Your House Didn’t Sell. Here’s What To Do Now.

When your house doesn’t sell, it doesn’t just feel frustrating – it feels personal. You put time, money, and emotional energy into this move. You told your friends and family it was happening. And now that your listing has expired without a buyer? You’re left feeling stuck, and maybe even a little embarrassed.

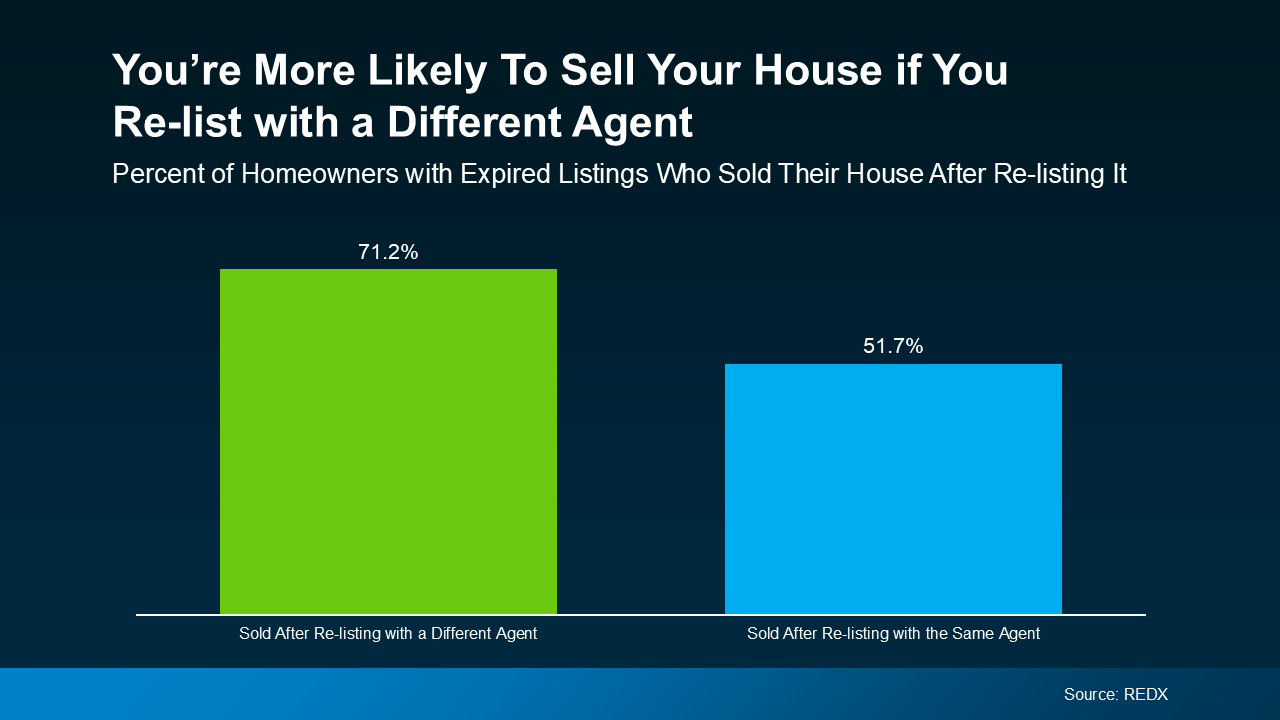

And here’s what most agents won’t tell you. Over 70% of homeowners who re-list with a different agent sell their house.

Re-list with the same agent? That stat drops to only 50%, according to the latest data from REDX. That’s like leaving the fate of your sale to a coin toss. And that’s not good enough.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better.

Same house. Different strategy. Completely different results.

Let’s break down what might’ve gone wrong – and how a fresh perspective can help you have a winning strategy this time.

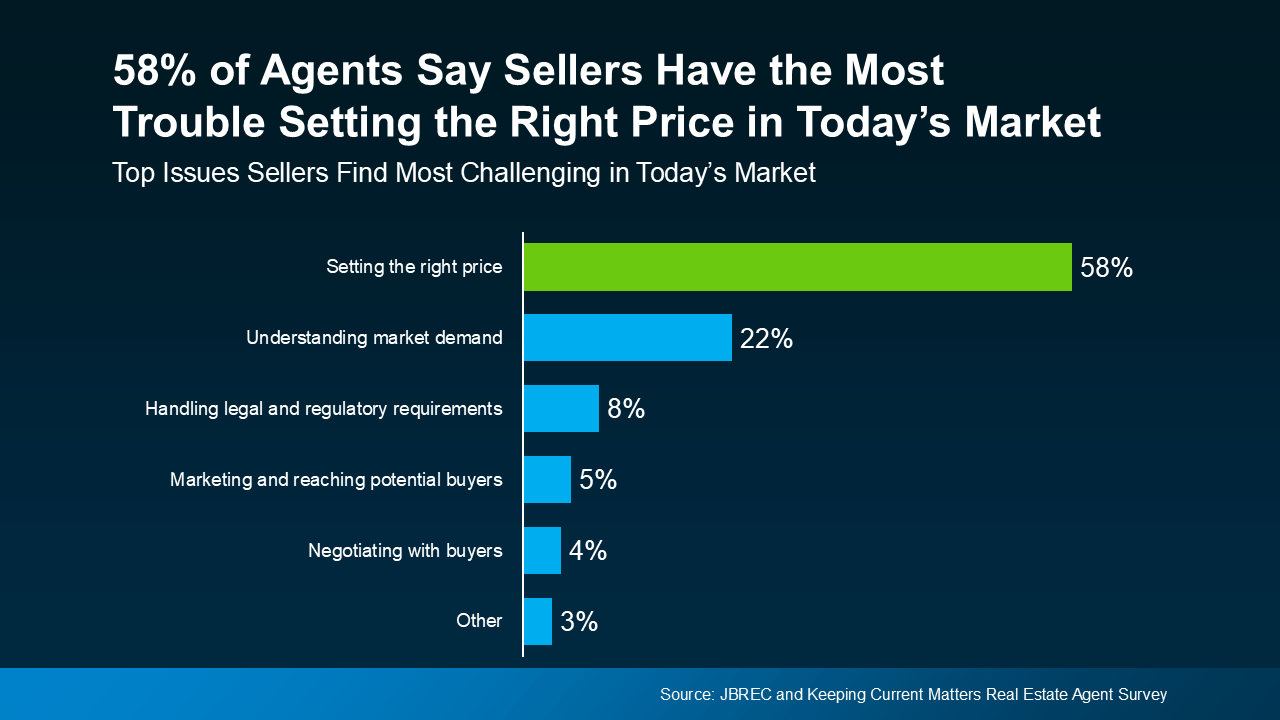

1. It Was Priced Too High

Today, homebuyers are feeling the squeeze of higher mortgage rates, so even a slightly overpriced home will get overlooked. And once your listing starts to go stale, it’s hard to regain momentum.

Missing the mark on pricing is a costly mistake – and too many homeowners are doing that very thing right now.

What we need to do now: We need to analyze the latest sales in your area to make sure you’re hitting the right number. This includes taking a hard look at real-time buyer behavior, and any feedback you got from open houses or showings your first time around. Pricing at, or even just below, current market value is a winning play because it drives more buyers to your listing – and that amps up the competition for your home.

2. It Didn’t Show Well

You only get one shot at a first impression. If the listing photos didn’t pop, the house wasn’t staged well, or it wasn’t updated, most buyers will skip over it without ever scheduling a showing. And even if buyers did show up, small things like scuffed walls, outdated light fixtures, or a wobbly doorknob can turn them away.

What we need to do now: Let’s walk through your house with fresh eyes to see if there are any areas that may have been sticking points inside and out. Sometimes taking down old drapery, some light staging, or even a fresh coat of paint can completely change how a buyer feels about the home.

3. It Didn’t Get the Right Exposure

If your home didn’t sell, chances are it wasn’t getting the visibility it deserved. Generic flyers and a few online photos aren’t enough anymore. Today’s top agents are using highly targeted digital marketing, social media strategies, custom video content, and more to get your listing in front of the right buyers at the right time.

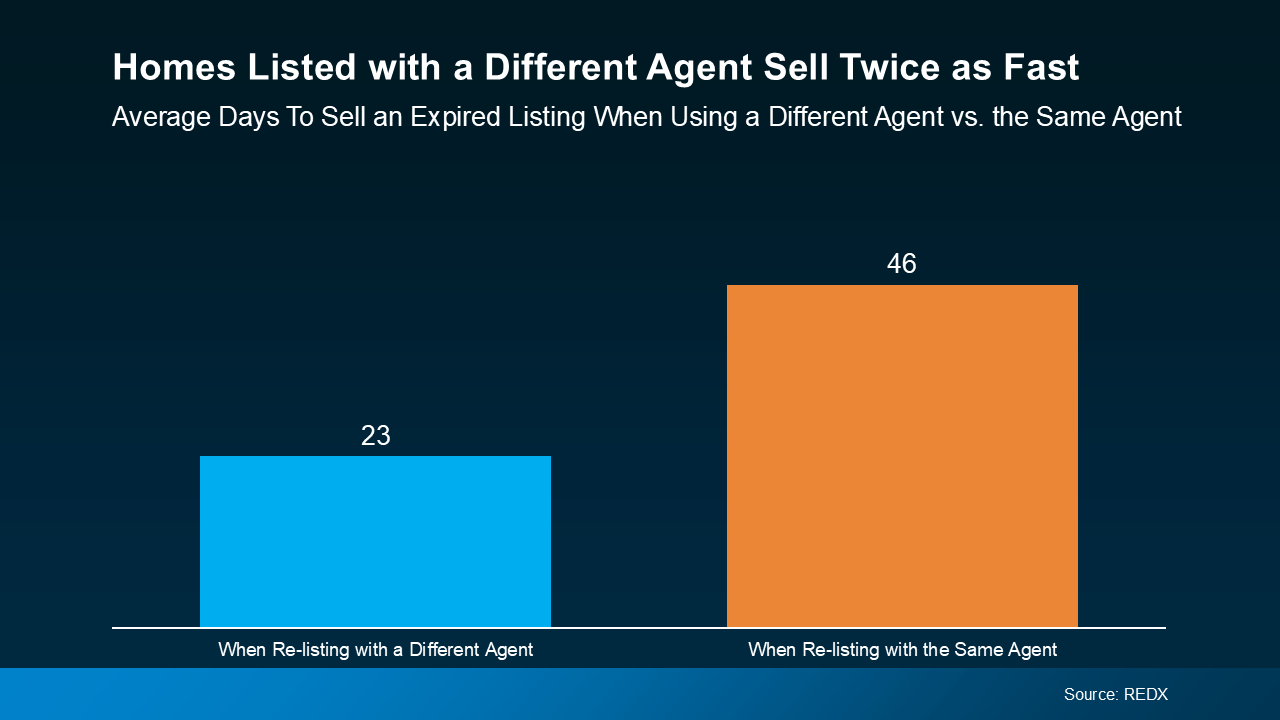

What we need to do now: We have to do more than just put your house online and hope it sells. Together, we can come up with a real plan to maximize its exposure. With the right pricing, staging, and marketing, your house will sell quickly. Here’s a real-world example (see graph below):

4. You Weren’t Willing To Negotiate

4. You Weren’t Willing To Negotiate

In this market, sellers who aren’t open to negotiating on things like closing costs, inspection repairs, or other concessions are often left behind. And if your last agent didn’t set that expectation with you, that’s a real shame.

What we need to do now: Be willing to meet buyers where they are. The goal is to get the deal done – and sometimes that means getting creative to help buyers cross the finish line. Home values have increased by over 55% over the last five years, so you likely have enough wiggle room to offer some perks without sacrificing your bottom line.

If your house didn’t sell and your listing has expired, you don’t need to give up. You just need a better plan. And a better partner.

Over 70% of homeowners who switch agents sell their house after re-listing it. That’s not a coincidence. That’s strategy.

If you’re ready for a proven approach, let’s talk so you know what to do differently – and why doing different things actually works. It’s time to get your move back on track.

Your House Didn’t Sell. Here’s What To Do Now.

There’s nothing quite like the sting of disappointment when your house didn’t sell. You cleaned. You staged. You told the world. And yet… the listing expired. The “For Sale” sign out front feels like a badge of defeat rather than an invitation. But take a deep breath. This is not the end. It’s the beginning of a smarter, sharper, winning strategy that will get your house sold—quickly, confidently, and for the right price.

Welcome to your fresh perspective.

Why Listings Expire – And What To Do About It

Many homeowners think their house didn’t sell because of the market itself. Maybe the economy was soft. Maybe the season was wrong. Maybe Mercury was in retrograde.

But more often than not, the reason an expired listing happens comes down to three crucial areas: pricing strategy, exposure, and buyer behavior. Let’s break them down.

1. Pricing Strategy – Why the Right Number Matters

A simple truth: an overpriced home scares off buyers faster than a creaky front door. Today’s homebuyers are sharper than ever. Armed with mortgage calculators in West Palm Beach, Zillow alerts, and real-time data, they can spot a bad deal instantly.

And with mortgage rates still flexing like a tired muscle, affordability is tight. Even the smallest misstep on price can sink interest.

Here’s the thing: when your price is right at or just below market value, something magical happens. You light a fire under buyers. You encourage multiple offers. You stir competition. The home becomes irresistible.

But when it’s off? Your house grows stale. Forgotten. Overlooked.

The fix? Dive into RedX data, recent comps, open house feedback, and true-time analytics. Consider your local market—yes, even the nuances of West Palm Beach. Leverage insights from a West Palm Beach mortgage broker to understand what buyers can actually afford. Then adjust that number.

Remember: A properly priced home isn’t giving up value. It’s creating demand.

2. First Impressions: The Silent Deal-Killer

First impression. It’s more than a saying—it’s the primal truth of real estate.

From the moment your listing photos hit the web to the second a buyer’s car creeps up the driveway, the mental measuring tape is out. Is this house worth it? Is this the one?

If the answer’s no—if the pictures are dark or outdated, if the bushes are scraggly, if the paint is peeling—your listing is dead before they’ve even stepped out of the car.

Consider this: curb appeal is your home’s handshake. A manicured lawn, a sparkling entry, fresh potted plants—small things that whisper, “You’ll want to live here.”

Inside? Staging is queen. A simple fresh coat of paint in the right color can add thousands to perceived value. Minor home updates—like new light fixtures or replacing that tired old ceiling fan—can change everything.

Want a buyer to fall in love? Give them a space that feels cared for, modern, and bright.

3. Exposure: Getting Seen Is Getting Sold

It’s not 1999. You can’t just put your house online, slap up a few mediocre photos, and pray.

Today’s top agents know better. They harness digital marketing, custom video content, and targeted marketing campaigns. They flood social media strategies—Facebook, Instagram, even TikTok—with professional visuals that make your house shine. They don’t hope to find the right buyer; they get your listing in front of them deliberately.

A lazy agent? They’ll post to the MLS and vanish.

A smart one? They’ll use retargeting ads, custom video content, and even influencer partnerships if necessary to crank up visibility.

If you want your house to sell—especially in competitive areas like West Palm Beach—your agent needs a 360-degree marketing assault.

And speaking of agents…

The Agent Equation: Why Switching Could Be Your Best Move

Here’s the secret you deserve to know.

RedX data shows over 70% of sellers who switch agents after an expired listing end up selling their home. Stick with the same agent? Only 50% close the deal.

Translation? If you want different results, you need a different partner.

Find an agent who understands not only your house—but also the local market, West Palm Beach’s quirks, and what it takes to unlock home values in this unique area. Someone who can advise on affordable West Palm Beach home loans, commercial mortgage broker options in West Palm Beach, and even property loan advice in West Palm Beach to help buyers feel confident.

You need someone who lives for strategy. For creativity. For the joy of turning “for sale” into “sold.”

The Buyer’s Mind: Understanding Buyer Behavior

Why didn’t your house sell? Because someone, somewhere, didn’t fall for it.

Buyer behavior is everything. Today’s buyers crave move-in ready homes. They expect style, flair, function, value.

They obsess over kitchens and closets. They panic at the thought of inspection repairs. They flinch at outdated carpet. They love smart home tech. They dream of open floor plans.

What makes them hesitate? Uncertainty. High closing costs. Fear of hidden problems.

That’s why the details matter. That fresh coat of paint? Calms nerves. Clean gutters? Suggests care. Home updates like touchless faucets or eco-friendly thermostats? Catnip.

Want to turn browsers into offers? Get inside their heads.

Negotiation: Your Secret Weapon

Many sellers secretly sabotage their own deals by refusing to flex on negotiation.

But here’s the truth: a little give can get you a lot.

Today’s buyers expect some sweetening—seller concessions, help with closing costs, or a few inspection repairs covered. If you—or your agent—were rigid the first time, that may have been the final nail in your unsold coffin.

Smart sellers see this moment as a trade: offer some perks, and you’ll make more in the end because the house will move faster. And remember—home values have soared over the past five years. You’ve got room.

West Palm Beach Spotlight: What You Need To Know

Selling in West Palm Beach? Your market is sizzling—but that comes with both opportunity and danger.

Locals are hunting for homes that feel move-in ready but affordable. That’s why tools like West Palm Beach mortgage calculators, first time home buyer loans in West Palm Beach, and flexible West Palm Beach refinancing options are in huge demand. Savvy buyers want deals—but they also want homes that look and feel like worth-every-penny investments.

And you can deliver that—if you prep the house and your agent markets it correctly.

Pro tip? Highlight local financing perks in your listing: “Eligible for Affordable West Palm Beach home loans!” or “Ask about mortgage preapproval in West Palm Beach!” Details like that get attention.

Looking to sell a business property? A commercial mortgage broker in West Palm Beach can help potential buyers finance your space faster.

In this town, local insight sells.

A Proven Approach: Your New Plan

You don’t need to wonder what went wrong anymore. Here’s the blueprint to get your house sold and finally close the deal:

-

Switch agents if your current one lacks fire, creativity, or strategy.

-

Reassess your pricing strategy using hard market data and RedX data.

-

Upgrade curb appeal, home updates, and staging to nail that first impression.

-

Ensure custom video content, digital marketing, and social media strategies boost exposure and visibility.

-

Adjust your negotiation mindset—consider seller concessions, help with closing costs, and minor inspection repairs.

-

Promote local financing options: West Palm Beach mortgage broker, property loan advice in West Palm Beach, best mortgage rates in West Palm Beach.

-

Lean on a proven approach—the kind today’s top agents live by.

Why This Time Will Be Different

When you follow this new path, you do more than put your house online and cross your fingers. You transform your house from an ignored expired listing into a can’t-miss opportunity.

Your next listing won’t sit idle. It won’t gather digital dust. With a fresh perspective, a smarter agent, sharper pricing, and world-class marketing, your house will sell quickly.

The difference? Planning. Execution. Commitment. And just the right sprinkle of local magic—especially if your buyers are dreaming of affordable West Palm Beach home loans or curious about West Palm Beach refinancing options.

The Bottom Line

You don’t need luck. You need a plan.

If your house didn’t sell, that was the past. The future looks brighter because now you have the map to success. Whether it’s tweaking your listing photos, boosting curb appeal, changing your agent, or diving deep into buyer behavior, you have the tools to win.

With the right agent to sell their house, a price that reflects true market value, and exposure that gets your home in front of hungry buyers, you can and will close this chapter—and start your next one.

The bottom line? A failed sale isn’t the end. It’s the opening scene of your next success story.

Let this time be the last time. Let this strategy be your secret weapon. And let your house get sold—the right way.

Your Next Step

Your move. Your decision. Your fresh start.

Need insight on local mortgage lenders in West Palm Beach? Curious about mortgage preapproval in West Palm Beach to ease buyer nerves? Wondering how to entice buyers with the best mortgage rates in West Palm Beach?

It’s all part of the plan. The proven approach. The way to win.

Get ready to see that “Sold” sign go up—for real this time.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice