BREAKING News: Mortgage Rates Just Dropped

The housing market just got some welcome news!

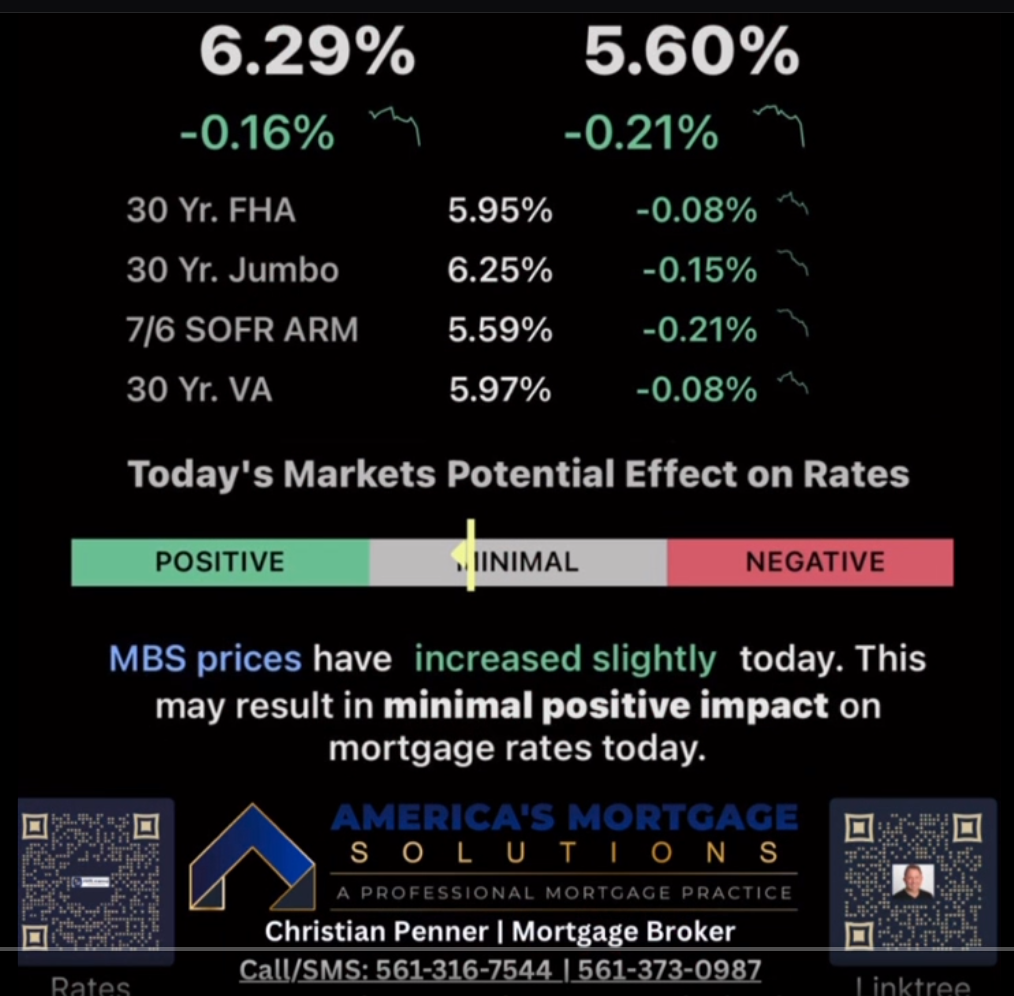

Mortgage rates plummeted after a surprisingly weak jobs report, with the 30-year fixed rate dropping from 6.45% to 6.29%

What This Means for YOU:

Lower monthly payments – A rate drop from 6.45% to 6.29% on a $400k home saves you about $40/month

More buying power – You can now afford roughly $5,000-7,000 more house for the same payment

Refinance opportunities – If you’ve been waiting to refi, this could be your moment

The Numbers That Matter:

- 30-Year Fixed: 6.29%

- 15-Year Fixed: 5.60%

- FHA Loans: 5.95%

- VA Loans: 5.97%

Why Did This Happen?

The August jobs report came in WAY below expectations (22K jobs vs. 75K expected), which sent investors rushing to buy bonds. When bond prices go up, mortgage rates go down – and boy did they go down today!

The bottom line: We’re back to fall 2024 rate levels, giving buyers and homeowners a breather in this challenging market.

When the job market shows weakness, investors flee to the safety of bonds. Bond prices rise, and mortgage rates fall. It’s Economics 101.

For perspective, this brings us back to the same rate levels we saw in fall 2024. If you’ve been sitting on the sidelines waiting for rates to improve, today might be the day you’ve been waiting for.

What This Actually Means

Let’s talk real numbers. On a $400,000 home purchase, this rate drop saves you about $40 per month. Over the life of the loan, that’s nearly $15,000 in interest savings.

But here’s what’s more important: you now have roughly $5,000 to $7,000 more buying power for the same monthly payment you were planning yesterday.

The Reality Check

This rate drop could reverse just as quickly with the next economic report.

The homebuyers who win in this market aren’t the ones who wait for the perfect rate. They’re the ones who recognize opportunity when it presents itself and act decisively.

Your Next Move

Whether you’re buying or selling any type of real estate – primary residence, second home, investment property, or commercial property – we’re here to help navigate these market shifts.

If you want to build something new or need professional mortgage advice, contact us at 561-316-6800. You can also find my calendar link in the comments to easily schedule a time for us to chat about your unique situation. (AMS.Money/Calendar)

Our Mission:

Tailored Solutions for Your Financial Success

We aim to customize a Real Estate and Financing Package that aligns with your short-term and long-term financial goals, while also considering your payment and equity objectives.

We aim to minimize your tax liabilities and maximize your cash flow, helping you achieve financial freedom.

In today’s market, securing real estate with a strategic financing package is a vital step toward building a stable and profitable financial future. Whether you’re looking to buy, sell, invest, or refinance, we help you make confident decisions that reduce your market risks and tax obligations.

Strategic Planning for Generational Wealth

Our approach goes beyond traditional services – we focus on equity-building strategies and debt management plans designed to secure long-term wealth for you and your family. By partnering with us, you’ll be taking crucial steps toward financial security and a brighter future.

Let’s work together to achieve your real estate goals and secure your financial future.

Comprehensive Services for All Your Real Estate and Financing Needs

Remember: Rates change daily, sometimes hourly. Don’t wait – let’s lock in these improved rates together.

If you are planning to take advantage of these lower rates?

Call me at 561-316-6800 or send me a message and let’s have a conversation.

What’s your next move in this shifting market?

![]()

Mortgage Rates Drop to 6.29%—What It Means for Buyers, Homeowners, and Investors

Meta Description: Mortgage rates dropped to 6.29% after a weak jobs report, marking the lowest levels since fall 2024. Learn how this impacts buyers, refinancing, and wealth-building strategies—and what steps you should take now.

Mortgage rate chart showing decline to 6.29% in September 2025.

Breaking News: Mortgage Rates Just Fell to 6.29%

The housing market just received some welcome relief.

As of September 9, 2025, the average 30-year fixed mortgage rate dropped to 6.29%, down from 6.45%. That may sound like a small change, but in the world of home loans, even fractions of a percentage can mean thousands of dollars saved over time.

For context, this is the lowest level since fall 2024, and it comes at a critical moment when affordability has been a major challenge for buyers.

Current Mortgage Rates: Snapshot for September 2025

-

30-Year Fixed Mortgage: 6.29%

-

15-Year Fixed Mortgage: 5.60%

-

FHA Loans: 5.95%

-

VA Loans: 5.97%

-

Jumbo Loans (Estimates): 6.45%–6.60%

These rates vary by lender, credit score, down payment size, and overall financial profile. But the trend is clear: borrowing just got cheaper.

Why Mortgage Rates Dropped: The Jobs Report Effect

So, what caused this sudden dip? The August jobs report came in shockingly weak:

-

Expected: 75,000 jobs

-

Actual: 22,000 jobs

That shortfall spooked investors. When the labor market cools, fears of economic slowdown rise. In response, investors move their money into U.S. Treasury bonds, considered safe assets.

Here’s the chain reaction in simple terms:

-

Investors buy more bonds →

-

Bond prices go up →

-

Bond yields go down →

-

Mortgage rates follow yields lower

It’s a classic case of “bad news for the economy is good news for borrowers.”

What Lower Rates Mean for Buyers

1. More Affordable Monthly Payments

If you’re buying a $400,000 home, the drop from 6.45% to 6.29% saves you about $40 per month. That’s $480 per year, or nearly $15,000 over 30 years.

2. More Buying Power

The lower rate means you qualify for a bigger loan at the same monthly payment. In fact, this shift gives you about $5,000–$7,000 more purchasing power.

That could be the difference between settling for a smaller house and landing your dream home.

3. Easier Entry for First-Time Buyers

High mortgage rates have kept many renters on the sidelines. This dip could be the opening they’ve been waiting for.

Why This Drop Matters for Refinancing

For homeowners who bought or refinanced when rates were higher, today’s drop may offer an opportunity to refinance and reduce monthly costs.

Example: Refinancing a $350,000 Loan

-

At 6.60%: Monthly principal & interest ≈ $2,235

-

At 6.29%: Monthly principal & interest ≈ $2,160

-

Savings: ≈ $75 per month, or $900 per year

While not massive, this can add up quickly, especially for households with tight budgets.

Tip: If your current rate is 7% or higher, refinancing today could deliver meaningful savings.

Loan Comparisons: Who Benefits the Most?

Conventional Loans

Best suited for buyers with strong credit and larger down payments. They benefit most from even small rate drops.

FHA Loans

Popular with first-time buyers. A drop like this can open the door for those who previously didn’t qualify.

VA Loans

For veterans and active-duty military, this drop makes already favorable loan terms even better.

Jumbo Loans

For luxury properties above conforming loan limits, a dip reduces payments significantly due to higher balances.

The Risk: Rates Could Bounce Back

While today’s drop is positive, it could be temporary. Rates are influenced by:

-

Federal Reserve policy

-

Inflation data

-

Future jobs reports

-

Global economic conditions

If inflation picks up again or the next jobs report is stronger, this relief could vanish quickly.

Spotlight: Common Questions Answered

Q: Are mortgage rates expected to keep falling in 2025?

A: Experts predict some volatility. If the economy slows further, rates may ease. If inflation ticks up, rates could climb again.

Q: Should I buy now or wait for lower rates?

A: It depends on your financial readiness. Rates are unpredictable. If you find a home that fits your needs and budget, today’s lower rate may be worth locking in.

Q: What’s the lowest mortgage rate ever recorded?

A: During the pandemic (2020–2021), 30-year fixed rates briefly fell below 3%, but those conditions were unique and unlikely to return soon.

Long-Term Perspective: Building Wealth with Real Estate

Lower rates don’t just save money—they help build equity and long-term wealth. Here’s how:

-

Equity Growth – Every payment increases your ownership stake.

-

Appreciation Potential – Homes historically rise in value over time.

-

Tax Benefits – Mortgage interest deductions can lower taxable income.

-

Rental Income – Investment properties can generate passive cash flow.

Case Study: How a Family Benefited from a Rate Drop

Consider a family in Florida who purchased a $450,000 home last year at 6.75%. By refinancing today at 6.29%, they save $125 per month. That’s:

-

$1,500 per year

-

$45,000 over 30 years

Those savings could fund a child’s college tuition, invest in retirement, or pay down debt faster.

Strategic Advice for Buyers & Sellers

-

Buyers: Get pre-approved quickly—lower rates increase competition.

-

Sellers: More buyers qualify at these levels, improving chances for strong offers.

-

Investors: Lower borrowing costs = higher ROI potential on rentals.

Our Mission: Tailored Financial Solutions

At AMS, we design financing packages that align with:

-

Your short-term affordability goals

-

Your long-term equity-building strategy

-

Your tax planning and cash flow needs

We believe in strategic planning for generational wealth, helping families secure not just homes—but financial futures.

Don’t Wait Too Long

Mortgage rates shift daily—and sometimes hourly.

📞 Call us today at 561-316-6800

📅 Schedule a consultation: AMS.Money/Calendar

Now is the time to explore buying, refinancing, or investing with confidence.

FAQs (Buyer-Focused)

Q: How does a 0.16% drop in mortgage rates affect affordability?

A: On a $400,000 loan, it saves about $40 per month and adds $5,000–$7,000 in buying power.

Q: Is now a good time to refinance my mortgage?

A: If your current rate is above 6.5%, refinancing to today’s 6.29% could lower costs.

Q: What’s better: a 30-year or 15-year mortgage right now?

A: A 30-year offers lower payments, while a 15-year saves more on interest long-term. The right choice depends on your cash flow and goals.

Q: How do mortgage rates impact the housing market overall?

A: Lower rates increase affordability, bring more buyers into the market, and can stabilize home prices.

Final Thought: Recognize Opportunity When It Comes

The rate drop to 6.29% is more than a statistic—it’s a window of opportunity.

Whether you’re buying, refinancing, or investing, smart decisions today could mean tens of thousands in savings tomorrow.

👉 The winners in today’s housing market aren’t those who wait—they’re those who act when the numbers align.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice