What Buyers Really Want in 2025: Prices, Rates, and How the Market Is Responding

Meta Description

Homebuyers consistently cite affordability—namely home prices and mortgage rates—as their top concern. This article explores how the housing market is shifting in 2025, what buyers need to know right now, and how to act with confidence heading into 2026.

Introduction

What do homebuyers say they need most in today’s housing market? A recent survey from Bank of America confirms what many already suspected: affordability—especially lower prices and more favorable mortgage rates—is at the top of their wish list.

The good news: signs are emerging that the market is responding. Prices are moderating in many regions, and mortgage rates have pulled back from their peaks. That doesn’t eliminate all the challenges—but it does reshape the landscape for buyers in 2025 and beyond.

In this article, we’ll dig into how these two core factors (prices and rates) are evolving, why it matters for you, and what steps you can take to navigate the shifting terrain. We’ll also include voice-friendly FAQs and tips so if someone asks, “Is it a good time to buy a home now?” your content can be discoverable by voice assistants.

What Buyers Say They Need: Affordability Tops the List

When asking prospective buyers what would give them more confidence to act, the answers are unsurprising yet revealing: lower home prices and better borrowing costs.

In fact, one survey found that only about 28 % of homes are affordable to the “typical” household under current standards. Realtor That paints a stark picture: for many, the obstacle isn’t just motivation or timing—it’s the math.

So let’s look at how each major lever—prices and rates—is trending in 2025.

Prices Are Moderating — Why That’s a Big Deal

From Double Digits to Single Digits

In the post-pandemic housing boom, many markets saw home prices rise by 15–20 % (or more) year over year. That kind of momentum became entrenched in buyer expectations. But in 2025, that pace is tempering.

Per the Fannie Mae Home Price Expectations Survey (Q3 2025), home price growth is expected to average 2.4 % in 2025 and 2.1 % in 2026. fanniemae.com That’s well below the double-digit jumps of recent years and closer to long-term sustainable norms.

Similarly, JP Morgan’s outlook estimates about 3 % price growth for 2025. JPMorgan Chase This suggests that many markets may shift from “too hot” to “just warm.”

Regional Variation Is Real

Not every market will follow the national average. While many large and fast-growing metros may still see modest gains, slower markets or those with oversupply could see flat or even slightly negative movement. That’s why regionally localized insight is crucial.

Why Moderation Helps Buyers

-

Predictability: When you don’t have to chase double-digit gains, you can plan your budget more reliably.

-

Less fear of overpaying: Slower growth reduces the risk that you’ll wake up a year later and feel you “overpaid.”

-

Wage alignment: If wages inch upward, they have more room to catch up to home value growth.

-

Pressure easing: Sellers may be more willing to negotiate, especially in markets where demand softens.

Yet, moderation doesn’t equate to price declines everywhere—and in many regions, homes may still gain value, just at gentler rates.

Risks to Watch

-

Supply constraints: A shortage of new builds or tight inventory can still push prices upward.

-

Inflation and cost pressures: Rising materials, labor, or regulatory costs may bleed into home prices.

-

Local shocks: Economic shifts, job losses, or population changes in certain areas can alter trajectories.

Mortgage Rates Are Easing — But With Caveats

Current Landscape

Mortgage rates have recently seen a slight easing. As of early October 2025, the average 30-year fixed mortgage rate fell to 6.3 %, the lowest in about a year. AP News+1 That’s a modest bright spot compared to mid-2024 peaks above 6.7 %. The Mortgage Reports+1

Despite that easing, many potential buyers are still watching from the sidelines, wary of committing under uncertainty. Reuters+1

Forecasts & Projections

-

Fannie Mae now expects mortgage rates to end 2025 at 6.4 %, then drift lower toward 5.9 % in 2026. HousingWire+2fanniemae.com+2

-

NAHB / Mortgage Bankers Association (MBA) anticipate a 30-year fixed rate averaging in the mid-6 % range through most of 2025. Forbes

-

Some analysts caution that falling below 6 % before 2026 could be unlikely given inflation pressure and government deficits. CBS News

-

Others are more optimistic: lending experts tell CBS News they expect rates to modestly decline to 6.0–6.2 % by year end. CBS News

Why Even Small Drops Matter

-

A 0.25% reduction in interest rates can lower monthly payments significantly for a fixed loan over 30 years.

-

Lower rates expand purchasing power, allowing buyers to stretch budgets for better homes or locations.

-

They also reduce debt servicing stress and improve cash flow.

Risks & Uncertainty

-

Volatility: Mortgage rates are affected daily by bond yields, inflation data, and Fed signals—so daily moves can be bumpy.

-

Fed policy and inflation: If inflation remains sticky, rate cuts may stall or reverse.

-

Economic surprises: A stronger-than-expected jobs report or fiscal shock could push yields higher.

Why These Shifts Matter for You — The Buyer’s Context

Affordability Gets a Slight Breather

Moderating growth and lower rates don’t solve all affordability issues, but they offer some breathing room—especially in high-growth or overheated markets.

Negotiation Power Improves

Buyers may find homes staying on the market longer, giving more leverage in price and contract terms. In markets where sellers had the upper hand, that dynamic may shift.

Less “FOMO,” More Strategy

With cooling frenzy, you don’t need to rush. You can evaluate homes more deliberately, weigh offers, and avoid bidding wars unless warranted.

Lock-in Strategy Becomes More Important

Because rates still hover in the 6+ % range, locking in a favorable rate quickly can save you from downside surprises. The window to do so may not last forever.

What Should You Do Now? A Buyer’s Playbook

Here’s a step-by-step guide to act wisely in this evolving market:

1. Get Your Finances in Order

-

Clean up your credit, reduce debt, build reserves.

-

Work with a trustworthy lender to prequalify or get preapproved.

-

Stay abreast of changes in credit scoring or mortgage policy (e.g. Fannie Mae / Freddie Mac rules).

2. Monitor Local Market Data

Track:

-

Days on market

-

Listing discounts

-

Inventory levels

-

Price trends by neighborhood

This gives you signals about when to be aggressive or cautious.

3. Time Rate Locks Strategically

If your lender allows it, consider a rate lock, but be mindful of float-down options or costs tied to early locking.

4. Negotiate on More Than Price

Use favorable conditions to push on:

-

Closing costs

-

Inspection contingencies

-

Repairs

-

Flexible move-in or escrow timing

5. Be Selective in Market Entry

In markets where prices still climb, join the market thoughtfully rather than race recklessly. Choose homes that check both your needs and financial limits.

6. Stay Ready to Pivot

If a major rate drop or market dip emerges, be ready to act. But also avoid overcommitting until signals align.

7. Lean on Local Experts

Because much of this is local, having an agent who knows your specific city or ZIP code can help you translate national trends into smart moves.

What’s Ahead Into 2026 — A Look Forward

-

Further rate easing: Many forecasts suggest mortgage rates could drop below 6 % by late 2026. fanniemae.com+1

-

Continued, modest price growth: As per Fannie Mae and others, slow growth (2 %–3 %) may be the baseline, with upside in strong markets. fanniemae.com+1

-

More balanced markets: Buyers may gain more footing versus sellers, especially in areas where housing supply improves.

-

Local divergence: Expect some markets to outperform others—fast-growing regions may still post healthy gains.

FAQs (for Voice Search & Featured Snippets)

Q: Are home prices expected to fall in 2025?

A: In most markets, no. Experts forecast moderate growth — around 2–3 % nationally — rather than steep declines. Local variations may produce flat or slight dips in some areas.

Q: What is a realistic mortgage rate today?

A: As of October 2025, the average 30-year fixed mortgage rate is about 6.3 %. AP News+1 Analysts expect rates may settle around 6.4 % by year end. HousingWire+1

Q: When should I lock in a rate?

A: Lock when you feel your desired loan amount and approval are ready. If you see signs of rising rates, locking early may protect you. But always compare float-down or lock extension options.

Q: How much difference does a 0.5 % rate drop make in monthly payments?

A: For a $400,000 loan over 30 years, a 0.5 % lower rate can cut the monthly principal + interest payment by several hundred dollars. Over 30 years, that adds up substantially.

Q: Should I wait or act now if I plan to buy in the next year?

A: It depends. If rates dip significantly, waiting could benefit you—but you risk rising prices. If you find the right property and are ready, entering sooner with a solid rate may lock in value.

Conclusion / Bottom Line

The two biggest concerns buyers raise—prices and rates—are already showing signs of movement in 2025. While price growth is moderating and rates are easing, the challenges of affordability haven’t vanished entirely.

What is clear: the market’s tone is shifting. Buyers may find more breathing room, greater negotiation power, and more time to think through decisions. But volatility remains, and local conditions will matter more than ever.

If you’re considering a move—or trying to time your entrance—let’s connect. I can walk you through what’s happening in your area, help you interpret where things might head next, and map out a strategy that fits your goals and budget.

![]()

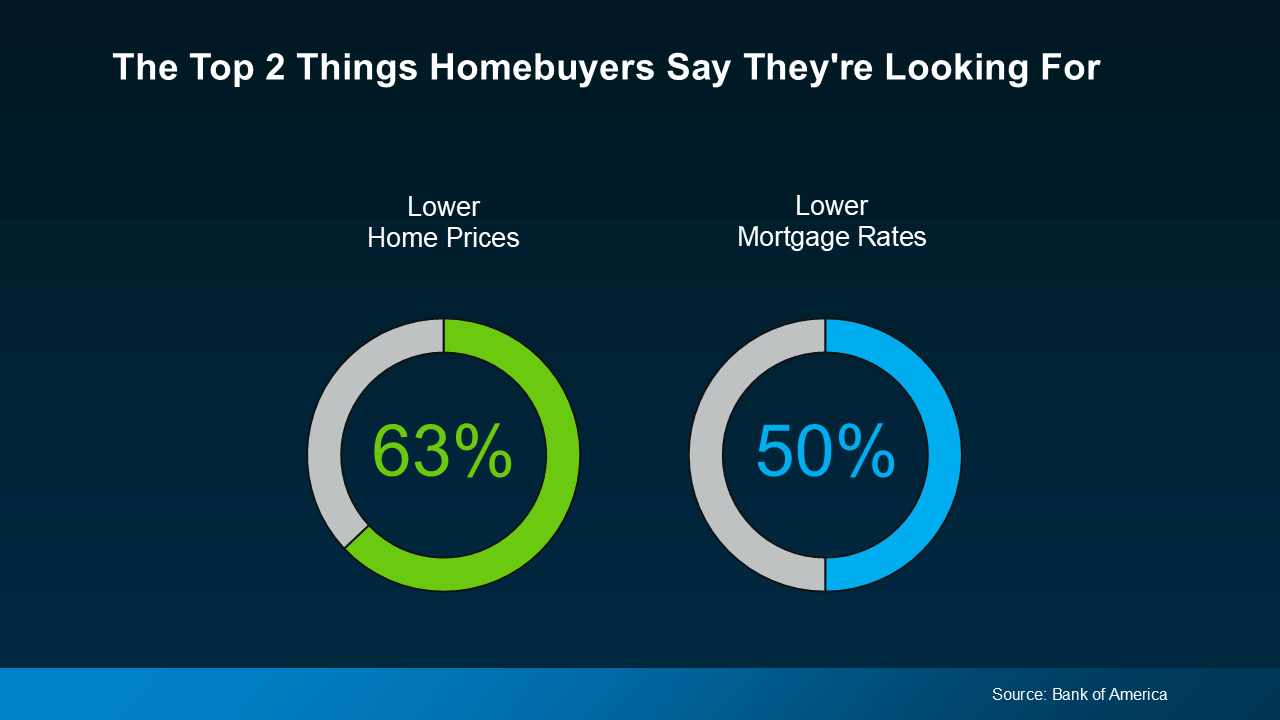

What Buyers Say They Need Most (And How the Market’s Responding)

A recent survey from Bank of America asked would-be homebuyers what would help them feel better about making a move, and it’s no surprise the answers have a clear theme. They want affordability to improve, specifically prices and rates (see below):

Here’s the good news. While the broader economy may still feel uncertain, there are signs the housing market is showing some changes in both of those areas. Let’s break it down so you know what you’re working with.

Here’s the good news. While the broader economy may still feel uncertain, there are signs the housing market is showing some changes in both of those areas. Let’s break it down so you know what you’re working with.

Prices Are Moderating

Over the past few years, home prices climbed fast, sometimes so fast it left many buyers feeling shut out. But today, that pace has slowed down. For comparison, from 2020 to 2021, prices rose by 20% in a 12-month period. Now? Nationally, experts are projecting single-digit increases this year – a much more normal pace.

That’s a sharp contrast to the rapid growth we saw just a few short years ago. Just remember, price trends are going to vary by area. In some markets, prices will continue to rise while others will experience slight declines.

Prices aren’t crashing, but they are moderating. For buyers, the slowdown makes buying a home a bit less intimidating. It’s easier to plan your budget when home values are moving at a much slower pace.

Mortgage Rates Are Easing

At the same time, rates have come down from their recent highs. And that’s taken some pressure off would-be homebuyers. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Slower price growth coupled with a slight drop in mortgage rates will improve affordability and create a window for some buyers to get into the market.”

Even a small drop in mortgage rates can mean a big difference in what you pay each month in your future mortgage payment. Just remember, while rates have come down a bit lately, they’re going to experience some volatility. So don’t get too caught up in the ups and downs.

The overall trend in the year ahead is that rates are expected to stay in the low to mid-6s – which is a lot better than where they were just a few short months ago. They may even drop further, depending on where the economy goes from here.

Why This Matters

Confidence in the economy may be low, but the housing market is showing signs of adjustment. Prices are moderating, and rates have come down from their highs.

For you, that may not solve affordability challenges altogether, but it does mean conditions look a little different than they did earlier this year. And those shifts could help you re-engage as we move into next year.

Bottom Line

Both of the top concerns for buyers are seeing some movement. Prices are moderating. Rates are easing. And both trends could stick around going into 2026.

If you’re considering a move, let’s connect walk you through what’s happening in our area – and what it means for your plans.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice