved in 2026?

Yes, especially for borrowers with inconsistent income or credit issues.

Who benefits most from DU 12.1?

Borrowers with clean credit, stable income, and strong documentation.

Can self-employed borrowers still qualify?

Yes, but with stricter documentation and consistent income trends.

How can I improve my chances?

Work with an expert like Christian Penner at America’s Mortgage Solutions (AMS) to structure your file correctly.

Final Thoughts: The New Rules of Mortgage Approval

The Fannie Mae DU 12.1 update is clear:

👉 Preparation is everything

👉 Accuracy is non-negotiable

👉 Automation is the future

Bottom Line

The advantage now belongs to those who:

✔ Structure files correctly upfront

✔ Maintain clean financial profiles

✔ Work with experienced professionals

Read from source: “America’s Mortgage Solutions (AMS)”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice