Why Experts Expect Mortgage Rates to Ease Over the the Next Year

You want mortgage rates to fall—and lately, they’ve begun to. But will that trend hold? Could rates slip meaningfully lower? Experts believe there’s potential, thanks to the behavior of the 10-year Treasury yield, a narrowing mortgage spread, and evolving macro conditions. Below, we break down why the outlook is cautiously optimistic—and what could derail it.

Meta Information

Title: Why Experts Expect Mortgage Rates to Ease Over the Next Year

Meta Description: Mortgage rates historically track the 10-year Treasury yield. With that yield forecast to decline and the “spread” narrowing, many analysts expect mortgage rates could drift lower over the next year.

Target Keywords: mortgage rates forecast, 10-year Treasury, mortgage spread, interest rate outlook, mortgage rate decline

Voice Search Targets:

-

“Will mortgage rates go down in 2026?”

-

“Why do mortgage rates follow the 10-year Treasury?”

-

“What could stop mortgage rates from falling?”

Introduction: A Glimpse of Relief—and Why It Matters

You may have felt a bit of relief: mortgage rates have edged lower in recent weeks. But for many homebuyers, that’s only the beginning. Will rates indeed ease further? And if so, by how much?

Experts are pointing to two central forces that could push rates downward in the coming year:

-

A decline in the 10-year Treasury yield, long a benchmark for long-term borrowing costs

-

A narrowing of the mortgage “spread”, the extra premium lenders charge over that benchmark

Together, these dynamics suggest room for mortgage rates to drift downward—albeit gradually. In this article, you’ll learn:

-

How the 10-year Treasury yield and mortgage rates are linked

-

What the spread is and why it matters

-

How forecasts see these factors evolving

-

The caveats and risks that could hinder a drop

-

What this means practically for borrowers

Let’s start with the foundation: the long-term link between mortgage rates and the 10-year yield.

1. The Long-Term Link: Mortgage Rates and the 10-Year Treasury Yield

Why mortgage rates track the 10-year Treasury

Over decades, the 30-year fixed mortgage rate has generally moved in tandem with the 10-year U.S. Treasury yield. This relationship holds because both are long-term, fixed-income securities that compete for capital in markets. When Treasury yields rise, investors demand higher returns, pushing mortgage rates up. When Treasury yields fall, mortgage rates tend to follow.

Importantly, mortgage rates are more closely tied to long-term yields than to short-term policy rates like the federal funds rate. That’s because mortgage loans lock in interest for decades, so markets price them based on long-term risk and return expectations. Schwab Brokerage+1

How the “spread” completes the picture

Mortgage lenders build in an additional risk premium above the 10-year yield. That premium is known as the “mortgage spread.” Over long spans, that spread (30-year fixed rate minus the 10-year yield) averages about 1.7 to 1.8 percentage points (i.e. 170 to 180 basis points).

So a rough formula many analysts use is:

Mortgage Rate ≈ 10-Year Treasury Yield + Spread

Because of this, if you expect the 10-year yield to drop and the spread to compress, it implies downward potential for mortgage rates.

When the link breaks down—or widens

It’s not always a perfect correlation. During periods of economic stress or uncertainty, the spread can widen significantly. Why? Because lenders demand more compensation for risk, capital becomes scarcer, or investor appetite for mortgage-backed securities falls. The Richmond Fed has studied mortgage spreads and notes that they tend to spike in times of financial stress or recession, behaving as a measure of market risk and stress. Federal Reserve Bank of Richmond

In other words: when fear is high, the spread widens; when confidence returns, it contracts. That dynamic is central to how much downward room mortgage rates may have.

2. The Spread Has Been Wide—but It’s Starting to Shrink

What’s driven the wide spread lately

Over the past few years, the mortgage spread has been unusually wide compared to historical norms. Several factors contributed:

-

Heightened risk aversion: lenders demanded extra cushion for credit, market stress, or uncertainty

-

Quantitative tightening & de-risking by central banks: the U.S. Federal Reserve has allowed mortgage-backed securities rolls to unwind, reducing market support for the MBS market

-

Volatile macro outlook: inflation, rates, and economic volatility kept lenders defensive

Because of that, mortgage rates haven’t just tracked the 10-year yield—they’ve sat significantly above where the usual spread would imply.

Signs of compression in the spread

Now, however, market participants are seeing hints that the spread is narrowing. Some contributing factors:

-

Increasing demand for mortgage-backed securities (MBS), reducing risk premiums

-

Greater clarity on economic signals and inflation trending downward

-

Expectations of future Fed rate cuts easing tension in interest markets

As the spread tightens toward its historical range, even a stable or modestly falling 10-year yield could produce a meaningful drop in mortgage rates.

Interpreting the spread through the lens of duration

One advanced insight: when the yield curve is inverted or steep, mortgage durations shorten, meaning mortgages behave as if more “short term” in risk. This can exaggerate spread movements during stress. The Richmond Fed explains this as the “mortgage duration effect”, which helps explain why spreads tend to blow out during recessions. Federal Reserve Bank of Richmond

Thus, as confidence returns and curves normalize, one should see spreads move closer to historical norms.

3. Forecasts for the 10-Year Treasury Yield: What Analysts Expect

If mortgage rates are going to fall, the 10-year Treasury yield likely needs to move downward first (or at least not rise further). So what are forecasts saying?

Drivers that could push the yield down

-

Softening inflation expectations: If CPI and PCE inflation continue to moderate, bond markets will price lower future yields

-

Economic slowdown or recession risks: Weaker growth and rising recession fears push safe-haven demand into Treasuries

-

Fed rate cuts and dovish guidance: Markets anticipate rate cuts or a more dovish stance by the Fed, which can pull down long-term yields

-

Global capital flows & safe-haven demand: International investors seeking stable assets could buy U.S. Treasuries, raising prices and lowering yields

What the forecasts say

-

According to Investopedia, most analysts expect mortgage rates to remain in the mid-6% range during 2025, with a gradual slide toward the low-6% area by late 2026. Investopedia

-

Schwab projects that a 30-year fixed rate might fall to 6.4% by end-2025 and potentially to 5.9% by the end of 2026, assuming favorable conditions. Schwab Brokerage

-

Bank of America analysts argue that to reach something like a 5.0% mortgage rate, the 10-year yield might need to fall to 3.0–3.25%, which would require significant policy shifts, such as renewed Fed purchases of MBS or yield curve control. ResiClub

So while modest declines are broadly expected, a steep plunge would require uncommon moves in markets or monetary policy.

4. Mortgage Rate Scenarios & When Relief Could Occur

Let’s put this all together into scenarios mapped onto possible yield and spread outcomes.

Scenario Table: Yield, Spread & Implied Mortgage Rate

| Scenario | 10-Year Treasury Yield | Spread | Implied 30-Year Mortgage Rate | Description / Likelihood |

|---|---|---|---|---|

| Base case | ~ 4.0 % | ~ 1.7 pp | ~ 5.7–5.8 % | Comfortable but unspectacular easing |

| Moderate drop | ~ 3.8 % | ~ 1.6 pp | ~ 5.4 % | Good room, if inflation cools |

| Aggressive drop | ~ 3.5 % | ~ 1.5 pp | ~ 5.0 % | Challenging, requires strong policy moves |

| Stress reversal | ~ 4.3 % | ~ 1.9+ pp | ~ 6.2+ % | If inflation surprises or risk premiums return |

These aren’t predictions—they’re illustrative reference points based on the formula we discussed. But they help frame what’s possible if yields and spreads move in favorable or adverse directions.

When could this easing happen?

-

The short term (next 3–6 months) could see modest downward drift, if inflation data surprises to the downside or the Fed signals softer policy.

-

The mid-term (6–12 months) is the window where the real move might play out—assuming creeping confidence in the economy and rate cuts.

-

The longer term (into 2026–2027) offers the greatest potential for downward compression, but also the greatest uncertainty.

Many forecasts anticipate that mortgage rates won’t plunge abruptly but rather slide gradually. Investors and borrowers should prepare for incremental improvements rather than immediate, dramatic relief.

5. Risks & Caveats That Could Derail the Drop

We’ve laid out the case for potential easing—but there are significant risks. Any of these factors could stall or reverse the trend.

1. Inflation surprises

If inflation remains sticky or rebounds (due to supply shocks, energy, wages), bond markets will price in higher yields, pushing mortgage rates back up.

2. Policy missteps and Fed surprises

The Federal Reserve’s path is still subject to data. If the Fed signals tighter policy or keeps rates higher than expected, that can push long-term yields upward. Also, the timing and magnitude of rate cuts matter.

3. Broad market volatility or risk-off events

Geopolitical shocks, financial stress, or abrupt shifts in sentiment can cause spreads to widen again—even if the 10-year yield is stable.

4. Yield curve dynamics & duration effects

If the yield curve becomes inverted (short-term rates higher than long-term), mortgage durations shorten, and spreads may widen. That can blunt or reverse downward pressure. Federal Reserve Bank of Richmond

5. Weak demand for MBS or illiquidity in mortgage markets

If investors shy away from mortgage-backed securities or liquidity dries up, lenders may demand larger premiums, pushing spreads up—even amid falling Treasuries.

6. Timing, expectations, and forward pricing

Bond markets price what’s expected. If the decline in yields or spread compression is already “priced in,” borrowers may not benefit until further confirmation shows up in actual rate movements.

In short: the path to lower mortgage rates is not guaranteed, and volatility must be expected.

6. What This Means for Homebuyers, Refinancers & Borrowers

For prospective homebuyers

-

Even modest declines in mortgage rates can improve affordability—especially for those on the fence.

-

If you’re ready to buy, don’t wait for “perfect” rates: get preapproved, stay flexible, and monitor trends.

-

Rate drops may allow buyers to stretch their budget or opt for more favorable terms.

For homeowners considering refinancing

-

Keep a close eye on 10-year yields and spread movements—these will be early signals before lenders pass along rate cuts.

-

Small changes (e.g. 0.25–0.50%) can be worth acting on—balance closing costs and your remaining loan term.

-

If rates approach your break-even point, refinancing can become worthwhile.

For mortgage originators, lenders, and agents

-

Stay ahead of shifting spreads, yield curve cues, and investor demand for MBS.

-

Educate clients on realistic expectations and promote agility in decision-making.

-

Use data-driven forecasting models to anticipate local pricing impacts.

For financial planners and real estate professionals

-

Encourage clients to watch leading indicators (Treasury yields, inflation, Fed guidance).

-

Position content and messaging around “when mortgage rates will drop” or “forecast 2026 interest rates” to capture voice and search demand.

-

Prepare clients for volatility and manage expectations: relief may come, but it may not be smooth.

7. Voice Search / FAQ Section (Optimized for AEO & VSO)

Q: Why do mortgage rates follow the 10-year Treasury yield?

A: Mortgage loans are long-term fixed-rate instruments. Investors compare them to other long-term investments like the 10-year Treasury. When Treasury yields rise, borrowing costs increase, and mortgage rates tend to track that movement.

Q: What is the mortgage “spread”?

A: The spread is the extra premium that mortgage lenders add above the 10-year Treasury yield. It compensates for credit risk, servicing costs, prepayment risk, and liquidity. Historically, that spread hovers around 1.7 to 1.8 percentage points.

Q: How low could mortgage rates go in the next year?

A: In a favorable scenario—with a falling 10-year yield and narrowing spread—rates could drop into the mid-5% range (e.g. 5.4–5.8%). If conditions are very supportive, an upper-5% scenario (around 5.0–5.2%) is conceivable—but that’s more aggressive and depends on strong tailwinds.

Q: What could prevent mortgage rates from falling?

A: Stubborn inflation, tighter Fed policy, widening spreads (due to market stress), poor demand for mortgage-backed securities, or reversals in bond yields could all prevent or reverse declines.

Q: When should I refinance based on this outlook?

A: Monitor yield and spread trends. When mortgage rates approach or cross your break-even threshold (accounting for closing costs), that’s your window. Don’t wait for an ideal rate; act when the math works in your favor.

Conclusion & Next Steps

Mortgage rates have begun to soften. But whether that trend endures—and how far rates fall—depends heavily on the interplay between the 10-year Treasury yield and the mortgage spread.

If inflation continues easing, the economy remains stable, and markets regain confidence, then a gradual decline in rates over the next year is plausible. But there’s no guarantee. Risks like inflation surprises, policy shifts, or market turbulence could intervene.

![]()

Why Experts Say Mortgage Rates Should Ease Over the Next Year

You want mortgage rates to fall – and they’ve started to. But is it going to last? And how low will they go?

Experts say there’s room for rates to come down even more over the next year. And one of the leading indicators to watch is the 10-year treasury yield. Here’s why.

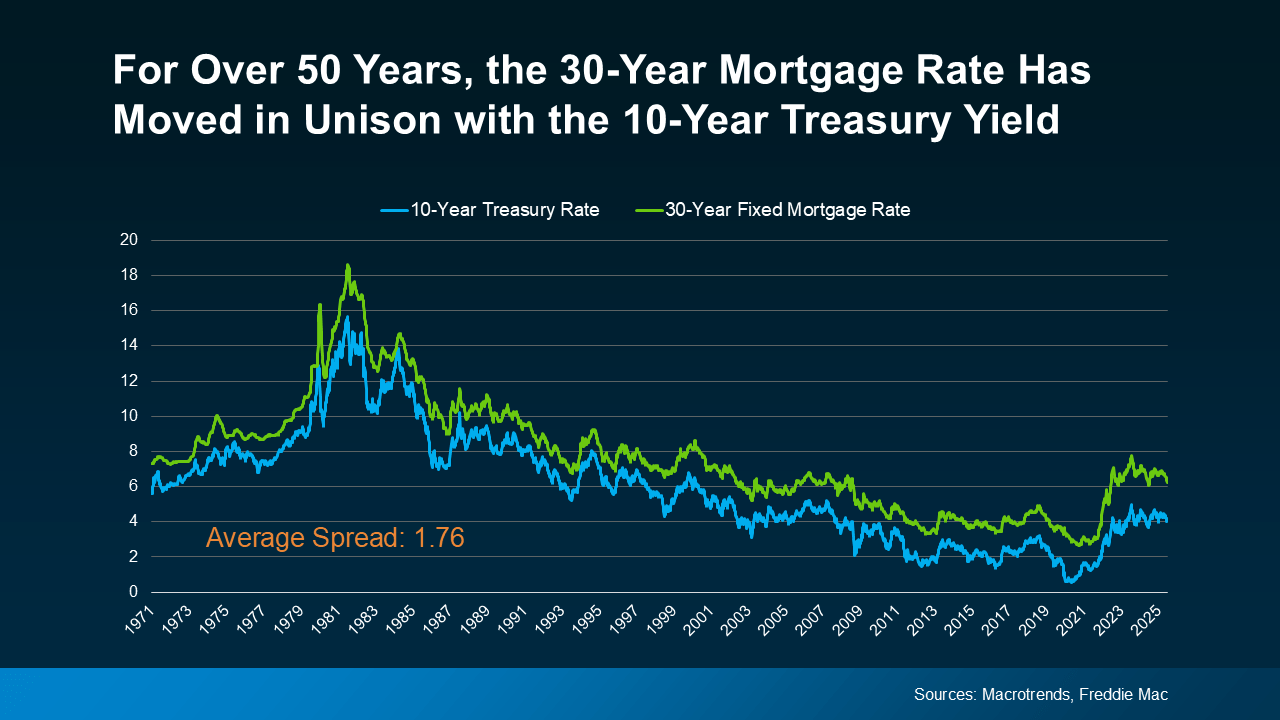

The Link Between Mortgage Rates and the 10-Year Treasury Yield

For over 50 years, the 30-year fixed mortgage rate has closely followed the movement of the 10-year treasury yield, which is a widely watched benchmark for long-term interest rates (see graph below):

When the treasury yield climbs, mortgage rates tend to follow. And when the yield falls, mortgage rates typically come down.

When the treasury yield climbs, mortgage rates tend to follow. And when the yield falls, mortgage rates typically come down.

It’s been a predictable pattern for over 50 years. So predictable, that there’s a number experts consider normal for the gap between the two. It’s known as the spread, and it usually averages about 1.76 percentage points, or what you sometimes hear as 176 basis points.

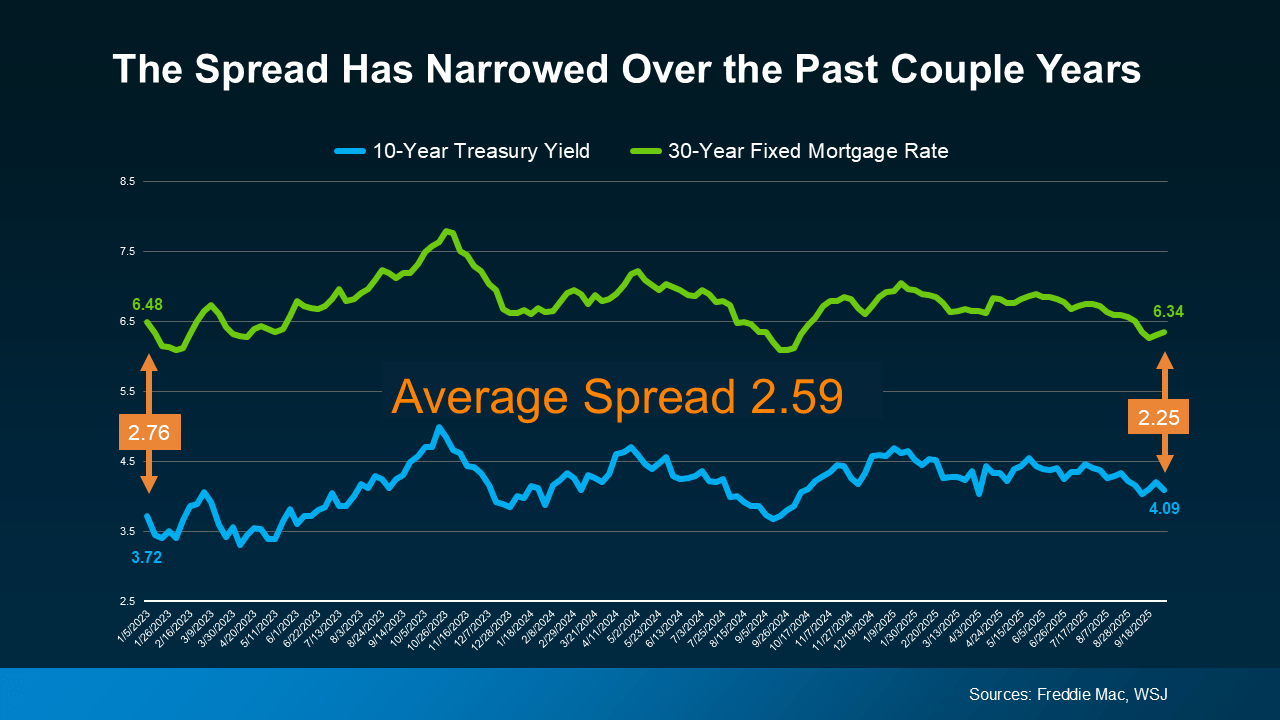

The Spread Is Shrinking

Over the past couple of years, though, that spread has been much wider than normal. Why? Think of the spread as a measure of fear in the market. When there’s lingering uncertainty in the economy, the gap widens beyond its usual norm. That’s one of the reasons why mortgage rates have been unusually high over the past few years.

But here’s a sign for optimism. Even though there’s still some lingering uncertainty related to the economy, that spread is starting to shrink as the path forward is becoming clearer (see graph below):

And that opens the door for mortgage rates to come down even more. As a recent article from Redfin explains:

And that opens the door for mortgage rates to come down even more. As a recent article from Redfin explains:

“A lower mortgage spread equals lower mortgage rates. If the spread continues to decline, mortgage rates could fall more than they already have.”

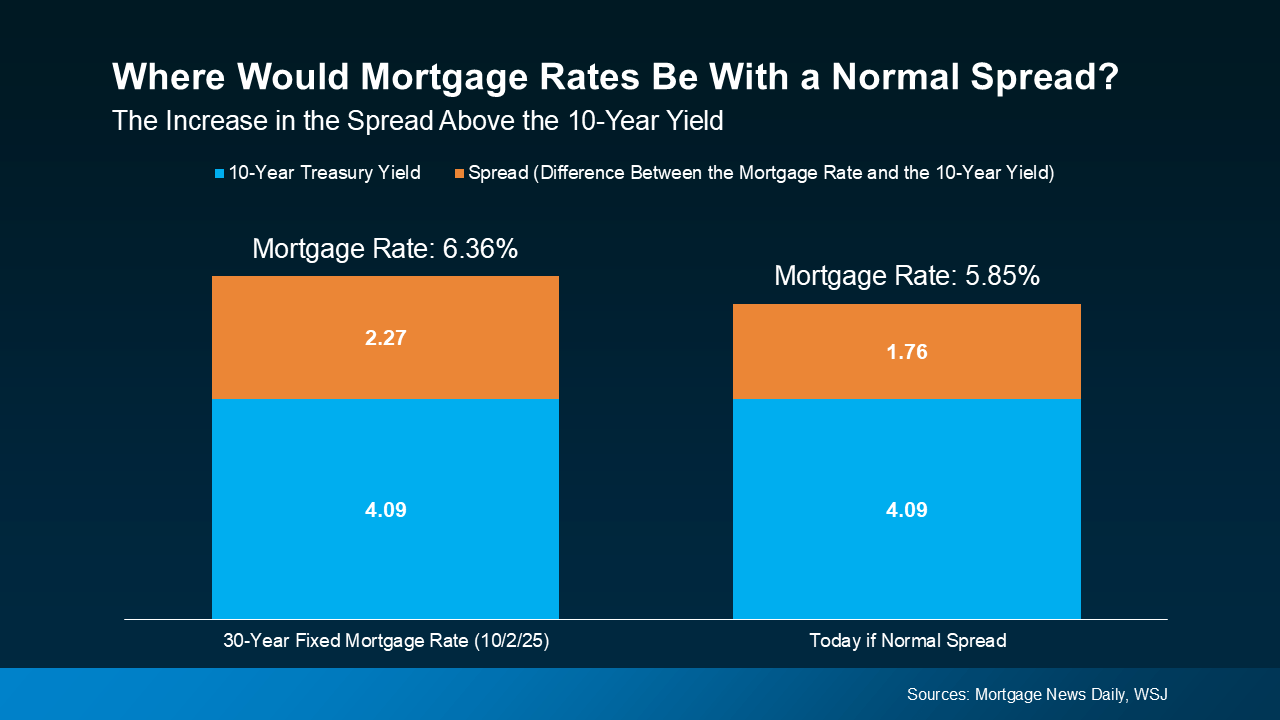

The 10-Year Treasury Yield Is Expected To Decline

It’s not just the spread, though. The 10-year treasury yield itself is also forecast to come down in the months ahead. So, when you combine a lower yield with a narrowing spread, you have two key forces potentially pushing mortgage rates down going into next year.

This long-term relationship is a big reason why you see experts currently projecting mortgage rates will ease, with a fringe possibility they’ll hit the upper 5s toward the end of next year.

Here’s how it works. Take the 10-year treasury yield, which is sitting at about 4.09% at the time this article is being written, and then add the average spread of 1.76%. From there, you’d expect mortgage rates to be around 5.85% (see graph below):

But remember, all of that can change as the economy shifts. And know for certain that there will be ups and downs along the way.

But remember, all of that can change as the economy shifts. And know for certain that there will be ups and downs along the way.

How these dynamics play out will depend on where the economy, the job market, inflation, and more go from here. But the 2026 outlook is currently expected to be a gradual mortgage rate decline. And as of now, things are starting to move in the right direction.

Bottom Line

Keeping up with all of these shifts can feel overwhelming. That’s why having an experienced agent or lender on your side matters. They’ll do the heavy lifting for you.

If you want real-time updates on mortgage rates, let’s connect so you have someone to keep you in the loop and help you plan your next move.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice