Mortgage Rates Just Saw Their Biggest Drop in a Year — What It Means for You

Meta Description

Mortgage rates plunged to their lowest level since October 2024, marking the sharpest drop in over a year. Discover what caused it, how it affects homebuyers, refinancing, and whether now is the time to act.

Introduction: A Breakthrough Buyers Have Been Waiting For

For months, buyers and homeowners alike have been stuck watching mortgage rates hover near stubborn highs. But last week, something shifted — in a big way. On Friday, September 5, 2025, the average 30-year fixed mortgage rate fell to its lowest point since October 2024, marking the largest single-day decline in over a year.

This wasn’t just a routine fluctuation. It was the kind of market movement that instantly changes affordability, reignites refinancing interest, and makes would-be homebuyers ask: Is now the time to act?

Why Did Mortgage Rates Drop So Sharply?

The Jobs Report Sparked It All

The immediate catalyst for the plunge was the August jobs report, which came in weaker than expected — for the second month in a row. Job creation slowed, unemployment ticked slightly higher, and wage growth softened.

Why does this matter for mortgage rates? Because weak labor data signals a cooling economy, which:

-

Reduces inflation pressure.

-

Increases the likelihood that the Federal Reserve will cut rates sooner rather than later.

-

Pushes investors into safer assets like U.S. Treasuries, lowering yields.

Since mortgage rates tend to track 10-year Treasury yields, those falling yields quickly translated into lower borrowing costs.

Inflation Expectations & Market Sentiment

For much of 2024, inflation was the Fed’s primary concern. High inflation = higher interest rates. But now, momentum is shifting:

-

Inflation has shown consistent signs of cooling since mid-2025.

-

Bond markets are pricing in slower growth, which reduces inflationary risks.

-

Investors are anticipating a more accommodative Fed.

As expectations change, so do mortgage rates.

The Global Economic Context

It’s not just the U.S. Domestic trends play the biggest role, but global conditions amplify shifts. Factors like:

-

European economic slowdown dragging bond yields lower globally.

-

Energy prices stabilizing, reducing cost-push inflation.

-

China’s sluggish recovery, contributing to lower global demand.

All of these dynamics add downward pressure on U.S. long-term interest rates — and, by extension, mortgages.

How This Drop Affects Buyers Right Now

Monthly Payment Savings

Imagine you were shopping for a home in May 2025, when mortgage rates hovered near 7%. On a $400,000 loan, your principal and interest payment would have been around $2,660/month.

At today’s average of 6.5%, that drops closer to $2,460/month — saving $200 per month, or nearly $2,400 a year.

That difference can be the key factor that turns “too expensive” into “affordable enough.”

Increased Buying Power

Instead of saving the $200/month, you might decide to increase your budget. At lower rates, you could afford roughly $25,000–$30,000 more home while keeping your monthly payment the same.

For first-time buyers, that could mean:

-

Expanding your search into more desirable neighborhoods.

-

Affording a bigger home with more space or amenities.

-

Moving sooner than expected because affordability just improved.

Psychological Shift in the Market

Markets aren’t just numbers; they’re psychology. For months, headlines about “stubbornly high mortgage rates” discouraged buyers. Now, “biggest drop in a year” may shift sentiment:

-

Buyers who paused their search may jump back in.

-

Sellers may feel renewed urgency to list before rates dip even further and bring in more competition.

What This Means for Current Homeowners

Refinancing Is Back on the Table

If you bought or refinanced in the past two years, chances are your rate was higher than today’s 6.5%. Even a drop of half a percent can be worth thousands over the life of a loan.

Example: On a $350,000 loan, reducing the rate from 7.0% to 6.5% cuts payments by about $115/month, or $1,380/year.

Cash-Out Refinance Opportunities

With home values still high, some owners may consider a cash-out refinance to tap into equity for renovations, debt consolidation, or investments — all while lowering their rate.

Shortening Loan Terms

Lower rates also make it more affordable to switch from a 30-year to a 15-year loan, shaving years off repayment and saving on total interest.

Will Rates Keep Dropping?

Key Factors to Watch

-

Federal Reserve policy: If inflation data continues to cool, the Fed could begin cutting rates as early as late 2025.

-

Jobs market trends: Continued weakness could push mortgage rates even lower.

-

Inflation reports: Any surprise uptick could stall or reverse progress.

Expert Forecasts

Industry experts are cautiously optimistic:

-

MBA (Mortgage Bankers Association) predicts rates may stabilize around 6.0–6.2% by early 2026.

-

Fannie Mae expects more volatility but sees a general downward trajectory.

-

Independent economists warn that geopolitical events or unexpected inflation could quickly shift conditions.

In short: rates may not plunge back to pandemic lows of 3%, but they may gradually ease lower through the coming months.

Practical Steps Buyers Should Take Now

-

Get Pre-Approved Immediately

Rates can shift quickly. Pre-approval locks in what you can afford today. -

Ask About Rate Locks with Float-Down Options

This lets you secure today’s rate but benefit if rates drop before closing. -

Work Closely with a Local Agent

They’ll help you spot opportunities as more buyers reenter the market. -

Consider Refinancing Even if You Bought Recently

If your rate is more than 0.5% above current averages, refinancing may save money.

Historical Context: How Today’s Drop Compares

Mortgage rates have always been tied to broader economic shifts. A quick look back shows perspective:

-

1980s: Rates peaked above 18%.

-

2000s: Averages ranged between 6–8%.

-

2020–2021: Pandemic lows dropped near 3%.

-

2022–2024: Rapid inflation sent rates back above 7%.

Today’s 6.5% range feels high compared to pandemic lows but historically, it’s still moderate. The real story is how much more affordable homes become when rates move even half a point lower.

Frequently Asked Questions

Will mortgage rates keep falling in 2025?

Possibly. If inflation continues to cool and the economy weakens, rates could ease further into the 6.0% range.

Should I wait to buy a home until rates drop more?

Waiting is risky. Prices may rise as more buyers return. Locking in today’s lower rate with a float-down option balances both.

Is now a good time to refinance?

Yes, if your current rate is at least 0.5–1.0% higher than today’s averages. Even a small difference can save thousands.

Can mortgage rates drop back to 3%?

Highly unlikely. Those levels were fueled by extraordinary pandemic policies. Experts expect rates to settle between 5.5–6.5% in coming years.

How do mortgage rates affect home prices?

Lower rates = more affordability = more demand. That often supports price growth, especially in competitive markets.

Conclusion: A Rare Opening for Buyers & Homeowners

After months of little movement, mortgage rates just made their biggest drop in over a year. For buyers, that means improved affordability. For homeowners, it means refinancing opportunities are back. And for the market as a whole, it signals a new chapter — one where affordability, confidence, and opportunity may finally align.

Don’t wait for the “perfect” rate. If today’s numbers bring a home within reach — or create meaningful savings on your loan — it may be the moment you’ve been waiting for.

![]()

Mortgage Rates Just Saw Their Biggest Drop in a Year

You’ve been waiting for what feels like forever for mortgage rates to finally budge. And last week, they did – in a big way.

On Friday, September 5th, the average 30-year fixed mortgage rate fell to the lowest level since October 2024. It was the biggest one-day decline in over a year.

What Sparked the Drop?

According to Mortgage News Daily, this was a reaction to the August jobs report, which came out weaker-than-expected for a second month in a row. That sent signals across the financial markets, and then mortgage rates came down as a result.

Basically, we’re seeing signs the economy may be slowing down, and as certainty grows in the direction the economy is going, the markets are reacting to what is likely ahead. That historically brings mortgage rates down.

Why Buyers Should Pay Attention Now

But this isn’t just about one day of headlines or one report. It’s about what the drop means for you.

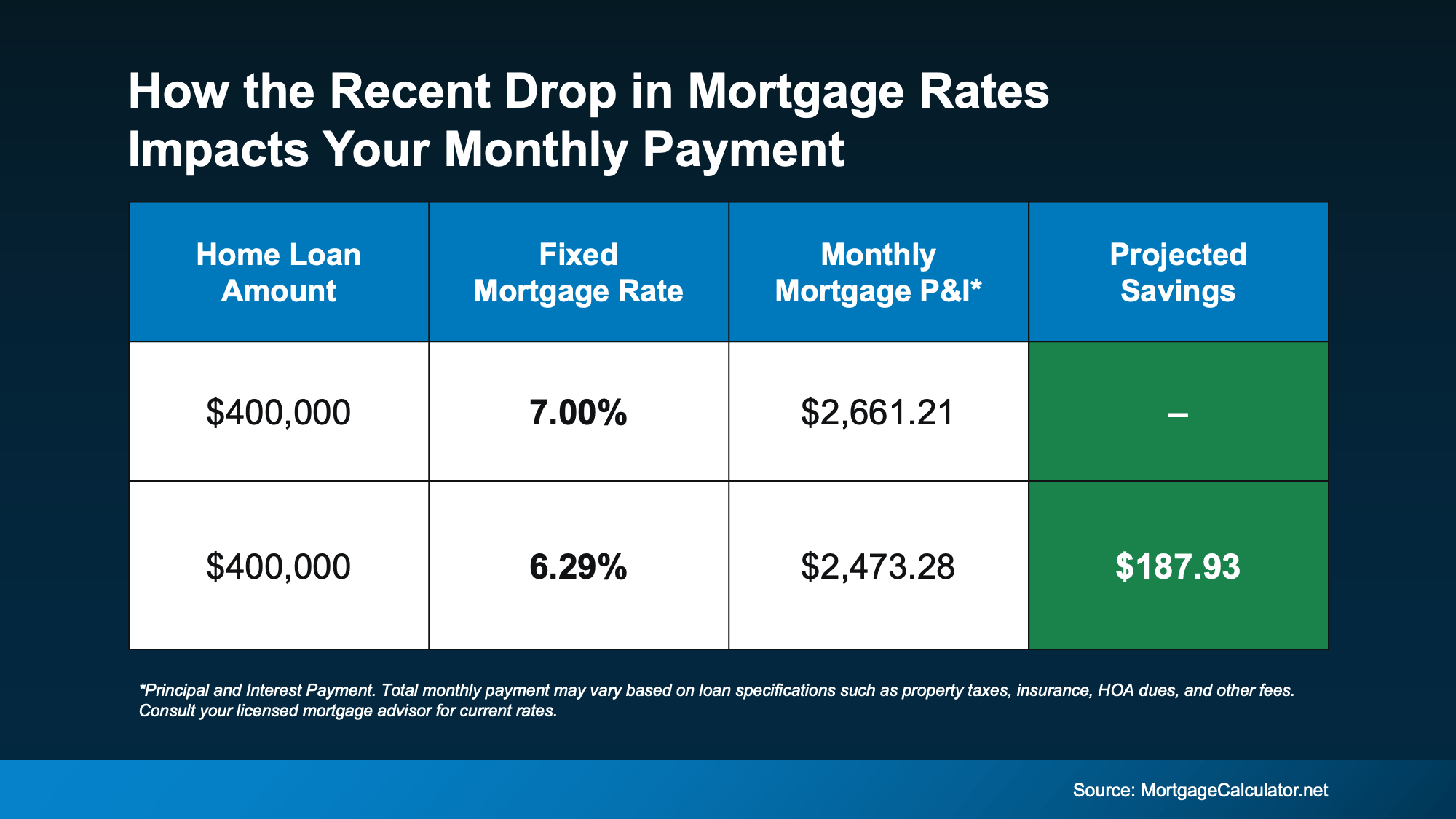

This recent change saves you money when you buy a home. The chart below shows you an example of what a monthly mortgage payment (principal and interest) would be at 7% (where mortgage rates were in May) versus where rates roughly are now:

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

How Long Will It Last?

That really depends on where the economy and inflation go from here. Rates could drop lower, or they could inch up slightly.

So, make sure you’re connected with a good agent and trusted lender. They’ll keep a close eye on inflation indicators, job market updates, and reactions to upcoming Fed policy to gauge where mortgage rates may go from here.

But for now, focus on this. While no one can say for sure where rates are headed, the fact that rates broke out of their months-long rut is a good thing. If you’ve been feeling stuck, this could make the start of a new chapter. As Diana Olick, Senior Real Estate and Climate Correspondent at CNBC, says:

“Rates are finally breaking out of the high 6% range, where they’ve been stuck for months.”

And that’s gives you more reason to hope than you’ve had in quite some time.

Bottom Line

This is the shift you’ve been waiting for.

Mortgage rates just saw their biggest decline in over a year. And if rates stay near this level, it could make a home you couldn’t afford just a few months ago feel possible again.

What would today’s rates save you on your future monthly payment? Let’s connect so you can find out.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice