57 Days on the Market Isn’t Slow. It’s Normal.

Introduction: Why Homes Taking Longer To Sell Isn’t a Problem

If you’re a homeowner asking, “Why is my home sitting on the market longer than expected?”—you’re not alone. The truth is, 57 Days on the Market Isn’t Slow. It’s actually a reflection of a healthier, more balanced real estate environment.

Over the past few years, the housing market moved at an unsustainable pace. Homes sold in days, often above asking price, leaving little room for negotiation. But today, the Market Clock has reset. The current Average Days On Market is stabilizing, and that’s good news for both buyers and sellers.

In markets like West Palm Beach, North Palm Beach, and Wellington, Florida FL, this shift is especially noticeable. With insights from the latest Monthly Housing Report and guidance from Christian Penner, a trusted Mortgage Broker, Mortgage Lender, Real Estate Agent, and Real Estate Advisor at America’s Mortgage Solutions (AMS), we’ll break down exactly what this means for you.

Understanding the New Normal: What 57 Days on Market Really Means

The Average Days On Market is one of the most important indicators in real estate. It measures how long a home typically takes to sell from listing to contract.

So, is 57 days too long?

Not at all.

In fact, historically speaking, 30 to 90 days has always been considered a normal selling timeframe. The ultra-fast market during the pandemic was the exception—not the rule.

Today’s Market Clock reflects:

- More balanced negotiations

- Better pricing strategies

- Increased buyer decision-making time

This normalization means Homes Taking Longer To Sell isn’t a red flag—it’s a sign of stability.

What the Latest Monthly Housing Report Reveals

The latest Monthly Housing Report highlights key trends shaping today’s real estate market:

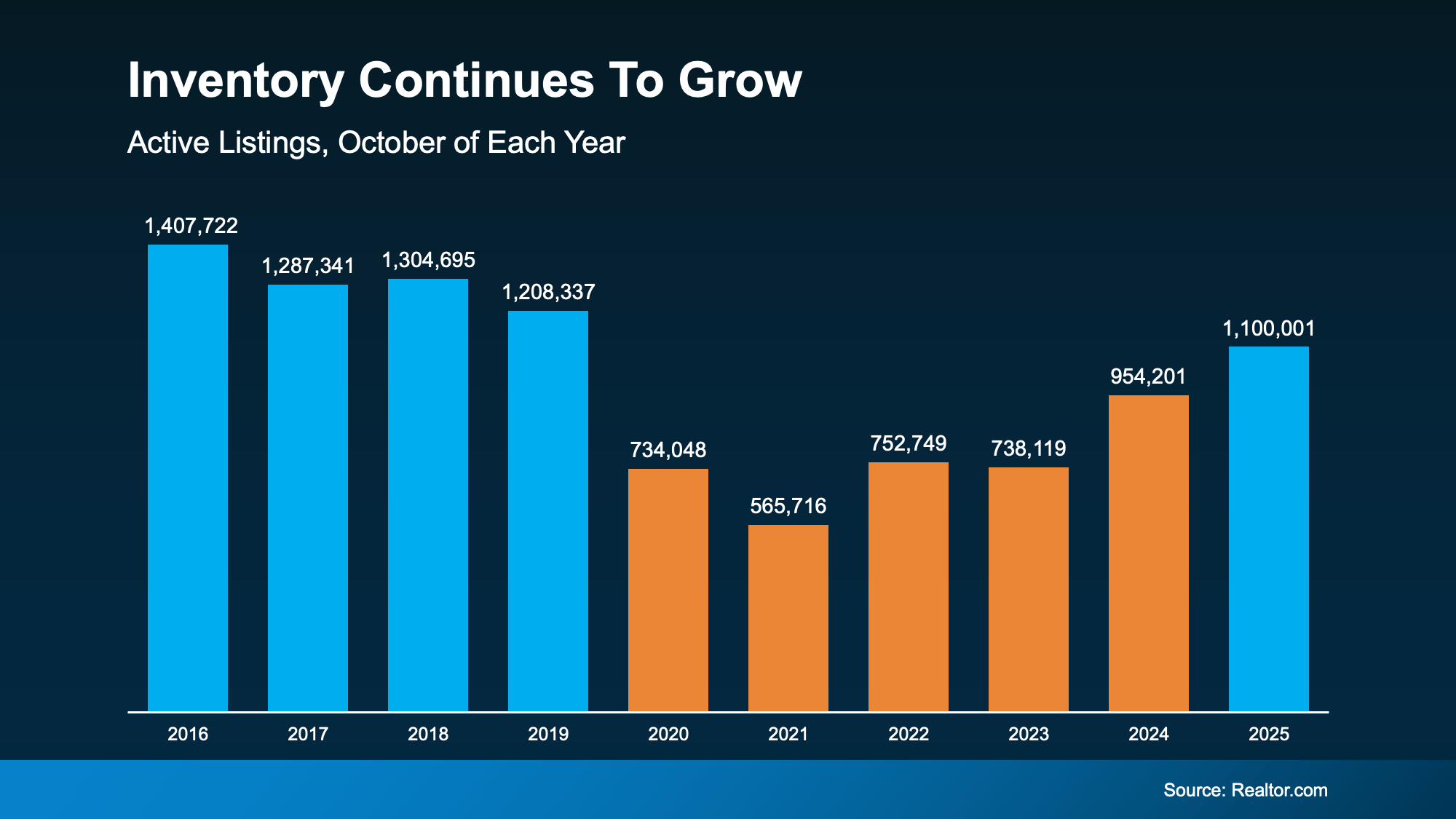

- Median list prices are declining year-over-year

- Inventory has increased for over two years

- Mortgage rates remain volatile but manageable

- Buyers are more selective and informed

This Data confirms that the market isn’t slowing—it’s adjusting.

For Homeowners, this means expectations need to shift. Instead of expecting instant offers, the focus should be on strategy, preparation, and pricing.

Why Homes Are Taking Longer To Sell in 2026

Rising Housing Supply Creates More Competition

One major factor is increasing Housing Supply. More listings mean buyers have more choices, which naturally extends the time it takes to sell a home.

In areas like Wellington, Florida FL, this is especially true, where new developments and listings are expanding options.

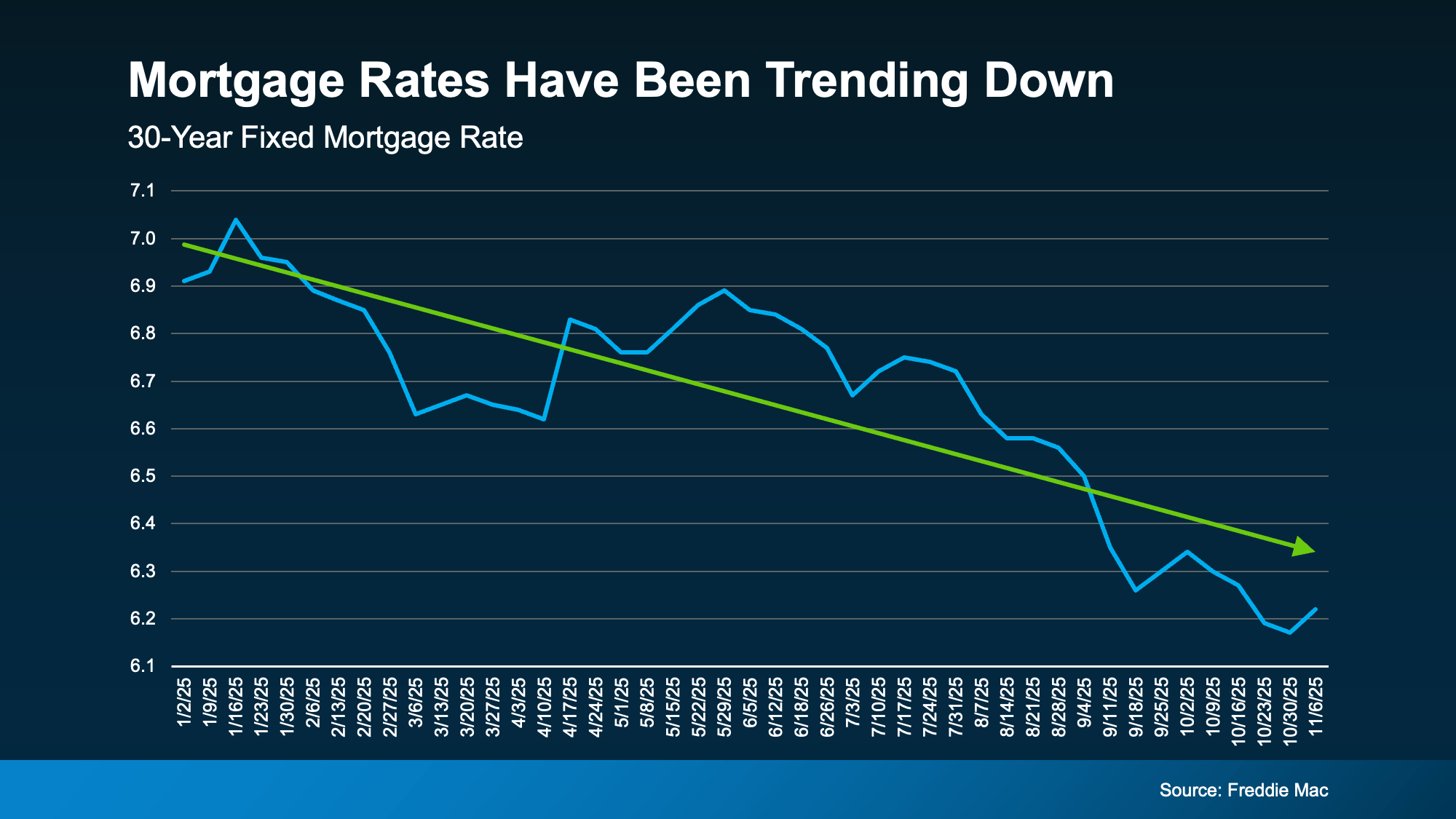

Mortgage Rates Influence Buyer Behavior

Mortgage rates have fluctuated in 2026, hovering around the 6% range. While still reasonable historically, they impact affordability and slow decision-making.

This doesn’t reduce Housing Demand—it simply makes buyers more cautious.

Economic Uncertainty Adds Hesitation

Global and economic uncertainties influence consumer confidence. Buyers are still active, but they’re taking more time to evaluate options.

This contributes to Homes Taking Longer To Sell, but doesn’t signal a weak market.

Housing Demand vs Housing Supply—Who Has the Advantage?

The balance between Housing Demand and Housing Supply is shifting.

- Buyers now have more negotiating power

- Sellers must be more strategic

- Inventory is improving but still tight in key regions

In North Palm Beach and West Palm Beach, demand remains strong due to lifestyle appeal, job growth, and migration trends. However, buyers are no longer rushing—they’re choosing wisely.

Why Pricing Strategy Matters More Than Ever

Price It Right From the Start

One of the most critical factors in today’s market is pricing.

Price It Right, and you attract serious buyers quickly. Overprice, and your home sits—leading to reductions that can hurt your final sale price.

Price It Right And Your House Will Sell

The latest Data shows that homes priced correctly from day one:

- Sell faster

- Require fewer price cuts

- Attract more competitive offers

This is where expert guidance becomes essential.

Local Market Insight: Florida Real Estate Trends

In West Palm Beach, North Palm Beach, and Wellington, Florida FL, the market reflects national trends—but with unique local advantages:

- Strong inbound migration

- High demand for lifestyle properties

- Continued long-term growth

Even with Homes Taking Longer To Sell, these markets remain resilient due to consistent Housing Demand.

Expert Insight: Christian Penner (AMS)

Navigating today’s market requires expertise. Christian Penner, a leading Mortgage Broker, Mortgage Lender, Real Estate Agent, and Real Estate Advisor at America’s Mortgage Solutions (AMS), provides valuable guidance for both buyers and sellers.

What Christian Recommends:

- Get pre-approved before listing or buying

- Understand financing options in a fluctuating rate environment

- Align pricing with current Market Outlook

- Use real-time Data to guide decisions

Working with a knowledgeable expert ensures you stay ahead of market trends.

Market Outlook for 2026: What’s Ahead

The current Market Outlook suggests:

- Continued inventory growth

- Stable but slightly elevated mortgage rates

- Moderate price adjustments

- Strong long-term demand

While challenges exist, the fundamentals remain solid. The market isn’t crashing—it’s recalibrating.

How to Sell Faster in Today’s Market

Even though 57 Days on the Market Isn’t Slow, you can still optimize your sale timeline:

1. Price Strategically

Use local Data and expert insights to Price It Right.

2. Enhance Presentation

Professional staging and photography increase buyer interest.

3. Market Effectively

Leverage digital platforms, social media, and local exposure.

4. Be Flexible

Accommodate showings and negotiate effectively.

Key Takeaways for Homeowners

- 57 Days on the Market Isn’t Slow—it’s normal

- The Market Clock has reset to healthier levels

- Homes Taking Longer To Sell reflects balance, not ضعف

- Housing Supply is rising, giving buyers more choices

- Price It Right And Your House Will Sell remains the golden rule

FAQs

Is 57 days on the market bad?

No. The Average Days On Market has normalized, and 57 days is well within a healthy range.

Why are homes taking longer to sell?

Increased Housing Supply, cautious buyers, and mortgage rate fluctuations all contribute.

What is the average days on market in 2026?

Around 50–70 days in many regions, depending on location and pricing.

How can I sell my home faster in Florida?

Focus on Price It Right, strong marketing, and working with experts like Christian Penner (AMS).

Should I lower my price if my home isn’t selling?

Not always. Review your strategy first—pricing, marketing, and condition all matter.

Conclusion: Strategy Over Speed

The real estate market has evolved. The days of instant sales are behind us—for now. But that’s not a bad thing.

57 Days on the Market Isn’t Slow. It’s a sign of a more thoughtful, balanced, and sustainable housing market.

For Homeowners in West Palm Beach, North Palm Beach, and Wellington, Florida FL, success today depends on understanding the Market Outlook, leveraging accurate Data, and applying smart strategies.

And remember: Price It Right And Your House Will Sell.

Read from source: “America’s Mortgage Solutions (AMS)”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice