What Mortgage Delinquencies Tell Us About the Future of Foreclosures

Meta Description:

Are rising mortgage delinquencies a warning sign of another foreclosure crisis? Explore 2025 housing market trends, FHA loan stress, foreclosure data, and why experts say this isn’t another 2008 crash.

Introduction: Rising Foreclosure Headlines—Should You Worry?

If you’ve been reading the news lately, you may have noticed headlines suggesting foreclosures are on the rise. Understandably, this can bring back memories of the 2008 housing crash, when millions of homeowners lost their homes.

But here’s the reality: today’s foreclosure numbers are nowhere near crisis levels. While mortgage delinquencies and foreclosures have risen slightly in 2025, experts emphasize that the housing market is fundamentally stronger today.

In this in-depth guide, we’ll explore:

-

What mortgage delinquencies reveal about foreclosure risks.

-

Why FHA loans are showing the most stress.

-

Which regions are most affected.

-

Why today’s market conditions are vastly different from 2008.

-

What homeowners can do if they’re struggling with payments.

By the end, you’ll have a clear understanding of why rising delinquencies don’t point to a housing crash, and what to watch for in the months ahead.

Foreclosures Are Rising—But Still Historically Low

To understand where we stand today, let’s look at the numbers:

-

2007–2011 Housing Crash: Over nine million Americans went through a distressed sale (foreclosure, short sale, or deed-in-lieu).

-

2024 Foreclosure Activity: According to ATTOM, foreclosure filings dropped to 322,103 nationwide, which was a 10% decrease from 2023 and 35% below 2019 pre-pandemic levels.

-

2025 Mid-Year Data: In the first half of 2025, filings rose slightly to 187,659, up 5.8% year-over-year.

Yes, foreclosures are up from last year—but they remain dramatically lower than during the last housing crash.

👉 Friendly Answer: “Are foreclosures as bad as 2008?”

Answer: No. Foreclosure numbers today are far lower than 2008, and lending standards are much stronger.

Why Mortgage Delinquencies Are an Early Warning Signal

Mortgage delinquencies—when homeowners fall 30 or more days behind on payments—are closely tracked by industry experts. They act as an early warning system for future foreclosure activity.

Current Delinquency Rates (Q2 2025):

-

Overall delinquency rate: 3.93%

-

Historic average (1979–present): 5.21%

-

Q1 2025: 4.04% (slight uptick due to early-stage delinquencies)

This means that, despite small fluctuations, the overall market is healthier than average.

Breaking Down Types of Delinquencies

Not all delinquencies are equal. Here’s a breakdown:

-

Early-Stage Delinquencies (30–59 days late): Often temporary, caused by short-term financial strain. Many homeowners recover.

-

Mid-Stage Delinquencies (60–89 days late): A more serious sign of trouble. Some recover, but risk increases.

-

Serious Delinquencies (90+ days late): Strongest predictor of future foreclosure.

As of mid-2025, serious delinquency rates remain low for conventional loans, but FHA loans are showing notable increases.

FHA Loans Under Pressure: Why They’re Struggling

FHA loans—backed by the Federal Housing Administration—are designed to help first-time and lower-income buyers. They require smaller down payments and more flexible credit standards. But these benefits come with risks:

-

Higher borrower vulnerability: FHA borrowers tend to have less financial cushion.

-

Greater exposure to inflation: Rising prices for food, gas, and insurance hit FHA borrowers harder.

-

Student loan overlap: FHA borrowers are more likely to also be behind on student loan payments.

Key 2025 FHA Loan Data:

-

12% of U.S. mortgages are FHA-backed.

-

But FHA loans now account for 38% of all delinquent balances (30+ days past due).

-

Serious FHA delinquencies: rose to 4.8% by early 2025 (highest since 2017 outside the pandemic).

-

June 2025 spike: FHA delinquency rate jumped 41 basis points in one month.

👉 Voice Search Q&A: “Why are FHA loans more at risk right now?”

Answer: Because FHA borrowers are more sensitive to inflation, rising insurance premiums, and debt burdens like student loans.

Regional Hotspots: Why the South Leads in FHA Stress

Not all regions are equally affected. FHA loan concentrations are highest in the South, particularly in:

-

Florida

-

Georgia

-

North Carolina

-

Texas

Why the South Is More Affected:

-

Higher insurance costs due to climate risks like hurricanes and flooding.

-

Lower median incomes compared to coastal markets, making FHA loans more common.

-

Local economies more vulnerable to job market shifts.

According to the Federal Reserve Bank of New York, states with more FHA loans are showing higher delinquency rates.

👉 Voice Search Q&A: “Which states have the most FHA delinquencies?”

Answer: Southern states like Florida, Georgia, and North Carolina show the highest concentrations.

Economic Factors Driving Delinquencies

Several broader economic pressures are contributing to rising FHA delinquencies:

-

Inflation: Even as inflation cools slightly, food, utilities, and household expenses remain elevated.

-

Rising Insurance Costs: Homeowners in high-risk states are paying thousands more per year, sometimes pushing budgets over the edge.

-

Job Market Softness: While unemployment remains low, certain industries (tech, retail, manufacturing) have seen layoffs.

-

Debt Pressures: Student loan delinquency rates topped 10% in 2025, creating overlap with mortgage stress.

Why This Isn’t 2008 All Over Again

Here’s why experts stress that today’s situation is very different from the last housing crisis:

-

Stricter lending standards: Post-2008 regulations prevent risky lending practices.

-

Record homeowner equity: Homeowners collectively hold trillions in tappable equity, giving them options to sell before foreclosure.

-

Conventional loan strength: Conventional mortgages have historically low delinquency rates.

-

Localized stress: Problems are concentrated in FHA loans, not the entire market.

👉 Voice Search Q&A: “Could mortgage delinquencies cause another housing crash?”

Answer: No. Today’s mortgage market is stronger, with stricter lending rules and higher equity levels.

Policy and Industry Responses

Government agencies and mortgage servicers are watching these trends closely.

-

HUD & FHA: Offering repayment plans, loan modifications, and foreclosure prevention programs.

-

VA Loans: Transition away from the VA Servicing Purchase (VASP) program could increase stress for some veterans.

-

Federal Reserve: Monitoring household debt as part of broader financial stability assessments.

These measures are designed to prevent localized stress from turning into a systemic issue.

What Homeowners Can Do If They’re Struggling

If you’re worried about missing mortgage payments, here are practical steps to protect your home:

-

Contact Your Servicer Immediately

-

Ask about repayment plans or forbearance.

-

-

Explore Loan Modification Options

-

Lower interest rates, extended terms, or principal adjustments.

-

-

Leverage Equity Before Foreclosure

-

If you have equity, selling may allow you to avoid foreclosure entirely.

-

-

Seek HUD-Approved Counseling

-

Free or low-cost advice on mortgage assistance programs.

-

-

Check for State or Local Programs

-

Some states offer homeowner assistance funds.

-

Forecast: What Experts Expect for 2026

Housing analysts project:

-

Foreclosure activity may rise modestly, especially in FHA-heavy markets.

-

No systemic crisis expected, thanks to conventional loan stability and equity cushions.

-

Regional differences will remain important—some Southern states may see elevated stress, while coastal states remain steady.

-

Household debt burdens (student loans, credit cards) could continue influencing mortgage delinquency trends.

Bottom Line: Rising FHA Delinquencies Are Worth Watching, But No Crisis Ahead

Yes, mortgage delinquencies and foreclosures are ticking up. But today’s situation is fundamentally different from 2008.

-

FHA borrowers—especially in the South—are under pressure.

-

But conventional loans remain strong, and homeowners nationwide hold significant equity.

-

The overall foreclosure rate is still historically low.

👉 Key Takeaway: We’re seeing stress in a segment of the market, not a collapse of the housing system.

FAQs: Mortgage Delinquencies and Foreclosures in 2025–2026

Q1: Are foreclosures going up in 2025?

Yes, slightly—but they’re still far below 2008 levels.

Q2: Which loans are most at risk right now?

FHA loans, especially in Southern states, are showing the most stress.

Q3: Will rising delinquencies cause another housing crash?

No. The broader mortgage market is stable, and equity levels protect homeowners.

Q4: Why are FHA loans struggling more than others?

Because FHA borrowers are more vulnerable to inflation, insurance costs, and debt burdens.

Q5: What can I do if I can’t pay my mortgage?

Contact your servicer immediately, explore repayment or modification options, and consider selling if you have equity.

Q6: Is this similar to 2008?

No. Lending standards are stricter, and most homeowners today have strong financial cushions.

Q7: Which regions have the most FHA loans?

The South, especially Florida, Georgia, and North Carolina.

Q8: How do rising insurance costs affect mortgage payments?

Higher premiums increase monthly costs, pushing some FHA borrowers into delinquency.

Q9: What role does student loan debt play?

Many FHA borrowers behind on mortgages are also delinquent on student loans, adding financial strain.

Q10: Will foreclosures rise again in 2026?

Analysts expect modest increases but no widespread crisis.

– – –

![]()

What Mortgage Delinquencies Tell Us About the Future of Foreclosures

You may be seeing headlines about how foreclosures are rising. And if that makes you nervous that we’re headed for another crash, here’s what you should know.

According to ATTOM, during the housing crash, over nine million people went through some sort of distressed sale (2007-2011). Last year, there were just over 300,000.

So, even with the increase lately, we’re talking about numbers that are dramatically lower. But what does the future hold? Is a wave coming? The short answer is, no.

Here’s why. Experts in the industry look at mortgage delinquencies (loans that are more than 30 days past due) as an early sign for potential foreclosures down the line. And the latest data for delinquencies is reassuring about the market overall.

Right now, delinquencies as a whole are consistent with where we ended last year, which means we’re not seeing the kind of increase that would signal widespread trouble.

But there are some key indicators to continue to watch. Marina Walsh, Vice President of Industry Analysis at the Mortgage Bankers Association, explains:

“While overall mortgage delinquencies are relatively flat compared to last year, the composition has changed.”

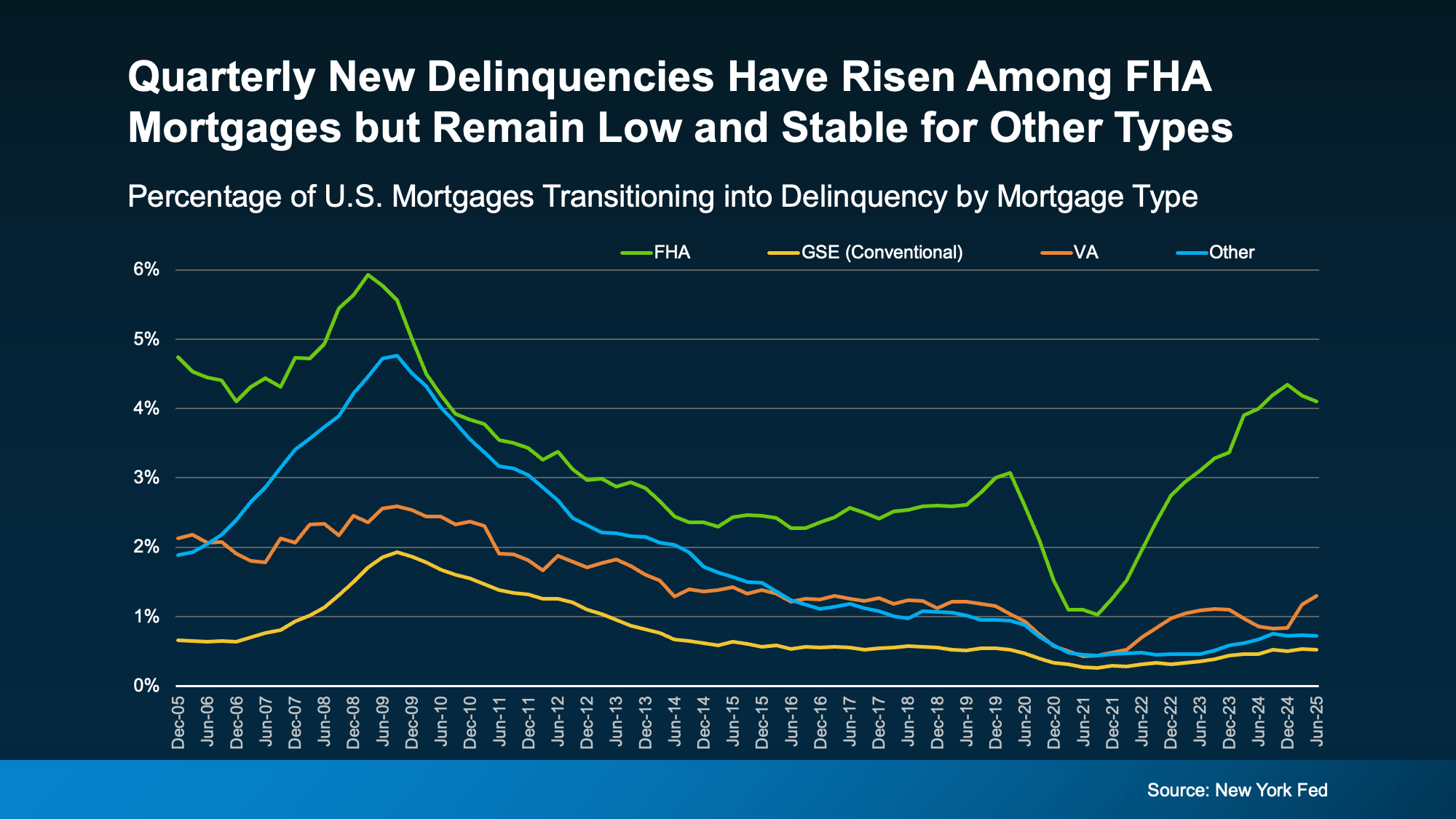

Right now, borrowers with FHA mortgages currently make up the biggest share of new delinquencies (see graph below):

And here’s why that may be happening. Borrowers with FHA mortgages may be more sensitive to shifts in the economy. And with recession fears, stubborn inflation, employment challenges, and more, it makes sense this segment of the market may be feeling it a bit more. But that doesn’t mean it’s a signal a crash is coming.

And here’s why that may be happening. Borrowers with FHA mortgages may be more sensitive to shifts in the economy. And with recession fears, stubborn inflation, employment challenges, and more, it makes sense this segment of the market may be feeling it a bit more. But that doesn’t mean it’s a signal a crash is coming.

If you look back at the graph, it shows, while there are more FHA loans experiencing hardship than the norm, delinquency rates for other loan types remain low and stable. Back during the crash, delinquency rates were significantly elevated for all 4 categories.

That means the broader mortgage market is on much stronger footing than it was back in 2008. As ResiClub says:

“The recent uptick in mortgage delinquency seems to be concentrated among FHA borrowers, however, mortgage performance remains very solid when viewed in light of the twenty-year history of our data.”

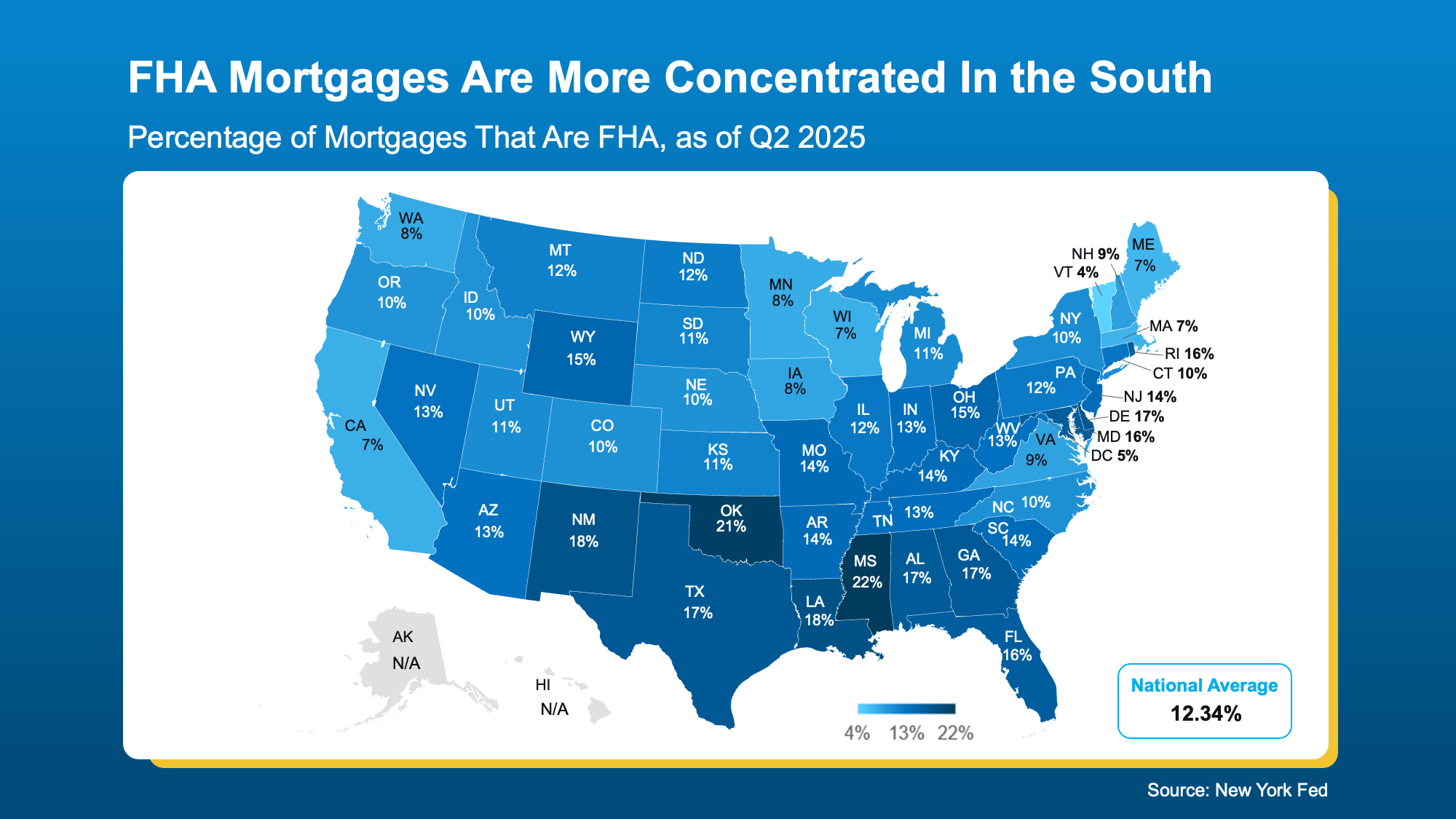

The Region with the Most FHA Loans

Here’s another reason this isn’t a signal of trouble ahead. FHA loans only make up about 12% of all home loans nationwide. But like anything else in housing, local data matters. There are some regions of the country where there are more of this type of loan than others, particularly the South.

The map below does not show how many FHA loans are delinquent. It just shows the overall concentration of FHA loans by state, so you can see which regions have the greatest volume (see map below):

As the Federal Reserve Bank of New York explains:

As the Federal Reserve Bank of New York explains:

“Looking at geographic concentrations of loans, recent data indicate that a higher proportion of mortgage balances are delinquent in many of the southern states . . . we see that higher delinquency rates coincide with a higher share of FHA loans across states.”

Just remember, even the delinquencies rates we’re seeing now aren’t as high as they were in 2008. Again, this is not a signal of a crisis. But it is something experts will monitor in the months ahead.

If You’re Experiencing Financial Hardship

No one wants to see anyone face the challenges of foreclosure. But just know that, if you’re a homeowner struggling with payments, you’re not alone – and you do have options.

The first step is reaching out to your mortgage provider. In many cases, you may be able to set up a repayment plan or explore loan modifications to help you stay on track. And for many homeowners today, you may also have enough equity to sell your house and avoid foreclosure. Odds are, at least some of these delinquencies will go that route since homeowners today have near record amounts of equity in their homes. It may be worth seeing if that could be an option for you too.

Bottom Line

Foreclosures are rising slightly, but they’re nowhere near the levels of 2008. And delinquency trends don’t point to a crash ahead.

This is something industry professionals are going to watch in the days ahead. If you want to stay up to date, let’s connect so you always have the latest information.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice