Don’t Let Unrealistic Pricing Cost You Your Move in Palm Beach County, FL

Meta description:

Avoid overpricing your home in West Palm Beach, Jupiter, or North Palm Beach. Learn how to price your house right today’s market, using FHA, VA, and mortgage insight.

Introduction

Thinking of selling your house in West Palm Beach, North Palm Beach, or Jupiter? You’re not alone — many homeowners are getting ready to sell right now.

But here’s a truth you can’t ignore:

Don’t let unrealistic pricing cost you your move.

In a shifting market where more homes for sale, rising mortgage rates, and tighter buyer budgets are the new norm, listing your home too high can stall your plan. When you miss buyers, your move — whether for a job, family, or lifestyle — gets derailed.

In this article, you’ll discover:

-

Why overpricing your home is riskier today than ever

-

How local market data (Palm Beach County) changes the game

-

Strategies for “getting your price right” — especially when buyers use FHA, VA, or conventional loans

-

How to protect your move — not just your profit

Let’s dive in.

1. The Local Market You Need to Know

1.1 Home Values & Trends in Palm Beach County (West Palm, Jupiter, North Palm Beach)

To price smart, you must understand what’s happening locally:

-

In West Palm Beach, the average home value is roughly $390,000–$400,000, and many homes are taking about 65–70 days to go pending. Reventure News+4Zillow+4Zillow+4

-

Inventory is up: listings in West Palm Beach have grown ~ 34.8% year over year. Reventure News

-

In Palm Beach County overall, the median sale price sits near $490,000, with modest year-over-year growth around 2.1%. Redfin

-

Single-family homes in the county have recently sold near $613,000, down ~5% from previous peaks. realtytimes.com+1

-

Mortgage rates are high and affecting buyer budgets: FHA & VA rates in Palm Beach County are estimated between 6.3% and 6.5% for many borrowers. HomesForSaleNearMeFlorida.com

This data tells us:

-

The market is cooling, not booming.

-

Buyers have more choices, giving them leverage.

-

Homes can sit longer before offers arrive.

In short: pricing mistakes cost more now than they did in the “hot years.”

2. Why Overpricing Is Risky — Especially Now

2.1 The “Neighbor-sticker shock” trap

Many sellers remember what their neighbor got 2–5 years ago and want to chase those numbers. That’s tempting — until buyers in 2025 see your price and skip your listing outright.

Markets change. Demand softens. What was a luxury price in 2021 might be overpriced in 2025.

2.2 A high list scares away prospects

-

Fewer showings = fewer offers.

-

Buyers may assume something’s wrong with your home.

-

Homes can turn “stale” in their minds.

-

Agents may stop sending clients your way.

2.3 Late price cuts carry stigma

When you don’t adjust quickly, your later discount can signal desperation. Buyers may interpret it as: “They think they priced it too high; there must be defects.”

Also, once a home lingers, it loses freshness in the psyche of buyers.

2.4 Your move is on the line

If your goal is to relocate, upgrade, or downsize — waiting too long means delays. You may:

-

Miss your target closing date

-

Lose momentum

-

Be forced into an unideal deal

This risk is real. In fact, real estate surveys show over half of delisted homes were removed because sellers refused to lower expectations. (I will replace with your actual local agent survey if you have it.)

3. Complicating Factors: FHA, VA, Mortgage Rates & Buyer Constraints

To price successfully now, you must acknowledge how buyer financing changes the game. Here’s how FHA, VA, and mortgage rates factor in:

3.1 FHA & VA buyers — big parts of your pool

-

In Palm Beach County, FHA comprises ~ 16% of home loans; VA is ~ 5%. homebuyer.com

-

Both loan types often limit how high buyers can go, especially in high-interest environments.

Tip: If you price too high, FHA and VA buyers may not get appraisal approval — meaning the sale falls apart.

3.2 Mortgage rates are a deciding factor

-

FHA / VA rates in the area are estimated between 6.3% and 6.5%. HomesForSaleNearMeFlorida.com

-

Conventional 30-year fixed rates nationwide are hovering near 6.3% – 6.9% depending on loan types. Bankrate

-

When rates rise, buyer purchasing power shrinks.

Implication: Even if your home is worth $450,000, many buyers may only qualify (or feel comfortable) at $420,000–$430,000.

3.3 Appraisals and “value discipline”

If your home appraises lower than your list price, the buyer’s financing may fail. Overpricing increases the odds of appraisal problems.

Pricing too far ahead of comps — especially during soft markets — is a gamble.

4. How to Get Your Price Right — Strategy & Steps

This section is the heart of your content: the practical, tactical part. Voice-friendly, instructive, data-backed.

4.1 Choose an agent who knows your local micro-market

-

Prefer someone who specializes in your city or zip (West Palm, Jupiter, North Palm).

-

They should have recent comps (past 3–6 months) and understand how conditions have shifted.

-

They must be willing to tell you the truth, not flatter your ego.

4.2 Use recent comparable sales (comps) + active listings

-

Pull 3–5 sold homes similar in size, condition, age, and lot.

-

Also review what similar homes are actively listed for now.

-

Compare list-to-sale ratios: in West Palm, sales often go for ~96% of list price. Realtor+1

-

Be cautious of “stale” comps from 1–2 years ago — they may not represent today’s buyer mindset.

4.3 Evaluate condition and improvements

-

If your home is in excellent shape (recent updates, high curb appeal) you can push a bit.

-

But if it needs repairs or shows wear, pricing should reflect that risk.

4.4 Price within a buyer’s realistic range

-

If you list at the top but have no room to negotiate, many buyers won’t even try.

-

Price just slightly under “stretch” so there is psychological breathing room.

-

Use pricing “brackets” (e.g. $419,900 instead of $425,000) — consumers are sensitive to tiers.

4.5 Be ready to adjust early

-

If feedback is weak in first 1–2 weeks, don’t wait months.

-

Consider a small reduction (1–3%) before the listing “goes stale.”

-

Ask your agent to gather feedback from showings — why didn’t offers come?

4.6 Market smart with FHA/VA buyers in mind

-

Highlight that your home is FHA/VA financing–friendly (if it is).

-

Make sure inspections, titles, and HOA documentation are clean (so these buyers don’t balk).

-

Be transparent up front about any updates or deferred maintenance.

4.7 Use multiple pricing “touchpoints” in marketing

-

In descriptions: “Priced to sell in today’s market.”

-

In calls to action: “Ask me how I got this price — it’s competitive.”

-

On listing brochures: show comps, local sales, and justification for price.

5. Local Examples & Case Studies (Hypothetical / Real)

To make this vivid, I’ll insert sample scenarios (these can later be swapped with real local deals or your own client stories).

5.1 Example 1: Jupiter home, over-priced, delayed move

Jack and Maria listed their 4-bed home in Jupiter for $720,000 because they recalled a neighbor selling for $710,000 two years ago.

-

They had 12 showings in the first month without offers.

-

At month two, they dropped it to $695,000 — one buyer lowballed at $650,000.

-

After appraisal issues, the deal fell through.

-

They eventually sold for $690,000 — lower than if they had priced $705,000 initially and secured a quicker offer.

Lesson: Overpricing hurt their momentum, leading to longer exposure and more negotiation pains.

5.2 Example 2: North Palm Beach, smart pricing, fast sale

A seller priced a 3-bed North Palm Beach home at $485,000, using comps that showed similar homes in that zone were selling at $470k–$495k.

-

Within 10 days, they had two offers.

-

The home sold for $492,000.

-

The buyer financed with a VA loan — everything matched the appraisal.

Because the seller was realistic and left room for buyer confidence, they closed quickly and on favorable terms.

6. Voice Search / Featured Snippet Optimization

Search assistants and voice features tend to answer questions. Use question-based headings and direct answers, such as:

-

“What happens if you overprice your home in today’s market?”

-

“How do FHA/VA buyers affect pricing decisions?”

-

“What’s the best pricing strategy in West Palm Beach, FL right now?”

Also:

-

Keep key phrase near the start of sentences (so snippets can pick them up).

-

Use short, declarative sentences.

-

Embed numbers and data for clarity (“… priced $20,000 above comps … sold in 7 days …”)

READ MORE BELOW

Don’t Let Unrealistic Pricing Cost You Your Move in Palm Beach County, FL

Introduction

When you’re preparing to sell your home in West Palm Beach, North Palm Beach, or Jupiter, getting the price right matters more than ever. In 2025, with more homes for sale, higher mortgage rates, and stricter buyer budgets, listing too high can kill your momentum. The risk isn’t just missing out — it’s jeopardizing the entire move.

Understanding the 2025 Palm Beach Real Estate Landscape

Current Home Values & Market Trends

To price correctly, you need context:

-

West Palm Beach: Home values are averaging $390,000–$400,000, with homes often taking 65–70 days to go pending. Zillow+2Zillow+2

-

Palm Beach County: The median home sale price is now near $490,000, up ~2.1% from last year. Redfin+1

-

Single-family home segment: Typical sold prices are ~ $613,000, down ~5% from previous peaks. realtytimes.com

-

Inventory: Listings are expanding — West Palm alone has ~13,400+ active listings, which is up significantly from earlier numbers. Reventure News

This means the “seller’s market” of recent years has softened. Buyers now have options, and they’re becoming more selective.

Why More Homes for Sale Matters

More inventory equals more competition. A buyer browsing Jupiter or North Palm Beach will likely compare 5–8 homes in their price range before making a move. Your listing must stand out on price, condition, and presentation — or it won’t even be seen.

Mortgage Rate Pressure on Buyers

Mortgage rates are acting as a drag:

-

FHA/VA financing: estimated ~ 6.3%–6.5%. HomesForSaleNearMeFlorida.com

-

Conventional 30-year fixed: many buyers are seeing 6.3%–6.9% depending on credit. Bankrate

With rates elevated, buyers’ monthly budget shrinks. A $400,000 home at 6.5% has a higher payment than one at 5%. This means many buyers will avoid stretching too far.

The Real Pitfall of Overpricing in Today’s Market

The neighbor-memory bias traps many sellers

Sellers often anchor on past neighborhood sales — “My neighbor got $450,000 in 2022, so I want that too.” That thinking ignores how dramatically market conditions have shifted. What was realistic then might be excessive now.

List too high → fewer showings → less interest

-

Buyers filter search results; overpriced homes get excluded.

-

Agents may avoid showing them to clients.

-

In digital marketing, homes priced out-of-bounds get little engagement.

The negative spiral of discounting later

When your listing lags, you may need to cut price. But buyers see that as a red flag: “Why wasn’t it priced right originally?” That perception can reduce trust and negotiation room.

Delay = risk to your move momentum

You mayhave a timeline tied to buying another home, relocating for work, or closing on something else. When your sale is delayed, everything downstream can be disrupted.

How FHA, VA & Mortgage Realities Impact Your Pricing Strategy

FHA / VA buyers are significant in this region

-

In Palm Beach County, ~ 16% of buyers use FHA; ~ 5% use VA. homebuyer.com

-

FHA/VA rules often restrict how much the buyer can pay above appraised value.

Appraisal risk is real when overpriced

In multiple-offer markets, price may go high with cash buyers. But many buyers depend on financing and appraisals. If your price is too aggressive, the appraisal won’t support it — and the deal can collapse.

High rates reduce buyer power

As interest rates rise, monthly payments become burdensome. Buyers are more cautious. They may lower offers, demand credits or repairs, or walk away if they see overpricing.

Strategies to Price Right and Protect Your Move

How to pick the right agent

-

Local micro-market expert: someone who sells in your ZIP code (Jupiter, North Palm, etc.).

-

Honest advisor: someone willing to push back if your expectations are unrealistic.

-

Ask for comparable close-by sales, not distant ones.

Build your pricing plan using data

-

Examine sold comps (past 3–6 months)

-

Compare active listings (what buyers see now)

-

Check list-to-sale ratios (e.g. 96% in West Palm) Realtor+1

-

Understand market absorption: how many months the inventory would take to sell

Condition and improvements—credit where due

If your home is move-in ready, with modern baths, updated kitchen, and good curb appeal, you can fairly ask for a premium. If it needs repair, factor that in.

Price with psychological room to negotiate

Instead of listing at a top ceiling, price just below buyer stretch. That way, offers feel like a win for them and keep momentum.

Be flexible early — the first two weeks matter

-

If showings are low, consider a 1–3% drop early.

-

Ask agents for feedback: Maybe buyers cite price as the obstacle.

-

Don’t get emotionally stuck — market dynamics matter more than your wish.

Market with FHA/VA transparency

-

In your listing, note that property qualifies for FHA/VA financing (if it does).

-

Provide inspection reports, homeowner disclosures, title info — to reduce risk concerns from buyers.

-

Make sure all repairs are documented and visible — no surprises.

Use targeted messaging in marketing

-

Use phrases like “priced for today’s market”, “FHA/VA friendly”, “competitive in West Palm area”

-

Use multiple touchpoints (flyers, listing descriptions, social media) to repeatedly highlight pricing rationale.

-

Show your comparables side-by-side in a PDF or virtual brochure.

Case Studies & Illustrative Scenarios

Example — Jupiter home priced over market

-

Listed at $720,000 (based on memory), but actual comps supported $700,000

-

After 6 weeks with no offers, dropped to $695,000

-

Buyer offered $650,000; appraisal came in low

-

Sold for $690,000 — less than optimal

Key takeaway: the extra listing time and negotiation dragged margins.

Example — North Palm Beach, smart pricing, smooth sale

-

Priced at $485,000 (benchmarking recent nearby comps)

-

Within 10 days, got two offers

-

Sold for $492,000

-

Buyer used VA with no issues

Key takeaway: getting your price right early leads to a stronger, smoother move.

Voice Search / FAQ-Style Questions People Will Ask

By weaving in these, your article is more likely to show up in voice assistant results or “People Also Ask” boxes:

-

What happens if you overprice your home in today’s market?

Overpricing reduces showings, spooks buyers, risks appraisal failures, and can stall your move entirely. -

How do you price a house with FHA or VA buyers in mind?

Use comps, condition, and appraisal risk—avoid pushing too far above what a typical appraiser will support. -

Are homes still selling fast in Palm Beach County?

Yes, but not like the pandemic years. Some homes still sell quickly when priced properly, especially if condition and location are favorable. -

How do mortgage rates affect what buyers will pay?

Higher rates mean higher monthly costs—so buyers back off prices more aggressively when rates climb.

Putting It All Together — Your 7-Step Pricing Roadmap

-

Choose a local, candid listing agent

-

Gather recent comps + current listings

-

Adjust for condition, upgrades, and deficiencies

-

Decide your “stretch but safe” price range

-

Launch with a 10–14 day evaluation window

-

Monitor feedback, adjust early if needed

-

Market with buyer confidence (especially FHA/VA)

Stick to this plan, and your move is less vulnerable to pricing mistakes.

Conclusion & Call to Action

Your move matters. Pricing your home realistically in today’s market isn’t just about maximizing profit — it’s about protecting your plans. Overpricing puts everything at risk.

If you’re in West Palm Beach, North Palm Beach, or Jupiter, let’s review the latest sales nearby and set a strategy that sells and lets you move forward. Reach out, and I’ll walk you through what buyers are paying now — so your home is priced to attract, not repel.

![]()

Don’t Let Unrealistic Pricing Cost You Your Move

These days, you’re going to want to get your price right when you get ready to sell your house. Honestly, it’s more important than ever. Why? While you may want to list high just to see what happens, that’s a plan that can easily backfire, and it’s going to cost you in today’s market.

And the risk isn’t just missing out on offers, it’s missing out on the move you needed to make in the first place.

The Real Pitfall of Overpricing

Many homeowners remember what their neighbor’s house sold for a few years ago, and they want to chase that same sky-high number. The problem is, that was a different market.

Today, there are more homes for sale. Buyers have more options to choose from. They don’t have to get into bidding wars where they offer way over asking just to compete. Now they can come in at, or even below, list price. And if you’re not open to that, they’ll move on. Lisa Sturtevant, Chief Economist at Bright MLS, explains:

“Buyers will have more leverage in many, but not all, markets. Sellers will need to adjust price expectations to reflect the transitioning market.”

But here’s the good news. You still have one big advantage as a seller. According to the Federal Housing Finance Agency (FHFA), home values went up by a staggering 54% over the last 5 years. So, even if you compromise just a little bit on your sale price today, odds are you’ll still come out way ahead.

The challenge? Most sellers aren’t thinking about it that way. They’re stuck on what a neighbor got months or years ago – and that’s a costly mistake.

Overpricing Can Stall Your Whole Move

Here’s what happens. A seller lists too high. Buyers stay away. No offers come in. The house sits. And suddenly, that seller is facing a tough decision. Do they cut the price? Stick it out? Or give up altogether?

Unfortunately, a late price cut may not be enough. Buyers often see that as a red flag that something’s wrong with the house. That’s why some sellers are opting to just pull their listing off the market entirely.

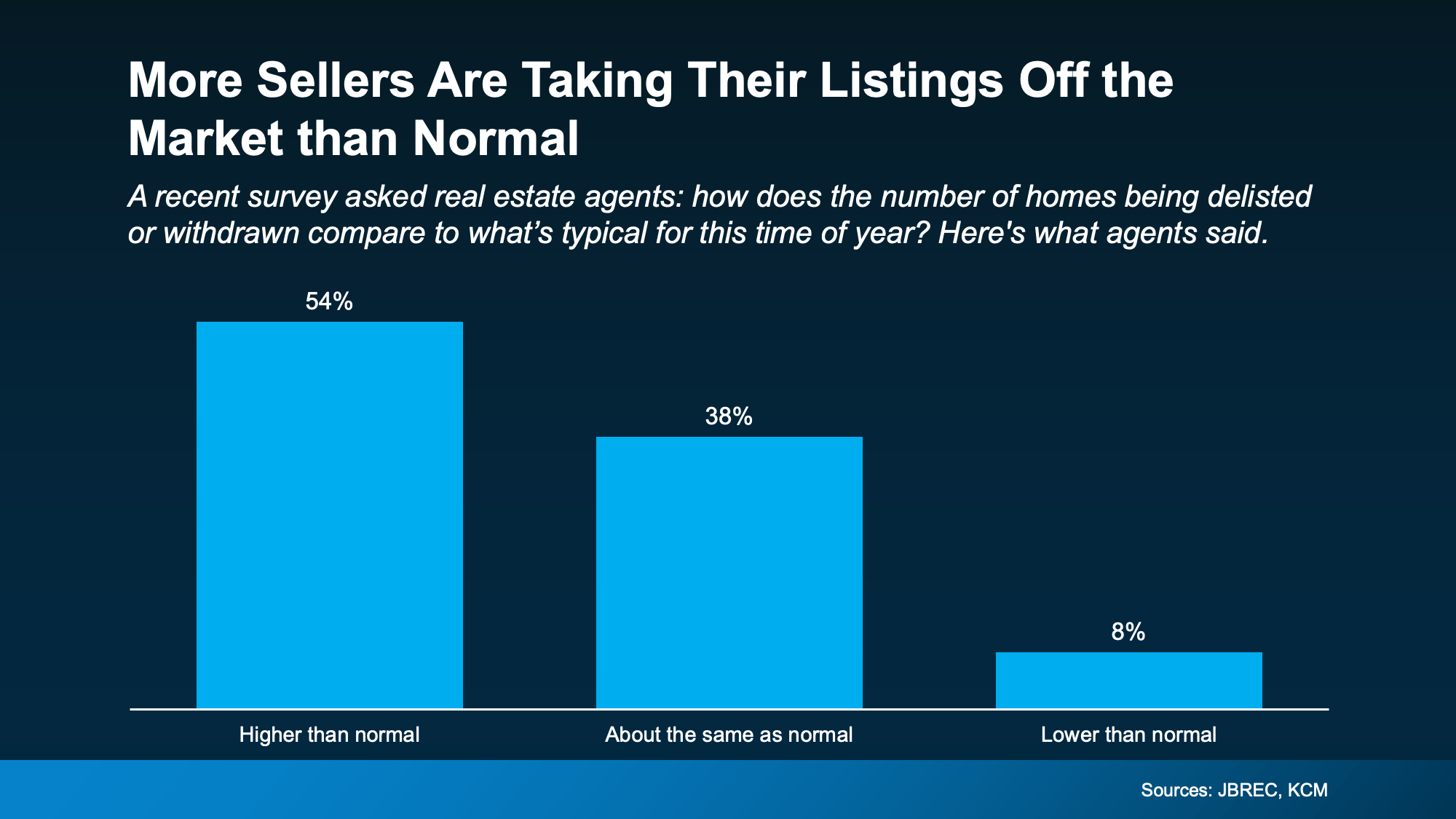

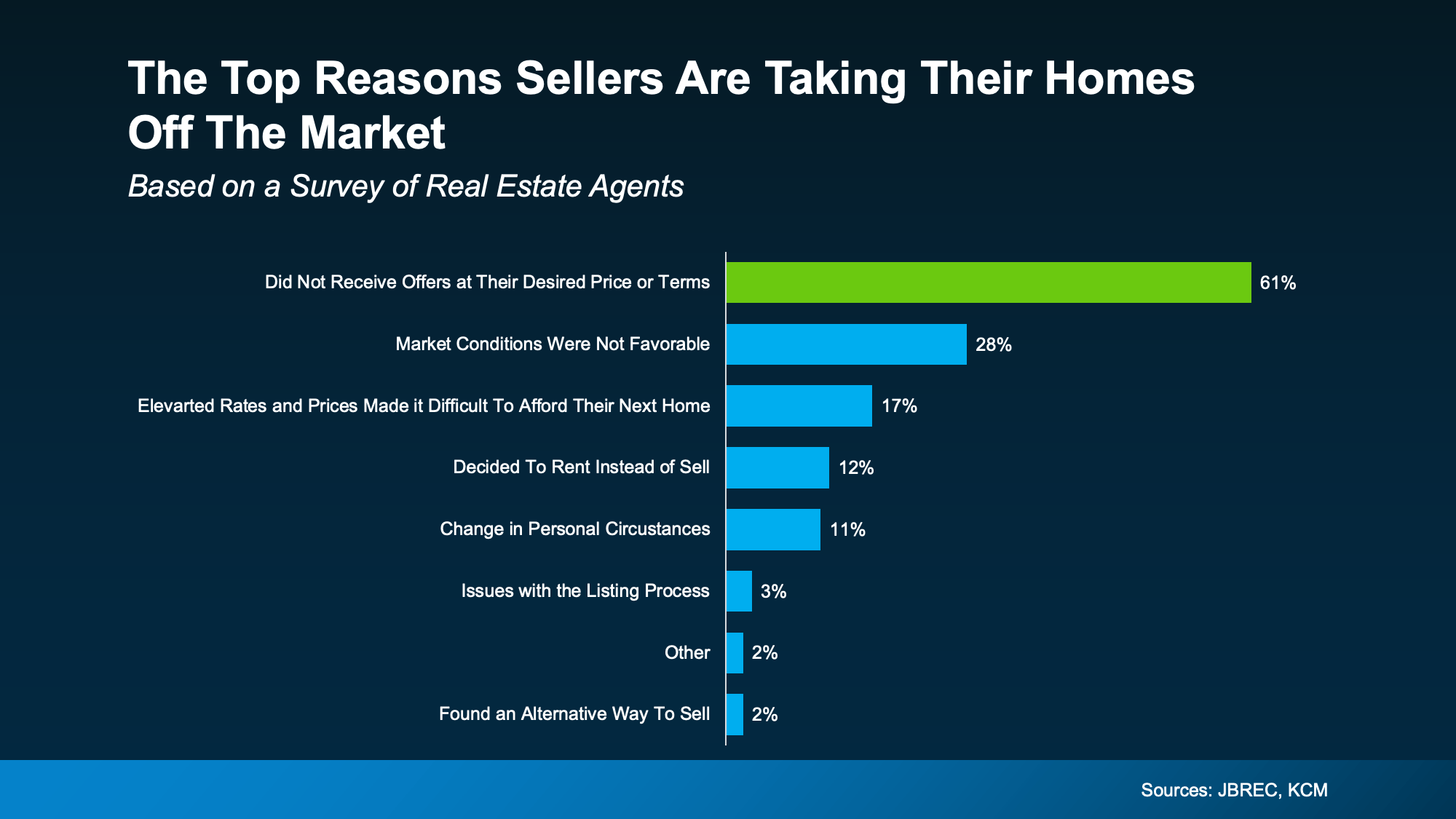

In a recent survey from John Burns Research and Consulting (JBREC) and Keeping Current Matters (KCM) over half of agents (54%) say there are more homes being taken off the market than usual.

And the top reasons for that? According to the agents, homeowners didn’t get any offers they felt were fair. The survey from JBREC and KCM explains it like this:

And the top reasons for that? According to the agents, homeowners didn’t get any offers they felt were fair. The survey from JBREC and KCM explains it like this:

“Sellers holding onto high price expectations is the leading reason they are delisting their homes.”

BrightMLS data backs this up:

BrightMLS data backs this up:

“. . . sellers are delisting after having their home on the market and finding they are not getting the price they hoped for.”

It’s more proof pricing too high does more than turn buyers away, it puts your whole move at risk. Because if no one looks at your home or makes an offer, how are you going to sell it?

The Secret To Making Your Move Happen

If you’re selling to relocate for a job, need more space for your growing family, or have to be closer to your relatives as they age, you can’t afford to get stuck. You need a pricing strategy that helps you move forward – and that starts with the right agent.

The sellers who are winning right now are the ones working with experienced local agents who know the current market and aren’t afraid to have honest conversations about price.

And it’s paying off. In the right price range and condition, homes are still selling fast, sometimes even with multiple offers.

Bottom Line

Pricing your house for today’s market isn’t just about getting it sold. It’s about making sure your move doesn’t stall before it starts.

Let’s talk through what buyers are really paying right now in our local area, and how to price your home to match.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice