Why Rising Foreclosure Headlines Aren’t a Red Flag for Today’s Housing Market in West Palm Beach, North Palm Beach, and Wellington, Florida FL

If you’ve been watching the news lately, you’ve likely seen alarming reports about rising foreclosures. Some headlines even say Foreclosure Activity Has Been Climbing For 10 Straight Months. That kind of phrasing is designed to grab attention. And it works.

But does it signal danger for Today’s Housing Market in West Palm Beach, North Palm Beach, or Wellington, Florida FL?

The short answer: No.

When you examine the actual data, historical comparisons, lending fundamentals, and homeowner balance sheets, the picture becomes much clearer—and far less dramatic.

This article breaks down what’s really happening, why context matters, and how this impacts buyers and sellers locally.

Understanding the Headlines: What the Data Actually Says

Let’s begin with the statistic that’s getting the most attention.

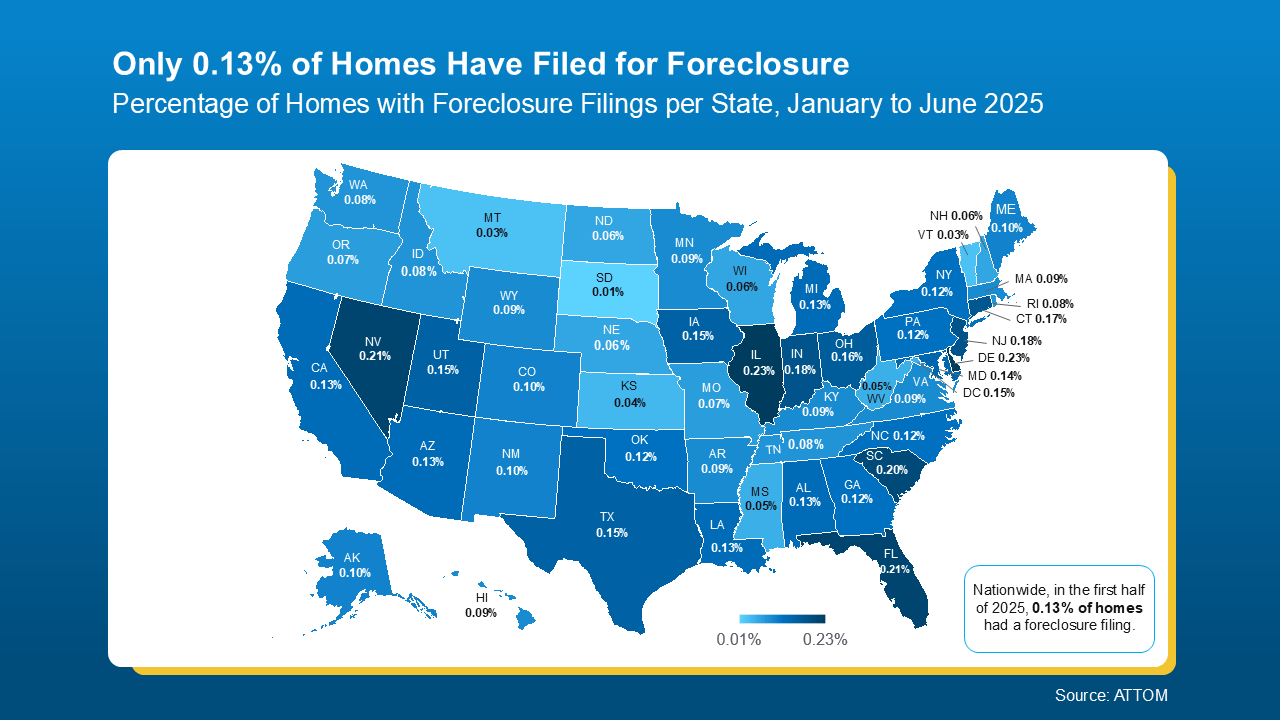

Recent reports confirm that Foreclosure Filings Are Up 32% year-over-year. Additionally, Attom Data Shows Foreclosure filings increasing across multiple states, with commentary noting that Foreclosure Activity Increased In 2025.

At first glance, that sounds serious.

However, here’s the critical context:

-

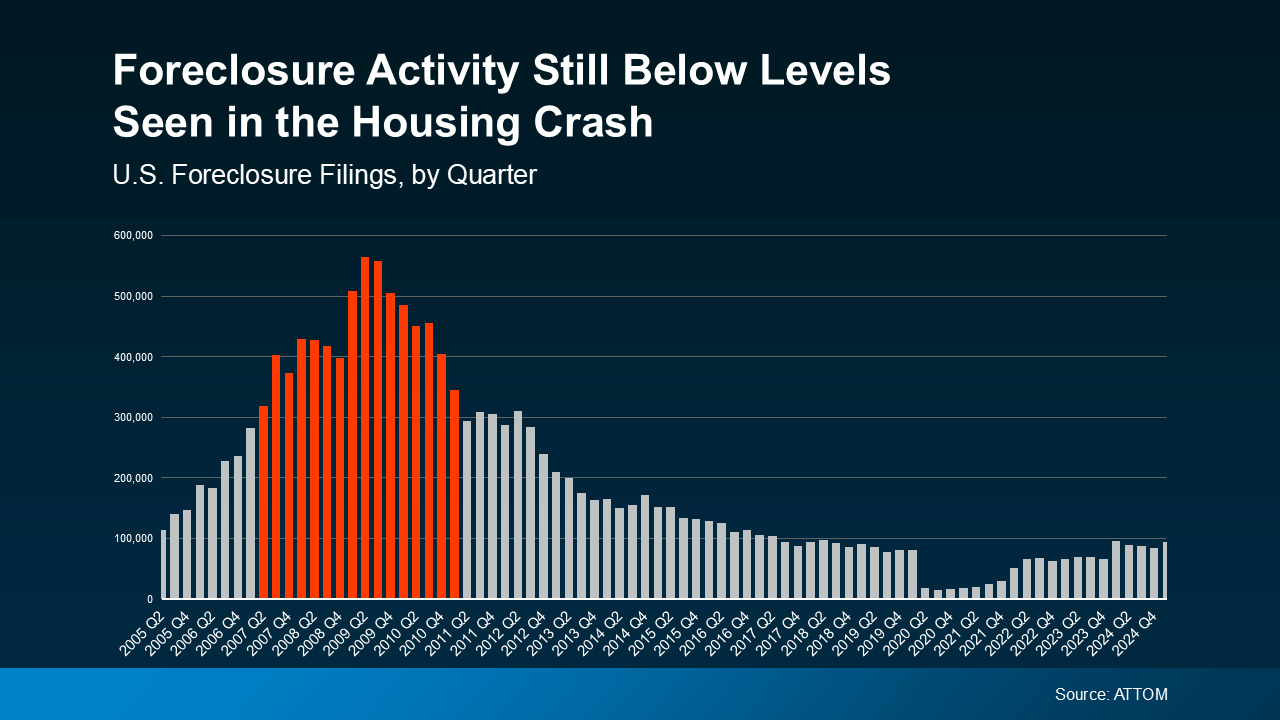

Today’s Foreclosure Numbers are still dramatically lower than what we saw during the 2008 housing crisis.

-

Foreclosure Activity Remains Well Below Pre-Pandemic Norms.

-

The increase reflects a Normalization Of The Housing Market, not systemic distress.

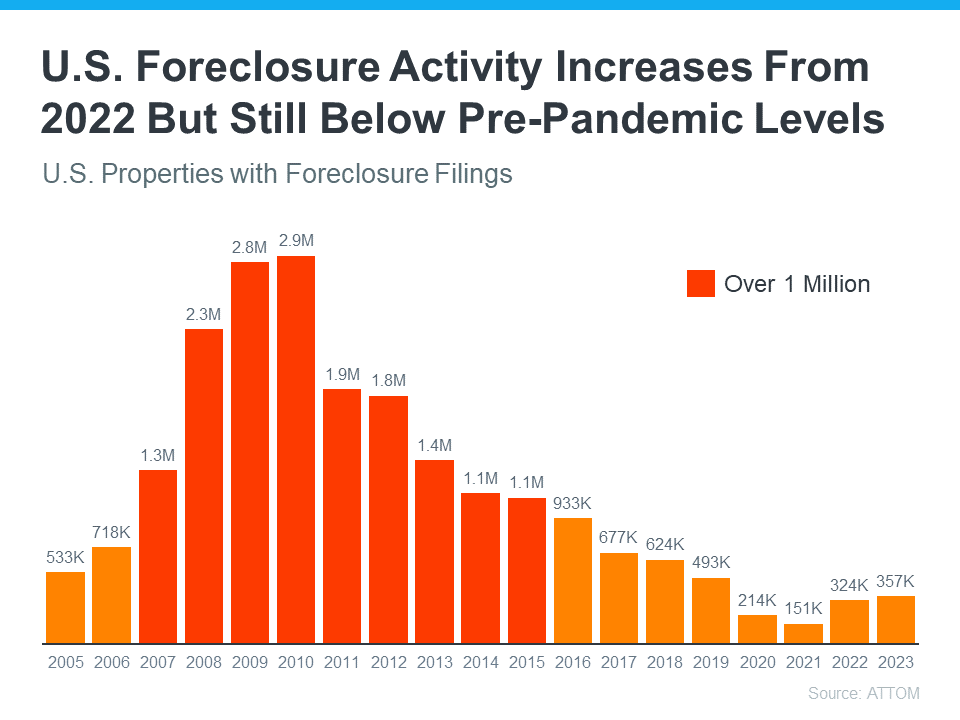

During the Great Recession, foreclosure filings exceeded one million per year. Today, filings remain a fraction of those levels.

A 32% increase sounds dramatic because the baseline was historically low during the pandemic years. When moratoriums and government protections ended, activity naturally adjusted upward.

That adjustment is not collapse. It’s normalization.

Why This Is Not 2008

To understand why this matters, we must compare structural differences between then and now.

1. Lending Standards Are Stronger

In the mid-2000s, loose underwriting allowed unqualified borrowers to obtain mortgages with minimal documentation. Risk layering was widespread. Adjustable-rate mortgages reset at higher payments. Debt-to-income ratios ballooned.

Today, Lending Standards Are Stronger across the board.

Mortgage qualification requires:

-

Verified income documentation

-

Credit score scrutiny

-

Conservative debt-to-income ratios

-

Ability-to-repay compliance

Modern underwriting is disciplined and regulated.

2. Borrowers Are More Qualified

This is one of the most important distinctions.

Borrowers Are More Qualified today than at any point leading into the previous crash. Most homeowners:

-

Have fixed-rate mortgages

-

Locked in historically low rates

-

Maintain manageable payment structures

This dramatically reduces default risk.

3. The Equity Factor

The defining difference in this cycle is Equity.

Over the past five years, Home Prices have appreciated significantly across West Palm Beach, North Palm Beach, and Wellington, Florida FL.

Even though some headlines speculate about Home Prices Down scenarios, the reality is:

-

Values remain substantially higher than pre-2020 levels.

-

The majority of owners gained significant appreciation.

-

Homeowners Have Far More Equity than during the last downturn.

And more specifically, most have High Home Equity positions.

That equity is the market’s shock absorber.

Why High Home Equity Changes Everything

In 2008, millions of homeowners were underwater—meaning they owed more than their homes were worth.

That created forced defaults.

Today is different.

Because of accumulated appreciation:

-

If hardship occurs, many owners have The Option To Sell.

-

Selling often allows them to pay off the mortgage.

-

In many cases, sellers walk away with proceeds.

That’s a critical distinction.

When people have equity, foreclosure becomes a last resort—not the default outcome.

In South Florida’s competitive environment, especially in waterfront communities of North Palm Beach and equestrian properties in Wellington, Florida FL, equity cushions are particularly strong due to sustained demand.

What’s Driving the Increase in Foreclosure Activity?

To properly analyze risk, we must separate emotional narrative from economic drivers.

The modest rise in Foreclosure Activity stems from:

-

Pandemic-era foreclosure pauses ending

-

Inflationary pressure affecting household budgets

-

Isolated financial hardship cases

But importantly:

-

There is no oversupply of Homes For Sale.

-

There is no collapse in buyer demand.

-

There is no wave of subprime adjustable-rate resets.

The market is recalibrating.

That’s why experts consistently refer to this as a Normalization Of The Housing Market.

Local Market Insight: Palm Beach County Perspective

Real estate is hyperlocal. National data doesn’t always reflect what’s happening on your street.

West Palm Beach

Inventory remains constrained relative to long-term averages. Buyer demand persists, especially among relocation buyers and international purchasers.

North Palm Beach

Luxury waterfront properties maintain pricing resilience. Equity levels remain robust due to sustained appreciation over the last five years.

Wellington, Florida FL

Equestrian estates and family homes continue attracting both domestic and international buyers, supporting property values even as transaction volume moderates.

Across these cities:

-

Today’s Foreclosure Numbers remain limited.

-

Distressed listings are not flooding the MLS.

-

Homes For Sale are still competing based on condition and pricing strategy—not desperation.

Addressing the “Home Prices Down” Fear

Whenever foreclosure headlines rise, so does the fear that Home Prices Down trends will follow.

But price depreciation requires:

-

Excess supply

-

Forced selling at scale

-

Tight credit conditions

-

Rapid demand contraction

We currently have:

-

Controlled inventory

-

Healthy buyer qualification

-

Strong equity cushions

-

Stable lending frameworks

Even in markets where prices have flattened or corrected modestly, the structural collapse conditions are absent.

In Palm Beach County, lifestyle demand, climate migration, and tax advantages continue supporting pricing stability.

The Real Role of Inventory

A crash requires excess inventory.

In 2008:

-

Construction outpaced demand.

-

Unsold inventory ballooned.

-

Foreclosures flooded the market simultaneously.

Today:

-

Builders remain measured.

-

Land constraints limit overdevelopment in coastal South Florida.

-

Distressed inventory remains minimal.

The supply-demand imbalance still favors long-term stability in many Florida micro-markets.

The Mortgage Structure Advantage

Another overlooked factor: loan composition.

Most homeowners today hold 30-year fixed-rate mortgages below 4%.

That means:

-

Payments are predictable.

-

There are no widespread rate resets.

-

Payment shock risk is limited.

This is fundamentally different from the adjustable-rate mortgage explosion prior to 2008.

When analyzing systemic risk in Today’s Housing Market, mortgage structure matters enormously.

What ATTOM’s Data Really Signals

Yes, Attom Data Shows Foreclosure filings increasing. And yes, Foreclosure Activity Increased In 2025.

But ATTOM also emphasizes that Foreclosure Activity Remains Well Below Pre-Pandemic Norms and far below crisis-era thresholds.

The language matters.

Increase ≠ crisis.

Normalization ≠ collapse.

The Psychology of Headlines

Media outlets optimize for clicks. Words like “surge” and “spike” drive engagement.

But financial decision-making requires:

-

Context

-

Historical comparison

-

Local market knowledge

-

Data literacy

That’s why working with a Trusted Real Estate Expert is critical when interpreting housing news.

When Foreclosure Might Be a Concern

Transparency is important.

Foreclosure increases become concerning if:

-

Equity evaporates rapidly

-

Unemployment surges dramatically

-

Credit availability tightens severely

-

Inventory spikes sharply

None of those macro indicators are currently aligned in Palm Beach County.

What Buyers Should Know

If you’re buying in West Palm Beach, North Palm Beach, or Wellington, Florida FL, rising foreclosure headlines do not mean:

-

Massive discounts are imminent

-

Inventory will flood the market

-

A crash is guaranteed

Instead, it means:

-

The ultra-low foreclosure period of pandemic years is adjusting.

-

The market is behaving within historical norms.

What Sellers Should Understand

Sellers must remain strategic.

Pricing still matters.

Presentation still matters.

Condition still matters.

But there is no data suggesting forced liquidation waves are about to undercut properly priced properties in our local markets.

The Financing Perspective

Mortgage conditions are central to housing stability.

Lending Practices today are conservative compared to pre-crash years.

Working with an experienced professional ensures clarity.

Christian Penner of America’s Mortgage Solutions (AMS) serves as:

His dual expertise across financing and property strategy allows buyers and sellers in Palm Beach County to interpret data accurately and act strategically.

The Importance of Expert Guidance

A knowledgeable professional can help you evaluate:

-

Your personal Equity position

-

Local Homes For Sale absorption rates

-

Financing qualification strength

-

Strategic timing decisions

A Trusted Real Estate Expert doesn’t react to headlines—they analyze conditions.

Voice Search Optimized FAQs

Is foreclosure activity rising in Florida?

Yes, Foreclosure Activity Has Been Climbing For 10 Straight Months, but Today’s Foreclosure Numbers remain historically low and consistent with a Normalization Of The Housing Market.

Are we heading toward another housing crash?

Current data does not support a crash scenario. Borrowers Are More Qualified, Lending Standards Are Stronger, and Homeowners Have Far More Equity than during the last crisis.

Are home prices falling in West Palm Beach?

While some areas have seen stabilization, widespread Home Prices Down trends comparable to 2008 are not present. Home Prices remain elevated relative to pre-2020 values.

Should I wait to buy because of foreclosures?

Distressed inventory remains limited. Waiting for a flood of discounted Homes For Sale may not align with current market realities.

The Bottom Line for Palm Beach County

Yes, Foreclosure Activity Increased In 2025.

Yes, Foreclosure Filings Are Up 32%.

Yes, Foreclosure Activity Has Been Climbing For 10 Straight Months.

But:

-

Foreclosure Activity Remains Well Below Pre-Pandemic Norms

-

Homeowners Have Far More Equity

-

High Home Equity acts as a financial buffer

-

Borrowers Are More Qualified

-

Lending Standards Are Stronger

This is not a systemic warning signal.

It is a recalibration.

In West Palm Beach, North Palm Beach, and Wellington, Florida FL, real estate fundamentals remain intact.

If you have questions about your home’s value, your financing options, or what these trends mean specifically for your property, consult Christian Penner at America’s Mortgage Solutions (AMS)—your local Mortgage Broker, Mortgage Lender, Real Estate Agent, and Real Estate Advisor.

In a market filled with noise, clarity is power.

Read from source: “America’s Mortgage Solutions (AMS)”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice