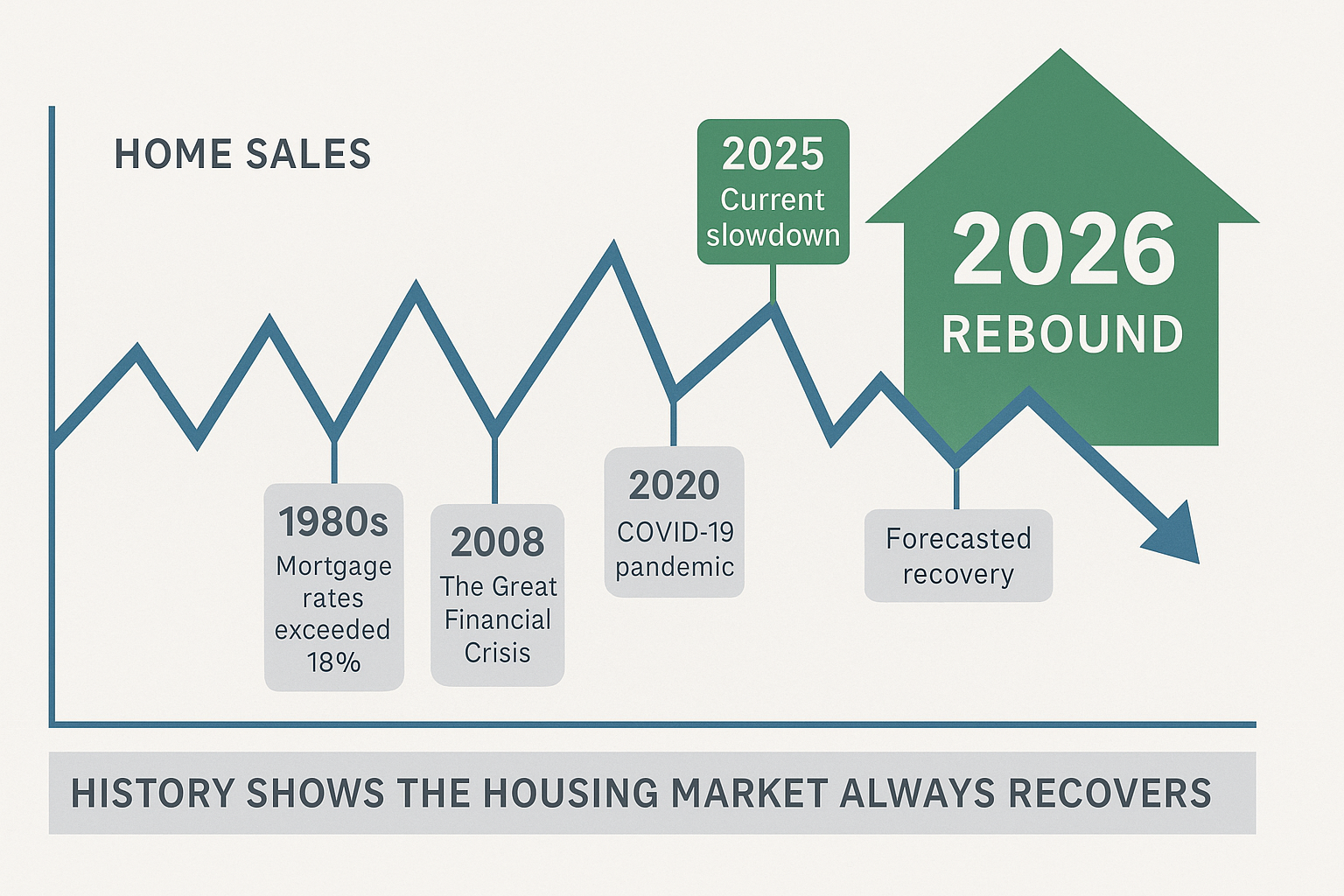

History Shows the Housing Market Always Recovers: 2025 Slowdown & 2026 Forecasts

Meta Description: Housing delistings are up, but history shows recoveries always follow. Experts predict a rebound by 2026. Here’s why—and what it means for sellers.

Introduction: Why This Market Feels Different—But Isn’t

If you’ve tried to sell your home recently, you may have noticed things aren’t moving the way they were just a few years ago. Homes that used to attract multiple offers within days are now sitting longer, with sellers reluctantly pulling listings after failing to meet price expectations.

According to Realtor.com, delistings are surging—up 38% since the start of 2025 and 48% compared to last year. For every 100 new listings in June, about 21 homes were taken off the market. In some regions, like Miami, the number was even higher, with about 27 delistings per 100 listings.

At first glance, this slowdown feels alarming. But here’s the reassuring truth: the housing market always recovers. Every downturn in modern U.S. housing history—from the high-interest-rate era of the 1980s, to the Great Recession in 2008, to the pandemic shutdown of 2020—eventually gave way to renewed growth.

In this in-depth article, we’ll explore:

-

Why history proves housing markets rebound

-

What’s happening in 2025 with rising delistings

-

Forecasts from Fannie Mae, NAR, and MBA through 2026

-

Buyer and seller psychology during downturns

-

Practical steps to prepare for the next rebound

The Current Market: A Pause, Not a Collapse

Rising Delistings Reflect Seller Hesitation

The surge in delistings doesn’t necessarily mean disaster. Instead, it reflects a gap between seller expectations and buyer affordability. Sellers, accustomed to the high-price, fast-sale conditions of 2021–2022, are often reluctant to cut asking prices. Buyers, meanwhile, are facing elevated mortgage rates and affordability challenges.

-

Key Stat: In June 2025, 21 out of every 100 new listings were withdrawn before selling.

-

Local Example: Miami ranked among the highest metro areas for delistings, highlighting affordability pressure in hot markets.

This tension creates the appearance of a “frozen” market. But historically, these pauses resolve as either prices adjust, interest rates fall, or buyer demand returns.

History Repeats: Lessons from Past Downturns

The U.S. housing market has faced many downturns. Yet in every case, recovery followed—often stronger than before.

The 1980s: Mortgage Rates Above 18%

In the early 1980s, the Federal Reserve raised interest rates aggressively to combat inflation. Mortgage rates soared past 18%, making borrowing nearly impossible for most buyers. Home sales stalled for years.

But when rates began falling in the mid-to-late 1980s, demand surged back. This episode proved that interest rate relief consistently unlocks housing activity.

2008: The Great Financial Crisis

The collapse of the housing bubble in 2008 was the most severe downturn in modern U.S. housing history. Millions of foreclosures and plummeting home values left deep scars.

Yet even this crisis gave way to recovery. By 2012–2013, prices stabilized, and demand slowly returned. Over the next decade, home values climbed steadily—culminating in the record highs of 2021–2022.

2020: The COVID-19 Shock

When COVID-19 shut down the world in March 2020, housing activity stopped overnight. Open houses disappeared, and buyers retreated.

But within months, the market roared back as remote work, low mortgage rates, and pent-up demand drove one of the fastest housing recoveries in history.

The Common Thread: Housing Always Rebounds

Despite different causes—interest rates, financial crises, pandemics—the result has always been the same: slowdowns are temporary. The fundamental drivers of housing demand—population growth, household formation, and the need for shelter—ensure that downturns don’t last forever.

2025 Housing Market: What’s Driving the Slowdown

Affordability Is the Biggest Factor

The combination of high mortgage rates and elevated home prices is the core reason sales have slowed.

-

Mortgage rates climbed rapidly in 2022, reaching levels not seen in two decades.

-

Home prices, meanwhile, have stayed sticky, keeping many buyers priced out.

This double hit has created one of the most unaffordable housing environments in recent memory.

Buyer Psychology: Waiting on the Sidelines

Buyers are hesitant for two main reasons:

-

High Monthly Payments: Even if prices stabilize, higher rates mean bigger mortgage bills.

-

Expectations of Lower Prices or Rates: Many buyers are waiting, hoping for better conditions.

This “wait-and-see” mindset reduces demand further, reinforcing the slowdown.

Seller Psychology: Holding Out for Yesterday’s Prices

On the flip side, sellers don’t want to accept lower offers, especially if they bought or refinanced at low pandemic-era rates. Many would rather delist and wait than sell for less.

This mismatch between buyers and sellers explains why listings are piling up, and why delistings are soaring.

2025–2026 Housing Market Forecasts: Expert Insights

Fannie Mae

-

2025 Sales: Projected 4.74 million

-

2026 Sales: Projected 5.23 million

-

Mortgage Rates: Expected to decline slightly—around 6.0% by 2026

-

Home Price Growth: +4.1% in 2025, +2.0% in 2026

National Association of Realtors (NAR)

-

Forecasts a 6% increase in sales in 2025 and an 11% increase in 2026

-

Predicts home prices to grow 3% in 2025 and 4% in 2026

Mortgage Bankers Association (MBA)

-

Projects sales closer to 4.3 million in 2025

-

Expects slower home price appreciation than Fannie Mae or NAR

The Consensus: A 2026 Rebound

While forecasts differ slightly, all agree on one thing: 2026 will mark a turning point. Lower mortgage rates, stabilizing prices, and improving affordability will bring buyers back into the market.

Why Housing Always Recovers: The Underlying Forces

1. Population Growth and Household Formation

New households form every year, whether through young adults moving out, families growing, or immigration. Housing demand is a demographic inevitability.

2. Limited Supply

Even during downturns, the U.S. often underbuilds housing compared to demand. This supply shortage puts upward pressure on prices once demand returns.

3. Housing as a Necessity

Unlike other assets, housing isn’t optional. Everyone needs a place to live, ensuring demand never disappears entirely.

What This Means for You (Buyers & Sellers)

For Sellers

-

Patience Pays: Historical patterns suggest recovery is near.

-

Prepare Now: Work with your agent to stage, price, and plan for relisting when conditions improve.

-

Stay Flexible: Be open to price adjustments or incentives to attract buyers sooner.

For Buyers

-

Opportunity Ahead: Slower markets often give buyers more negotiating power.

-

Lock or Wait?: If rates dip in 2026, affordability will improve.

-

Think Long-Term: Housing downturns are temporary; owning is still a wealth-building strategy.

Voice Search–Friendly FAQs

Q: Will the housing market recover in 2025?

A: Experts predict stabilization in 2025, but stronger recovery is expected in 2026 as mortgage rates decline.

Q: Why are so many homes being delisted right now?

A: Many sellers are pulling homes off the market because they aren’t getting their asking price in today’s slower market.

Q: Is now a good time to buy or sell?

A: It depends on your goals. Buyers may find opportunities in less competitive conditions, while sellers may benefit by waiting for 2026’s rebound.

Conclusion: The Cycle Always Turns

Housing downturns are never easy. For buyers, affordability is a challenge. For sellers, watching homes sit unsold is discouraging. But history—and today’s forecasts—offer reassurance: the housing market always recovers.

From the 1980s to 2008 to 2020, every slowdown gave way to renewed growth. Today’s market may feel uncertain, but the underlying demand for housing hasn’t disappeared.

As we approach 2026, declining mortgage rates and growing buyer demand are expected to kickstart the next wave of activity.

Bottom Line: If you’re waiting to sell, patience could pay off. If you’re looking to buy, opportunity may be around the corner. Either way, history shows one thing clearly: housing markets recover—and this one will too.

![]()

History Shows the Housing Market Always Recovers

Now that the market is slowing down, homeowners who haven’t sold at the price they were hoping for are increasingly pulling their homes off the market. According to the latest data from Realtor.com, the number of homeowners taking their homes off the market is up 38% since the start of this year and 48% since the same time last June. For every 100 new listings in June, about 21 homes were taken off the market.

And if you’ve made that same choice, you’re probably frustrated things didn’t go the way you wanted. It’s hard when you feel like the market isn’t working with you. But while slowdowns can be painful in the moment, history tells us they don’t last forever.

History Repeats Itself: Proof from the Past

This isn’t the first time the housing market has experienced a slowdown. Here are some other notable times when home sales dropped significantly:

- 1980s: When mortgage rates climbed past 18%, buyers stopped cold. Sales crawled for years. But as soon as rates came down, sales surged back, and the market found its footing again.

- 2008: The Great Financial Crisis was one of the toughest housing downturns in history. Sales and prices both dropped hard. Still, sales rebounded once the economy recovered.

- 2020: During COVID, sales disappeared overnight, and many people had to put their plans on hold. Yet the recovery was faster than anyone expected, with a surge of buyers re-entering the market as soon as restrictions eased.

The lesson is clear: no matter the cause, the market always rebounds.

Today’s Situation: Where We Stand Now

Over the past few years, home sales have been sluggish. And one big reason why is affordability. Mortgage rates rose at a record-breaking pace in 2022, and home prices were climbing at the same time. That combination put buying out of reach for many people. And when demand slows, home sales do too.

The Outlook: Why Things Will Improve

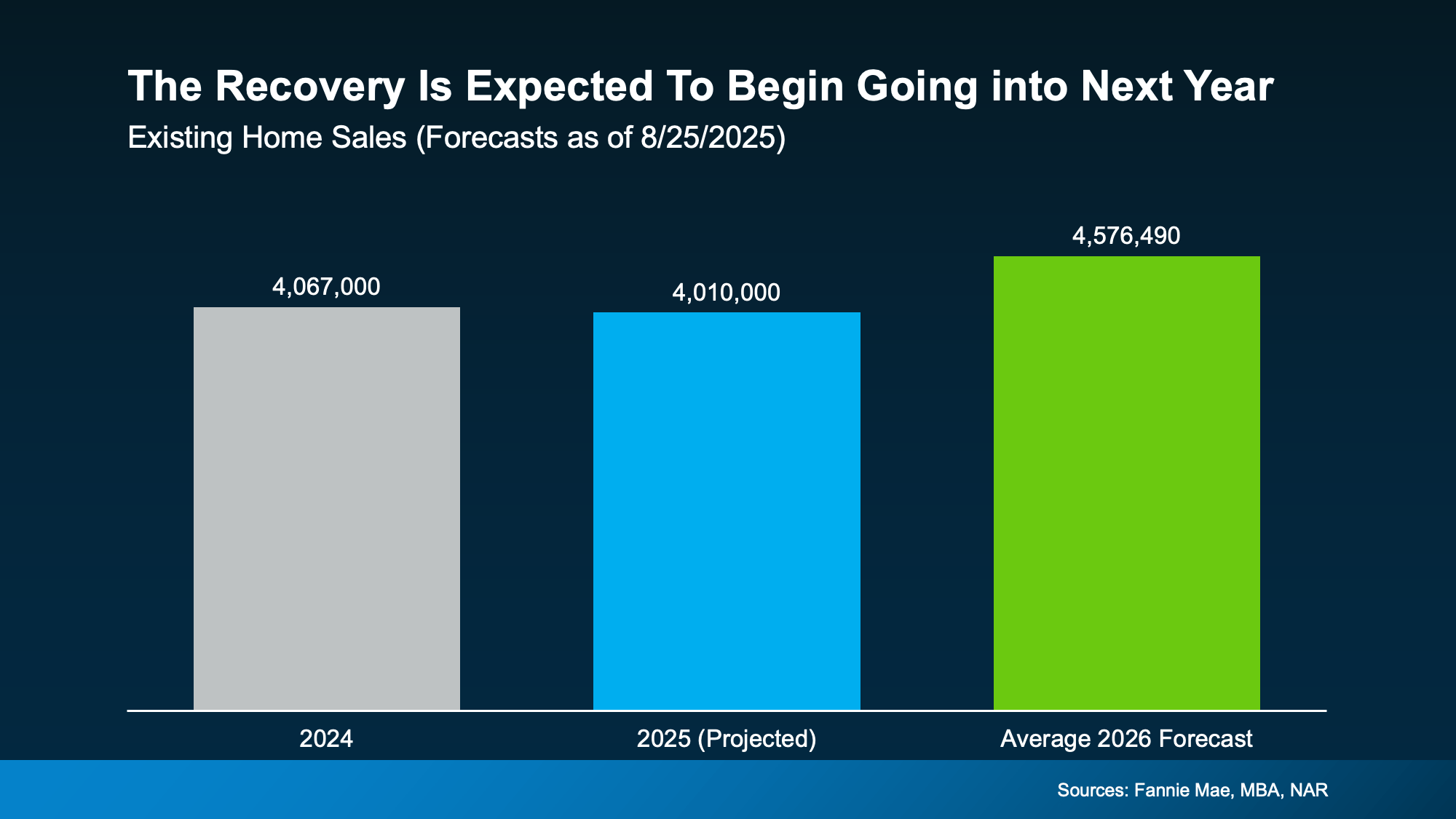

But here’s the encouraging part. Forecasts show sales are expected to pick up again moving into 2026.

Last year, just about 4 million homes sold (shown in gray in the graph below). And this year is looking very similar (shown in blue). But the average of the latest forecasts from Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR) show the experts believe there will be around 4.6 million home sales in 2026 (shown in green).

And a big reason behind that projection is the expectation that mortgage rates will come down a bit, making it easier for more buyers to jump back in.

That means what’s happening now is part of a cycle we’ve seen before. Every slowdown in the past has eventually given way to more activity, and this one will too.

That means what’s happening now is part of a cycle we’ve seen before. Every slowdown in the past has eventually given way to more activity, and this one will too.

Just like the 1980s, 2008, and 2020, today’s dip in home sales is temporary.

What That Means for You

If you’ve paused your moving plans, you did what you thought was right. Your frustration is valid. But it’s also important to remember the bigger picture. Housing slowdowns don’t last forever.

That’s where your local real estate agent comes in. Their job is to keep a close eye on the market for you. When the first signs of a rebound appear, they’ll help you spot the shift early so you can relist with confidence.

Bottom Line

If today’s housing market feels stuck, remember it’s never stayed down for good. Slowdowns end, activity returns, and people get moving again. So, let’s connect, because when the next wave of buyers shows up, you won’t want to miss it.

As activity picks up again, will you be ready to put your house back on the market, or do you need to move sooner?

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Get Pre-Approved Today