What a Fed Rate Cut Could Mean for Mortgage Rates in 2025 & Beyond

Meta Title: What a Fed Rate Cut Means for Mortgage Rates in 2025 & Beyond

Meta Description: A Fed cut doesn’t automatically mean mortgage rates fall. Discover how bond yields, spreads, inflation, and market sentiment truly drive rates — and when relief might arrive.

Introduction

When the Federal Reserve signals that it might cut the federal funds rate, many homeowners, prospective buyers, and refinancers hope mortgage rates will fall — sometimes sharply. But in practice, the path from a Fed rate cut to more affordable mortgage rates is anything but direct.

In 2025, the Fed has already moved, and markets are watching carefully for what comes next. Meanwhile, mortgage rates have resisted dramatic drops. Why? Because mortgage pricing is driven not just by Fed policy, but by bond markets, inflation expectations, spreads, and risk sentiment.

In this article, you’ll find:

-

An explanation of why mortgage rates don’t simply mirror Fed moves

-

How markets often “price in” Fed actions before they happen

-

The latest on Fed policy, mortgage rate data, and forecasts

-

Possible scenarios for mortgage rate trajectories through late 2025 and into 2026

-

What it all means for homebuyers, refinancers, and homeowners

-

A voice-search–friendly FAQ you can embed as schema

Let’s dig in.

1. The Fed vs. Mortgage Rates: Why They Don’t Always Move in Sync

1.1 The Fed’s Tool: The Federal Funds Rate

The Federal Reserve’s core lever is the federal funds rate — the rate at which banks lend to each other overnight. By adjusting this, the Fed influences short-term liquidity, monetary conditions, and the benchmark for many short-term interest rates.

However, the Fed does not directly set long-term mortgage interest rates. That’s a common misconception.

1.2 Mortgage Rates Track Longer-Term Yields

In practice, 30-year fixed mortgage rates more closely follow the 10-year U.S. Treasury yield and overall bond market conditions. Why?

-

Mortgage lenders and investors look at long-term yields as the basis for pricing loans, since mortgages are long-duration assets.

-

Mortgage-backed securities (MBS) compete with Treasuries for investor capital. To compete, yields on MBS must align (plus a margin) with Treasury yields.

-

The “spread” between mortgage rates and benchmark yields covers credit risk, operational costs, servicing, default risk, and liquidity premium.

So even if the Fed cuts its short-term rate, if Treasury yields remain elevated or even rise, mortgage rates may barely move — or could move in the opposite direction.

1.3 Other Key Forces Shaping Mortgage Rates

A Fed cut is only one piece of the puzzle. These forces often dominate:

| Factor | How It Affects Mortgage Rates |

|---|---|

| Inflation expectations | If inflation remains persistent, investors demand higher yields, pushing mortgage rates higher |

| Bond & MBS demand | If demand for mortgage-backed securities weakens, yields widen, increasing mortgage rates |

| Risk premiums & spreads | In uncertain markets, lenders widen spreads to protect against defaults or volatility |

| Economic data | Strong jobs or GDP growth can push yields upward |

| Fed balance sheet activity | If the Fed is shrinking its holdings of Treasuries/MBS, liquidity tightens and spreads widen |

| Global capital flows | Foreign demand for U.S. debt influences yields |

In short: mortgage rates are the result of many interacting forces — some connected to Fed action, many not.

2. Markets Price in Fed Cuts Ahead of Time

2.1 Anticipation vs. Action

Markets often anticipate central bank moves well before they happen. Traders, institutional investors, and bond markets adjust expectations of rate cuts or hikes, and those expectations show up in bond yields and mortgage pricing before official policy changes.

For instance, in 2025, mortgage rates have moved in response to expectations of a rate cut even before the Fed took action. CBS News+1

That means that by the time the Fed does cut, much of the anticipated effect may already be reflected in yields and mortgage rates — leaving less room for “surprise” movement.

2.2 Modest Cuts, Limited Surprise

When the Fed’s cut aligns with market consensus — e.g., a standard 25 basis point cut — much of the movement is already priced in. The actual announcement may produce only modest additional reaction. The bigger impact often comes from unexpectedly large cuts or strong dovish guidance for future cuts.

2.3 Data, Volatility & Rate Divergence

Unanticipated economic data — such as inflation surprises, labor market shifts, or geopolitical events — may shift bond yields sharply. This can cause mortgage rates to move in a direction contrary to the Fed’s action.

In volatile periods, yield curves can invert or steepen, spreads can widen, and investor sentiment can swing — complicating the transmission of Fed policy to mortgage rates.

3. Recent Context — Fed Action, Mortgage Data & Market Signals

3.1 The September 2025 Fed Cut

On September 17, 2025, the Federal Open Market Committee (FOMC) cut the target range for the federal funds rate by 25 basis points, bringing it to 4.00%–4.25%. Federal Reserve+2Trading Economics+2

The Fed also reaffirmed that it would continue reducing its holdings of Treasury securities and agency mortgage-backed securities (MBS). Federal Reserve

The statement emphasized that further rate decisions will depend on incoming data, particularly on employment and inflation. Federal Reserve

Although some policymakers had preferred a 50 bps cut, the final decision aligned with market expectations. Federal Reserve+1

3.2 Mortgage Rate Trends During & After the Cut

-

Freddie Mac reports that on October 2, 2025, the 30-year fixed mortgage rate ticked upward slightly. Freddie Mac

-

Over recent weeks, the 30-year fixed rate has hovered in the mid-6% range. CBS News+1

-

In some weeks post-cut, mortgage rates rose again — a reminder that a Fed cut does not guarantee sustained rate declines. CBS News+1

-

According to AP News, the average 30-year mortgage rate was 6.34% in early October — slightly up from recent lows. AP News

These patterns underscore how mortgage rates respond not just to policy but to market forces, investor sentiment, and yield movements.

3.3 Analyst & Forecast Views

-

Forbes Advisor notes that many institutions expect mortgage rates to remain in the mid-6% range in 2025, with possible declines in 2026. Forbes

-

NAR (National Association of Realtors) anticipates mortgage rates could edge toward 6% in 2026, but likely will stay higher in 2025. Forbes

-

Some economists and market commentators argue that the Fed’s continued reduction of MBS holdings is acting as a headwind for rate declines, keeping mortgage spreads wider. Federal Reserve+2Akron Legal News+2

Taken together, the consensus is cautious: rates may decline gradually, but steep drops are unlikely unless conditions shift significantly.

4. Scenarios for Mortgage Rates: What Could Happen Next

Given how many variables are in play, it’s helpful to think in terms of scenarios. Below are possible paths for mortgage rates through late 2025 and into 2026 — along with what would need to fall into place.

4.1 Base Case: Gradual Decline

Assumptions:

-

The Fed delivers one or two additional 25 bps cuts in late 2025 if inflation softens and growth slows.

-

Treasury yields gradually retreat as markets price in the easing cycle.

-

Spreads on mortgage-backed securities and mortgage risk margins tighten slightly.

Expectations:

-

Mortgage rates drift downward, perhaps toward ~6.0% to ~6.3% by late 2025.

-

Movement will be modest, not dramatic.

-

The primary gains come from gradual yield compression and long-term expectations.

-

Some borrowers will see enough movement to justify refinancing, especially those who locked very high rates earlier.

4.2 Optimistic Case: Faster Roll-Back

Assumptions:

-

The Fed surprises with larger cuts (e.g. 50 bps) or signals a more aggressive easing stance.

-

Treasury yields drop sharply in response.

-

Mortgage spreads narrow significantly due to heightened demand for bonds/MBS.

Expectations:

-

Mortgage rates could dip into the 5.5% to 6.0% range, especially late 2025 or early 2026.

-

Some mortgage lenders might offer promotional pricing or incentives to attract refinancing volume.

-

This scenario would require a relatively soft economic backdrop and alignment of multiple favorable factors.

4.3 Pessimistic Case: Inflation Resurgence or Policy Reversal

Assumptions:

-

Inflation unexpectedly rebounds (due to energy, supply shocks, tariffs).

-

Economic data surprises on the upside (strong jobs, consumer spending), limiting Fed’s freedom to ease further.

-

Treasury yields jump, spreads widen.

Expectations:

-

Mortgage rates stall or even climb, potentially approaching 6.5%+.

-

Any gains from prior cuts could be reversed.

-

Refinancing activity slows, and housing demand weakens under tighter conditions.

4.4 Wildcard Factors to Watch

-

Fed’s balance sheet policy: If the Fed continues to shrink its holdings of Treasury and MBS, it removes liquidity support for bond/MBS markets, pushing spreads wider.

-

Global rate dynamics & capital flows: Foreign central bank moves or global risk sentiment shifts can move U.S. Treasury yields.

-

Fiscal policy, deficits & government debt: Rising deficits or credit concerns can put upward pressure on interest rates.

-

Geopolitical risks or shocks: Sudden events — trade wars, wars, supply chain disruptions — can push yields and inflation expectations.

-

Sentiment & risk premia swings: In volatile times, lenders may demand greater compensation via spreads even if base yields drop.

5. Implications & Strategy: What You Should Do as a Buyer, Homeowner, or Refinancer

5.1 For Homebuyers: Act Wisely, Don’t Wait Blindly

-

Don’t over-time the market. Waiting for “the perfect rate” can backfire, especially if yields rise or home prices move upward.

-

Lock when comfortable. If you find a rate you can live with given your budget, locking in may reduce risk.

-

Understand affordability dynamics. Small rate changes matter, but so do down payment, loan term, and debt profile.

-

Expect more seller activity. If mortgage rates ease, more buyers may enter — competition could intensify.

5.2 For Refinancers: Crunch the Numbers

-

Look at your breakeven horizon. If your expected time in the home justifies paying refinancing costs, even moderate rate drops can make sense.

-

Target at least 0.75%–1.0% rate reduction (net of fees) when possible to generate meaningful savings over time.

-

Shop lenders. Different lenders offer different margins and closing costs — you may find better deals if you shop.

-

Track your credit profile. Improving credit, reducing debt, and lowering risk metrics can shrink your borrowing spread.

5.3 For Current Homeowners: Stay Alert, Strategize for the Long Term

-

If you have an adjustable-rate mortgage (ARM) coming up for reset, future rate cuts may reduce your payments.

-

More potential buyers returning due to lower rates may increase demand and raise home prices — boosting equity.

-

If you plan to stay long term, consider locking in a fixed rate now to protect against unexpected rate rises.

5.4 Smart Moves in a Shifting Rate Environment

-

Watch 10-year Treasury yields — they’re the bellwether for mortgage rate movement.

-

Stay updated on inflation data. CPI, PCE, and core inflation trends matter for forward expectations.

-

Monitor Fed commentary and speeches. Guidance around future rate paths often moves markets.

-

Be flexible. Be ready to lock, act, or pause depending on evolving dynamics.

-

Consult mortgage professionals or advisors who can provide projections tailored to your situation.

6. Voice-Search & FAQ Schema: Common Questions & Answers

Here’s a set of voice-friendly FAQs you can integrate into your page schema (FAQPage) to improve discoverability and voice search relevance.

Q1: Why don’t mortgage rates fall right after the Fed cuts rates?

A: Because mortgage rates follow long-term yields (like 10-year Treasury yields) and depend on spreads, risk premiums, and investor demand — not the short-term Fed rate alone.

Q2: How much could mortgage rates drop if the Fed cuts by 25 basis points?

A: If bond yields fall and spreads tighten, mortgage rates might decline 0.10% to 0.30% (10–30 basis points). But it depends heavily on market reaction.

Q3: Will mortgage rates go down significantly in 2025?

A: Most analysts expect a gradual decline in 2025, with more meaningful easing possible in 2026 if inflation and growth cooperate.

Q4: When should I lock a rate for a mortgage?

A: Lock when you see a rate and loan terms you can accept — don’t rely solely on future drops. Protect yourself against rising yields.

Q5: Is refinancing worth it right now?

A: Possibly, if you can reduce your rate by enough to overcome closing costs and your expected time in the home is long enough.

Q6: Will mortgage rates ever return to 4%?

A: It’s unlikely in the near to mid-term unless inflation collapses, yields fall dramatically, and central banks undertake aggressive easing globally.

Q7: Does the Fed buying or selling mortgage-backed securities (MBS) impact mortgage rates?

A: Yes — when the Fed holds or purchases MBS, it provides liquidity and supports narrower spreads. If the Fed reduces MBS holdings, that can widen spreads and keep mortgage rates higher.

Q8: What should I watch to anticipate mortgage rate changes?

A: Focus on 10-year Treasury yields, inflation data, Fed statements/guidance, and demand for MBS or bond flows.

7. Summary & Takeaway

A Fed rate cut is a meaningful tool in monetary policy — but it’s not a direct lever for mortgage rates. Mortgage rates respond to a broader set of forces: bond yields, inflation, investor demand, credit spreads, and risk sentiment.

While the September 2025 cut was expected, mortgage rates didn’t collapse afterward — much of the movement was already priced in. Going forward, a scenario of gradual declines in mortgage rates is most likely, unless conditions shift favorably in a dramatic way.

What should you do?

-

Stay informed and ready — watch key indicators like Treasury yields and inflation.

-

If you see a rate you’re comfortable with, lock it rather than trying to time the bottom.

-

Refinancers should model their breakeven periods and compare total costs vs. savings.

-

Don’t ignore credit, debt ratios, and lender offers — getting the best margin matters.

-

Expect modest movement, not miracles — and plan decisions accordingly.

![]()

What a Fed Rate Cut Could Mean for Mortgage Rates

The Federal Reserve (the Fed) meets this week, and expectations are high that they’ll cut the Federal Funds Rate. But does that mean mortgage rates will drop? Let’s clear up the confusion.

The Fed Doesn’t Directly Set Mortgage Rates

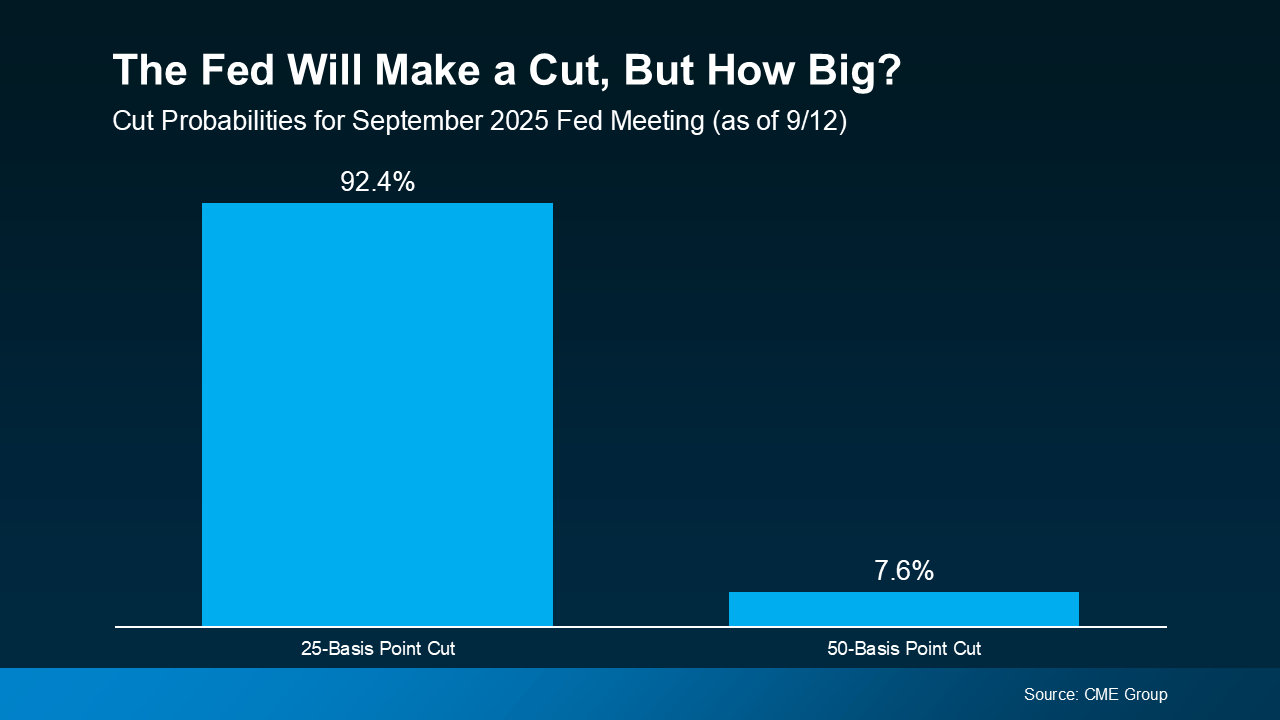

Right now, all eyes are on the Fed. Most economists expect they’ll cut the Federal Funds Rate at their mid-September meeting to try to head off a potential recession.

According to the CME FedWatch Tool, markets are already betting on it. There’s virtually a 100% chance of a September cut. And based on what we know now, there’s about a 92% chance it’ll be a small cut (25 basis points) and an 8% chance it will be a bigger cut (50 basis points):

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

Why Markets Already Saw This Cut Coming

Here’s the part that may surprise you. Mortgage rates tend to respond to what the financial markets think the Fed will do, before the Fed officially acts. Basically, when markets anticipate a Fed cut, that outlook gets priced into mortgage rates ahead of time.

That’s exactly what happened after weaker-than-expected jobs reports on August 1 and September 5. Each time, mortgage rates ticked down as financial markets grew more confident a cut was coming soon. And even though inflation rose slightly in the latest CPI report, the Fed is still expected to make a cut.

So, if the Fed goes with a 25-basis point cut, as expected, that’s likely already baked in to current mortgage rates, and we may not see a dramatic drop.

But if they go bigger and drop their Federal Funds Rate by 50 basis points instead, mortgage rates could come down more than they already have.

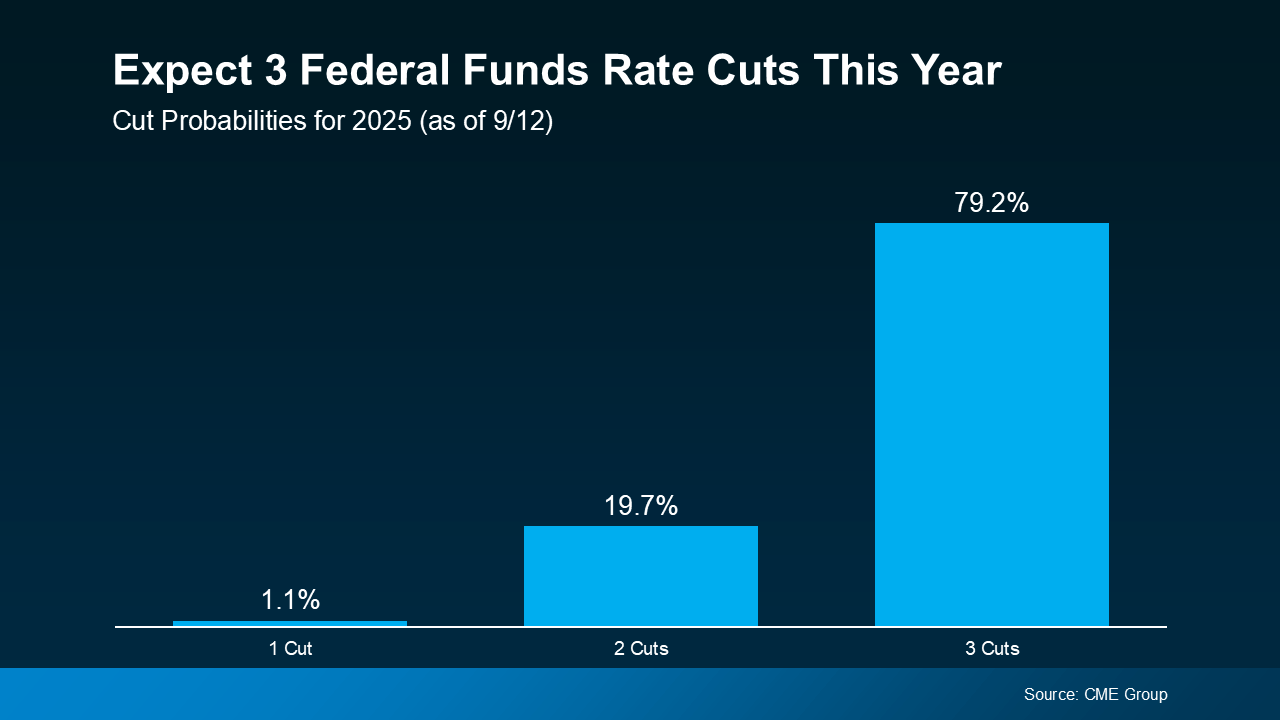

So, Where Do Mortgage Rates Go from Here?

While the upcoming cut may not move the needle much, many experts expect the Fed could cut the Federal Funds Rate more than once before the end of the year. Of course, that’s if the economy continues to cool (see graph below):

As Sam Williamson, Senior Economist at First American, explains:

As Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If multiple rate cuts happen, or even if markets just believe they will, mortgage rates could ease further in the months ahead. But here’s the catch – all of this depends on how the economy evolves. Surprise inflation data or unexpected shifts could quickly change the outlook.

Bottom Line

Mortgage rates likely won’t drop sharply overnight, and they won’t mirror the Fed’s moves one-for-one. But if the Fed begins a rate-cutting cycle, and markets continue to expect it, mortgage rates could trend lower later this year and into 2026.

If you’ve been waiting and watching the housing market, now’s the time to talk strategy. Even small changes in rates can make a meaningful difference in affordability, and understanding what’s ahead helps you make the best decision for your situation.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice