What Credit Score Do You Really Need To Buy a Home?

What Credit Score Do You Really Need To Buy a Home?

According to Fannie Mae, 90% of buyers don’t actually know what credit score lenders are looking for, or they overestimate the minimum needed.

Let that sink in. That means most homebuyers think they need better credit than they actually do – and maybe you’re one of them. And that could make you think buying a home is out of reach for you right now, even if that’s not necessarily true. So, let’s look at what the data really says about credit scores and homebuying.

There’s No One Magic Number

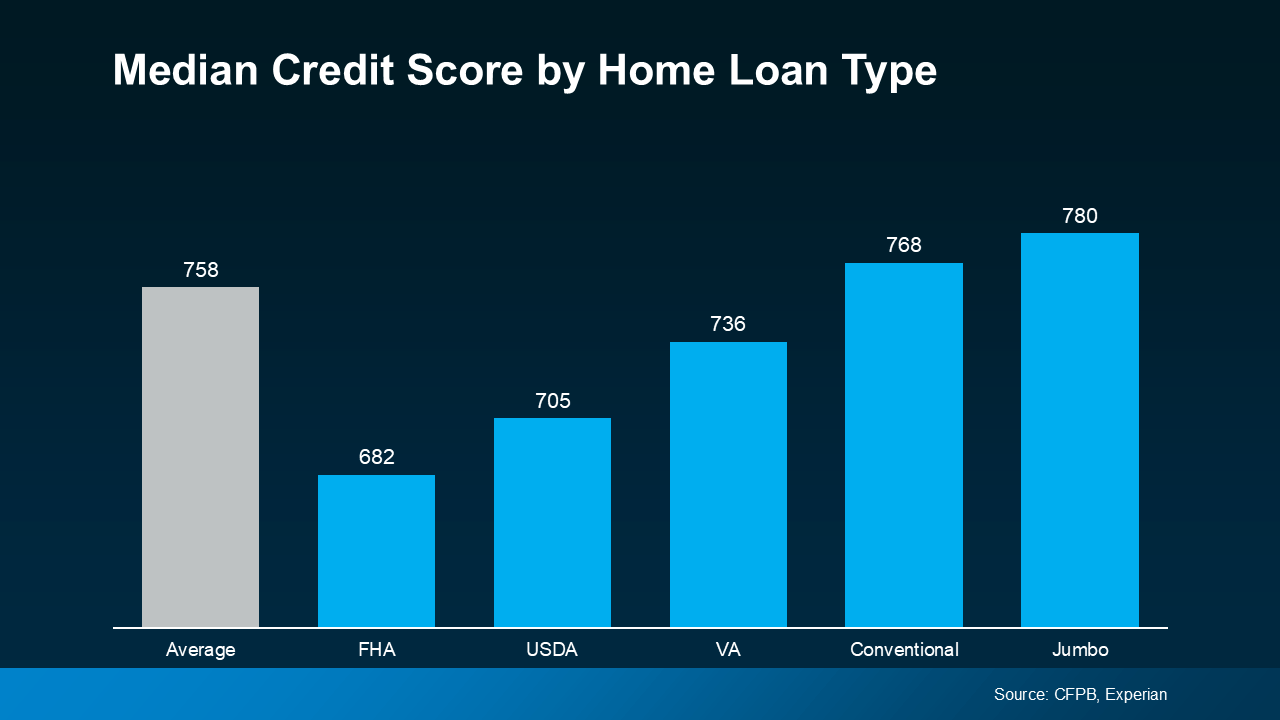

There’s no universal credit score you absolutely have to have when buying a home. And that means there’s more flexibility than most people realize. Check out this graph showing the median credit scores recent buyers had among different home loan types:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

Why Your Score Still Matters

When you buy a home, lenders use your credit score to get a sense of how reliable you are with money. They want to see if you typically make payments on time, pay back debts, and more.

Your score can impact which loan types you may qualify for, the terms on those loans, and even your mortgage rate. And since mortgage rates are a big factor in how much house you’ll be able to afford, that may make your score feel even more important today. As Bankrate says:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That still doesn’t mean your credit has to be perfect. Even if your credit score isn’t as high as you’d like, you may still be able to get a home loan.

Want To Boost Your Score? Start Here

And if you talk to a lender and decide you want to improve your score (and hopefully your loan type and terms too), here are a few smart moves according to the Federal Reserve Board:

- Pay Your Bills on Time: This is a big one. Lenders want to see you can reliably pay your bills on time. This includes everything from credit cards to utilities and cell phone bills. Consistent, on-time payments show you’re a responsible borrower.

- Pay Down Your Debt: When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible. That makes you a lower-risk borrower in the eyes of lenders – making them more likely to approve a loan with better terms.

- Review Your Credit Report: Get copies of your credit report and work to correct any errors you find. This can help improve your score.

- Don’t Open New Accounts: While it might be tempting to open more credit cards to build your score, it’s best to hold off. Too many new credit applications can lead to hard inquiries on your report, which can temporarily lower your score.

Your credit score doesn’t have to be perfect to qualify for a home loan. But a better score can help you get better terms on your home loan. The best way to know where you stand and your options for a mortgage is to connect with a trusted lender.

Read More About:

What Credit Score Do You Really Need To Buy a Home?

Introduction: Peering Behind the Numbers

In the labyrinth of homebuying, where emotions, finances, and timing converge, one gatekeeper quietly dictates the journey — your credit score. Whispered about in bank offices and fretted over during late-night online calculator sessions, the credit score has become a mythic number. It inspires dread in some and overconfidence in others. But here’s the pivotal question: What credit score do you really need to buy a home?

Spoiler: The answer is more liberating than most people imagine. While many envision an Everest-level number to clear, the reality — according to institutions like Fannie Mae and the Federal Reserve Board — is far more nuanced.

Let’s untangle the misconceptions, understand your options for a mortgage, and uncover how to get a home loan with confidence — especially if you’re exploring Affordable West Palm Beach home loans or looking for the best mortgage rates in West Palm Beach.

Chapter 1: A Misunderstood Barrier to Entry

A surprising 90% of homebuyers, according to a study by Fannie Mae, either underestimate or overestimate the credit score required to qualify for a home loan. That uncertainty has stopped countless would-be buyers from even trying to apply for a mortgage.

Many think they need a nearly perfect FICO Score to get their foot in the door. The truth? You don’t.

The Power of Perception vs. Reality

There’s no singular number etched in stone that every lender worships. The minimum credit score required depends on several variables: your loan type, the lender’s underwriting criteria, and your overall financial profile — including your available credit amount and repayment history.

This revelation changes the game. Suddenly, buying a home isn’t a far-off fantasy. It becomes an attainable milestone.

Chapter 2: The Myth of the Magic Number

Let’s obliterate the notion that there’s one omnipotent score you must achieve. A look at median credit scores across different home loan types unveils a rich tapestry of diversity. FHA loans, for instance, often accept scores as low as 580, while conventional loans may require something closer to 620–640.

Median Scores Across Home Loan Types

Different loans, different scorebands. Here’s the breakdown of common home loan types:

-

FHA Loans: Accept scores as low as 580

-

VA Loans: Often flexible with lower scores, particularly for veterans

-

Conventional Loans: Generally require scores of 620 and up

-

Jumbo Loans: Tend to demand higher scores — often 700 or more

And in West Palm Beach, with its eclectic mix of luxury condos, starter homes, and waterfront estates, there’s no shortage of lending options, from first-time home buyer loans in West Palm Beach to commercial mortgage brokers in West Palm Beach. There’s truly a fit for every scenario.

Chapter 3: Why Your Credit Score Still Holds Power

Let’s not get too relaxed, though. Just because a sky-high credit score isn’t mandatory doesn’t mean it isn’t influential. In the mortgage world, your credit score is a compass. It determines the terms on your home loan, your mortgage rate, and sometimes whether you’ll even be able to qualify for the loan.

The Domino Effect

A stronger score can unlock better conditions — like a lower interest rate, reduced private mortgage insurance (PMI), or a more flexible down payment requirement. A lower score, on the other hand, may trigger higher monthly payments or more stringent terms.

Bankrate explains it best:

“Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

This is why boosting your credit score is a priority if you’re aiming for the best mortgage rates in West Palm Beach or seeking West Palm Beach refinancing options.

Chapter 4: The Lender’s Lens

Let’s get into the psyche of lenders. When they examine your credit report, they’re not just evaluating numbers — they’re assessing risk, reliability, and responsibility.

They’re asking:

-

Do you pay your bills on time?

-

How much of your available credit amount are you using?

-

Are there derogatory marks or collection accounts?

-

Have you had multiple credit applications in a short timeframe?

In essence, they want to see a responsible borrower with a stable financial history.

If you appear as a lower-risk borrower, your odds of mortgage approval skyrocket — even more so when working with local mortgage lenders in West Palm Beach who understand the nuances of the area market.

Chapter 5: Tactical Ways to Boost Your Credit Score

So how can you become that dream client lenders love?

1. Pay Your Bills on Time

It sounds obvious, but timeliness is paramount. Even one late payment can knock points off your score. On-time payments signal maturity and stability.

2. Pay Down Your Debt

If you’re consistently utilizing a high percentage of your available credit amount, you may look financially stressed. Aim to keep usage below 30% — ideally under 10% — to signal strong management.

3. Review Your Credit Report

Errors happen. Misreported delinquencies or incorrect balances can drag your score down. Pull your credit report from all three bureaus and scrutinize every detail. Dispute inaccuracies immediately.

4. Don’t Open New Accounts Unnecessarily

Opening several lines of credit in a short time leads to multiple hard inquiries — a red flag to lenders. Unless strategically advised, avoid opening fresh accounts during the mortgage preapproval in West Palm Beach phase.

Chapter 6: Customizing the Mortgage for You

Now that the credit foundation is laid, let’s zoom out to the bigger picture — choosing a mortgage that fits like a glove.

Exploring Your Options for a Mortgage

-

Are you eligible for FHA or VA loans?

-

Will you benefit from first-time home buyer loans in West Palm Beach?

-

Do you need a jumbo loan for a luxury property?

-

Interested in West Palm Beach mortgage calculators to estimate costs?

-

Need tailored property loan advice in West Palm Beach?

The beauty of the modern mortgage market is personalization. No longer does one mold fit all.

A West Palm Beach mortgage broker can be your concierge, guiding you through loan types, helping you qualify for a mortgage, and ensuring you’re not leaving money on the table.

Chapter 7: Getting Preapproved — The Power Move

Before house-hunting in earnest, it’s wise to talk to a lender and get mortgage preapproval in West Palm Beach. Preapproval shows sellers you’re serious, gives you a concrete budget, and lets you move quickly when your dream home surfaces.

The lender will look at:

-

Your credit scores

-

Your loan type

-

Your debt-to-income ratio

-

Income stability

-

Assets and reserves

Think of it as your financial passport. And the stamp of approval opens the gates to buy a home.

Chapter 8: The Local Advantage — Why West Palm Beach Shines

In the sun-soaked, palm-lined avenues of West Palm Beach, opportunities abound. Whether you’re exploring affordable West Palm Beach home loans for a quaint bungalow or diving into commercial mortgage broker in West Palm Beach options for a mixed-use building, the landscape is rich and rewarding.

West Palm Beach’s real estate market favors the prepared and the proactive. With demand high and inventory evolving, aligning your credit score and mortgage approval early means you’ll stand tall when opportunity knocks.

Local lenders bring added value — insight into neighborhood trends, city tax structures, and competitive mortgage conditions — giving you a sharp edge.

Chapter 9: Beyond the Score — A Holistic View

Let’s step back and remember: credit scores are pivotal, but they’re one thread in a broader financial tapestry.

Lenders will also examine:

-

Employment history

-

Monthly liabilities

-

Savings for down payment and closing costs

-

Gifted funds

-

Co-borrowers and guarantors

Even with a mid-range score, strong performance in these other categories can help you qualify for the loan or negotiate better loan terms.

Chapter 10: Empowerment Through Education

Fear and misinformation keep many qualified buyers on the sidelines. But knowledge — real, up-to-date, practical knowledge — is your leverage.

By understanding how credit scores intersect with lending, by optimizing your profile, and by choosing the right partners like a trusted lender, you rewrite your narrative from “maybe someday” to “why not now?”

A higher credit score is a powerful ally, but not an immovable barrier. With deliberate action, strategic planning, and expert guidance, you can move from dreaming to buying a home — and enjoying the radiant sunsets from your West Palm Beach patio.

Conclusion: You’re Closer Than You Think

A home isn’t just a structure; it’s security, freedom, and legacy. And you’re closer to that reality than you might believe. Your credit score matters, yes — but it’s not a glass ceiling. It’s a stepping stone.

So whether you’re nurturing your credit, seeking affordable West Palm Beach home loans, or consulting with a West Palm Beach mortgage broker for personalized advice, now is the time to take bold steps forward.

Connect with a trusted lender. Talk to a trusted lender. Understand your options for a mortgage. Refuse to let assumptions dictate your financial destiny.

The keys to your future home may be just a few smart moves away.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Today’s Tale of Two Housing Markets

Today’s Tale of Two Housing Markets

Depending on where you live, the housing market could feel red-hot or strangely quiet right now. The truth is, local markets are starting to move in different directions. In some places, buyers are calling the shots. In others, sellers still hold the power. It’s a tale of two markets.

What’s a Buyer’s Market vs. a Seller’s Market?

In a buyer’s market, there are more homes for sale and not as many buyers. That means homes sit longer, buyers have more negotiating power, and prices tend to soften as a result. It’s simple supply and demand.

On the flip side, a seller’s market happens when there aren’t enough homes available for the number of people looking to buy them. Because buyers have to compete with each other to get the house they want, that leads to faster sales, multiple offers, and rising prices.

Right now, both of these scenarios are playing out, depending on where you are. So, how do you know what kind of market you’re in? Lean on a local real estate agent. They’ll explain what’s really happening in your area based on these key drivers.

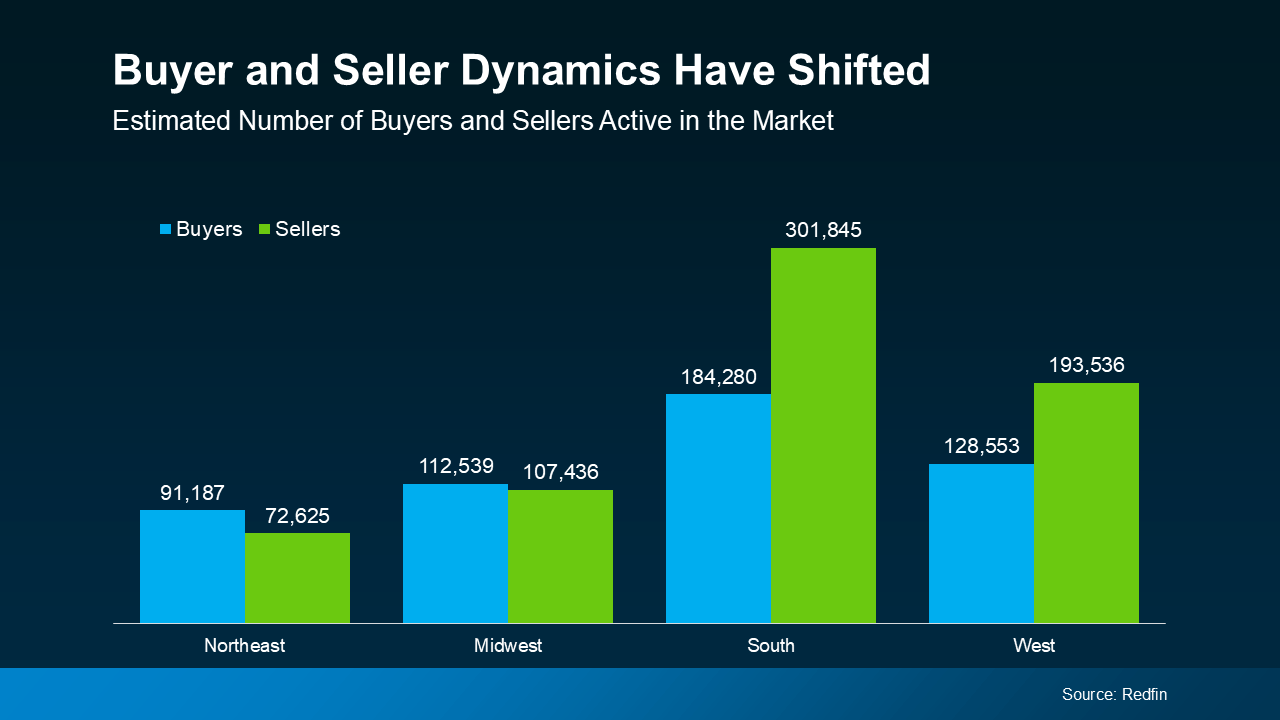

The Number of Buyers and Sellers by Region

One of the biggest factors impacting each market is the number of active buyers and sellers. According to Redfin, here’s what that looks like by region (see graph below):

Today, the Northeast and Midwest are more likely to be seller’s markets. Buyers still outnumber sellers there, and that keeps things tilted in favor of homeowners. Generally speaking, homes are selling faster and prices are rising in those areas.

Today, the Northeast and Midwest are more likely to be seller’s markets. Buyers still outnumber sellers there, and that keeps things tilted in favor of homeowners. Generally speaking, homes are selling faster and prices are rising in those areas.

But the South and West are leaning more toward buyer’s markets. There are more sellers than buyers, which means more listings to choose from and less competition among buyers.

That’s a major shift from a few years ago when sellers had the advantage almost everywhere. Today, your local conditions matter more than ever – and they can vary even from one neighborhood to the next.

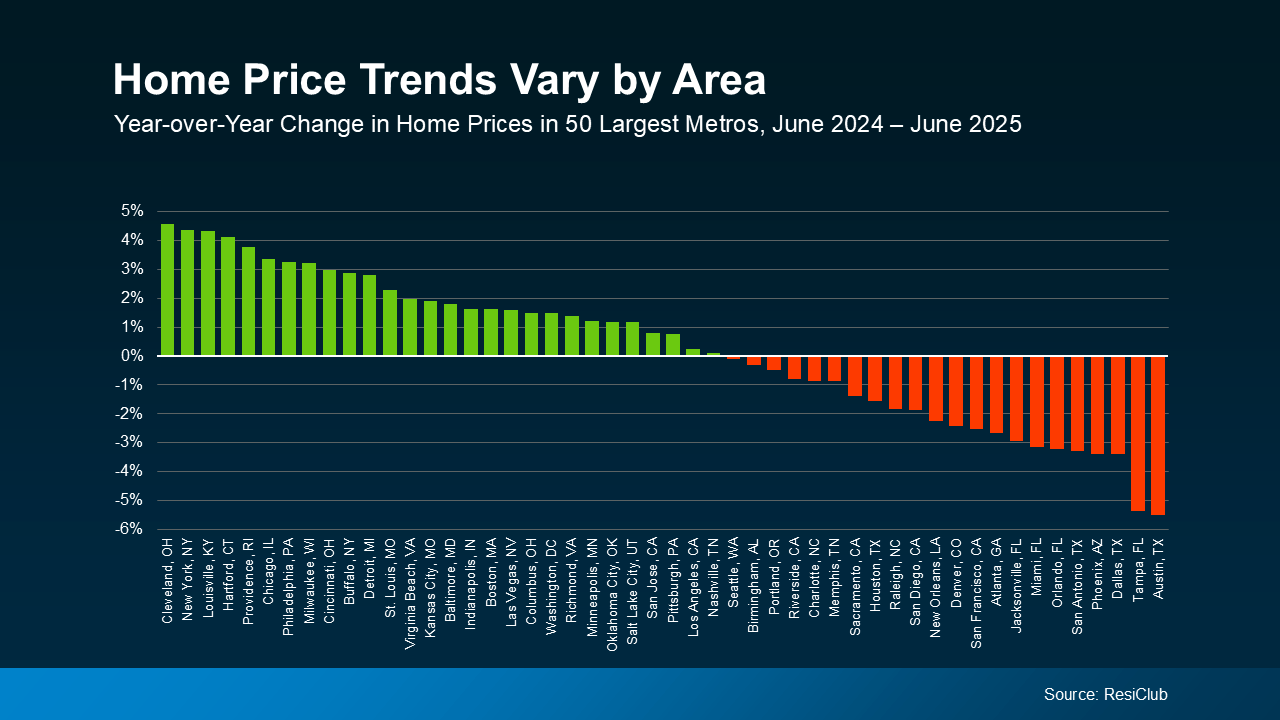

Price Trends Mirror the Buyer/Seller Divide

When inventory and buyer activity shift, so do prices. In places where demand still outpaces supply, like much of the Northeast and Midwest, prices are continuing to climb.

But in parts of the South and West where inventory is up and demand has cooled, prices are softening. And that’s a plus for buyers looking to negotiate in those areas.

Here’s the latest price data from ResiClub to show how this divide is shaking out across the top metros in the country (see graph below):

This is why it’s the tale of two markets. Roughly half of the top 50 metros are up, and half are relatively flat or down.

This is why it’s the tale of two markets. Roughly half of the top 50 metros are up, and half are relatively flat or down.

That said, don’t panic if you own a home in a market where prices are dipping. Most homeowners have built up significant equity over the past few years, and chances are you have too. So, you’re likely still come out way ahead when you sell.

Why Local Insights Matter

Even in regions that lean more buyer-friendly right now, there will be cities, towns, and even neighborhoods that don’t follow the regional trends. That’s why an agent’s local market expertise is so important. They can help you understand what’s happening all the way down to a zip code level, including:

- Whether your area is favoring buyers or sellers

- How to set the right price or craft an offer strategy based on local trends

- The best way to make your move happen, no matter what’s happening in the market

In a market where conditions vary this much from place to place, success starts with understanding every aspect of your local area. Let’s connect so you’ve got an expert in your corner who knows exactly how to guide you through your market, wherever you are.

Read More About:

Today’s Tale of Two Housing Markets

The streets tell two different stories. On one side of town, homes are flying off the shelves, signs flipping to “Sold” overnight. On the other side, listings linger, sellers anxiously dropping prices, hoping the right buyer appears. Welcome to the Tale of Two Housing Markets, a national paradox playing out in local neighborhoods across America.

The housing landscape is no longer one-size-fits-all. It has fractured—split between buyers markets and sellers markets, shaped by local conditions, regional housing trends, and the delicate balance of supply and demand. Some areas are booming, while others are simply… simmering.

A Fork in the Road: Buyers Market vs Sellers Market

Before diving deeper, let’s decode the terms steering today’s housing narrative.

In a buyers market, there are more homes for sale than there are people to buy them. That surplus injects negotiating power into the hands of the buyer. Expect longer days on market, price drops, and sellers offering incentives just to stay in the game.

In contrast, a sellers market arises when there are fewer homes available than there are buyers vying for them. The result? Multiple offers, bidding wars, faster sales, and home prices trending upward.

It’s all about inventory. It’s the heartbeat of every local housing market.

The National Scene: One Country, Two Stories

Zoom out, and the national picture reveals a curious duality. Data from Redfin and ResiClub show how unevenly the market has evolved. Cities like Boston, Minneapolis, and Cincinnati lean heavily toward sellers markets, while Las Vegas, Phoenix, and parts of Texas are deep in buyers markets territory.

In many regional markets, this divide is stark. For instance:

-

The Northeast and Midwest continue to experience low inventory and elevated demand, leading to price climbing and homes selling faster.

-

Meanwhile, the South and West are experiencing an influx of listings, tempered buyer activity, and shifting market conditions that favor buyers.

It’s not just a tale of states—it’s a tale of two housing markets that can change from one zip code to the next.

The Power of Local Market Expertise

Success in this environment demands hyper-local knowledge. An agent’s ability to understand local trends and interpret neighborhood trends can be the difference between a quick deal and a costly mistake.

That’s why it’s vital to lean on a local real estate agent. They’re fluent in the pulse of your local area, plugged into whispers before they become headlines. They can tell you if homes are selling faster, if there are more homes for sale this month, and if your neighborhood is tilting toward a buyers market or a sellers market.

Knowing when to act—and when to wait—is everything.

The Pulse of the People: Active Buyers and Sellers

The housing market isn’t just data. It’s people. Families moving for better schools, retirees downsizing, remote workers planting roots somewhere new.

According to Redfin, active buyers and sellers are behaving differently depending on their geography. In sellers markets, people are listing less frequently, fearing they won’t find a replacement home they can afford. In buyers markets, inventory is rising as would-be sellers try to capitalize before things slow further.

This behavior drives market conditions. It’s a domino effect.

Price Movements: The Tale Told in Dollars

Every movement in buyer activity or seller activity leaves footprints—namely, in price trends.

-

In seller-leaning markets, home prices are still on the rise, with some cities showing year-over-year growth in the double digits. Think price climbing.

-

In buyer-favorable regions, price softening is the trend. It doesn’t mean a crash, but rather, a cool-down. For first-time buyers, that’s a window of opportunity.

If you own a home in a market where prices are dipping slightly, don’t sweat. You’ve likely built up significant equity over the past five years. And while sellers had the advantage during the pandemic-fueled frenzy, today’s sellers still benefit from that long-term appreciation.

The Local Lens: Why Hyperlocal is the New National

The truth is, even within the same city, you’ll find two different stories. A waterfront condo may attract cash offers above asking, while a suburban townhome just ten miles away might sit idle for months.

That’s why local insights are gold. A real estate professional with local market expertise won’t rely on generalizations. They’ll zero in on zip codes, school zones, walkability scores, even planned infrastructure projects. Their expert guidance ensures your strategy is tailored—not templated.

This granular view helps you:

-

Set the right price as a seller

-

Craft a strong offer in a competitive market

-

Understand whether your block is part of a buyers market or a hidden sellers market

West Palm Beach: A Microcosm of Market Duality

Let’s take a closer look at West Palm Beach, Florida—an area that exemplifies the nation’s housing split.

Some neighborhoods here are clearly in sellers markets, with luxury estates moving fast and attracting multiple offers. But elsewhere, the scene favors buyers, especially in communities with rising inventory and newly built developments.

Navigating this dichotomy is where a mortgage partner becomes essential.

For those seeking financial clarity, there are resources such as:

-

West Palm Beach mortgage broker

-

Affordable West Palm Beach home loans

-

Best mortgage rates in West Palm Beach

-

First time home buyer loans in West Palm Beach

-

West Palm Beach refinancing options

-

Local mortgage lenders in West Palm Beach

-

West Palm Beach mortgage calculators

-

Property loan advice in West Palm Beach

-

Commercial mortgage broker in West Palm Beach

-

Mortgage preapproval in West Palm Beach

Pairing a savvy mortgage team with a local real estate agent gives buyers the confidence and agility to move quickly in your local area.

Buying or Selling? Timing Is (Almost) Everything

Whether you’re entering or exiting the market, success isn’t about luck—it’s about reading the signs.

If you’re a seller in a sellers market, don’t get greedy. Even hot markets can cool. Leverage your position while homes are selling faster and buyer activity is elevated.

If you’re a buyer in a buyers market, move strategically. With more homes for sale, you have options. You also have room to negotiate—not just on price, but on closing costs, timelines, and even post-sale repairs.

In both scenarios, equity matters. It can fuel your next purchase or create financial cushion. If you’ve built up significant equity, that leverage gives you power—whether you want to sell your home, upgrade, or refinance.

Rewriting the Script: Today’s Housing Reimagined

The traditional housing cycle has evolved. Old assumptions no longer hold. The spring buying season isn’t always the hottest. Pandemic patterns have reshaped mobility, remote work has redrawn maps, and economic pressures have created two housing markets in one nation.

Today’s buyers are savvy. Today’s sellers are cautious. And the tools to succeed—market analytics, financial insights, local partnerships—are more available than ever.

The Next Move: Smart Strategy, Local Focus

Here’s what defines success in the current environment:

-

Know your local housing market

-

Study price trends in your neighborhood

-

Watch inventory and buyer activity

-

Get preapproved for a mortgage if you’re buying

-

Price with precision if you’re selling—set the right price

And most importantly: lean on a local real estate agent. They are your front line. Your ally. They know why an agent’s role is not just transactional, but transformational.

Final Word: Chart Your Course with Confidence

The American housing market is no longer a singular story. It’s a mosaic of experiences, from coast to coast. Whether you’re a seasoned investor, a first-time buyer, or looking to sell your home, your journey is unique—and so is your neighborhood.

So in this tale of two housing markets, choose your path with care. Watch the numbers. Follow the local rhythms. And trust those who know the terrain. With the right people by your side, the right financing options at your fingertips, and an ear to the ground in your local area, you’ll write a story of success no matter which side of the market you’re on.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

The Latest Mortgage Rate Forecasts

The Latest Mortgage Rate Forecasts

Some Highlights

- If you’re tempted to delay your move in hope that mortgage rates will come down, you may want to rethink that strategy based on the latest forecast.

- Experts say mortgage rates are projected to stay in the 6s this year. So don’t expect a big drop.

- If you want to talk about what this means for your move, let’s connect. As forecasts change, having an expert who can keep you updated is essential.

More About:

The Latest Mortgage Rate Forecasts

A Pulse Check on the Mortgage Market

In the ever-evolving symphony of the real estate world, few notes hit harder than the shift in mortgage rates. A mere quarter-point swing can alter a buyer’s trajectory, an investor’s projection, or a homeowner’s financial peace. As we cross into the latter half of the year, the spotlight is firmly fixed on the latest mortgage rate forecasts—and for good reason. The stakes are high, the volatility is real, and the guidance? Essential.

Welcome to the macro-micro confluence of trends, predictions, and pivotal decisions. The terrain is textured, but clarity is coming. Let’s explore how the latest forecast is shaping the housing landscape and what it means for those standing at the crossroads of a home buying decision.

Chapter 1: Decoding the Numbers — The Latest Mortgage Rate Reality

The headlines are buzzing. Pundits are speculating. But beneath the noise lies a more consistent refrain: mortgage rates aren’t crashing—they’re plateauing. For many, the anticipation of a big drop has been the linchpin of their wait-and-see approach. But according to the latest mortgage rate forecasts, patience may not pay off.

The national average for a 30-year fixed mortgage hovers comfortably in the 6% range. Not 4%. Not 3%. And certainly not a sudden return to pandemic-era lows. Most forecasts pin rates in the mid to high 6s, with minor oscillations influenced by inflation metrics, labor reports, and Federal Reserve commentary.

Chapter 2: Reading Between the Forecasts — What the Experts Say

Experts say the market has entered a stage of recalibration. There’s no tsunami of rate drops coming. The conditions that sparked near-zero rates—global panic, fiscal stimulus, emergency Fed action—are no longer in play.

What we’re seeing now, according to every seasoned real estate expert, is a return to historic norms. If your vision of ideal rates is tied to 2.65%, it’s time to update the lens. Historically, 6-7% interest rates are not only common—they’re stable. That kind of stability brings predictability, which buyers and lenders alike crave.

Chapter 3: No Time to Wait — Why You Shouldn’t Delay Your Move

There’s a common misconception circulating: “I’ll just wait until rates drop.”

But waiting can be costlier than acting.

While you’re in holding mode, prices continue to climb. Competition stays fierce. Inventory remains constrained. And when rates do eventually tick downward—even slightly—expect a floodgate of demand to open. That surge? It could nullify any benefit a rate reduction might bring.

The real takeaway: don’t delay your move banking on a myth. Instead, secure what you can now, within your means, and lock in a payment before competition skyrockets again.

Chapter 4: The Elusive Big Drop — Stop Chasing Shadows

Is a big drop in mortgage rates coming?

Unlikely. The economic gears are turning in a way that doesn’t support dramatic dips. Inflation is moderating, but it’s not vanquished. The Fed is treading carefully. And lenders are pricing in risk, not optimism.

Chasing a big drop could leave you stranded in a market that’s left you behind. Better to act while the road is open than wait for a shortcut that may never appear.

Chapter 5: Time to Rethink Strategy

Home buying isn’t a sprint; it’s a game of strategy. With mortgage rate forecasts cementing in the 6% range, it’s time to rethink strategy—from financing to offer structure.

Think about adjustable-rate mortgages. Consider buying down points. Explore hybrid loans. And, if you’re in South Florida, consult a West Palm Beach mortgage broker who can customize your loan solution to fit your unique needs.

The name of the game now is creativity and adaptability. Not delay. Not rigidity.

Chapter 6: Navigating the Terrain With a Real Estate Expert

In uncertain climates, guidance is gold.

A real estate expert doesn’t just interpret trends—they help you capitalize on them. With daily insights into updated information, hyper-local market shifts, and the true temperature of buyer competition, their role is now more pivotal than ever.

If you’re unsure where the numbers are heading, or how to align your goals with current conditions, leverage the insight of someone who walks the market every day.

Chapter 7: Making a Confident Home Buying Decision

The perfect rate? It’s the one you can afford, secure, and sleep peacefully with.

Every home buying decision is personal, financial, and psychological. It’s not just about the latest mortgage rate—it’s about your timeline, your job security, your savings cushion, your monthly payment comfort zone.

Don’t let fear or media headlines shape your decision. Let your lifestyle, your goals, and your personal economy guide you.

Chapter 8: Let’s Talk Interest Rates

Interest rates are affected by more than just Fed hikes. Bond markets, global debt, inflation expectations, and economic data all play a role. And while some indicators may hint at relief in the long-term, the current climate suggests we’re in for a long plateau.

The truth? A stable interest rate market is actually good. It allows buyers to plan, negotiate, and purchase with confidence.

Chapter 9: A Hyper-Local Lens — The West Palm Beach Forecast

Step into West Palm Beach, where the sun is hot, the listings are competitive, and loan options are as diverse as the architecture.

Here’s where things get nuanced.

Buyers seeking affordable West Palm Beach home loans aren’t just hunting for lower rates—they’re seeking flexible structures, community-based lenders, and local insights. The same applies to those shopping for the best mortgage rates in West Palm Beach. It’s not just about the APR—it’s about who can close fast, fund efficiently, and understand the local market pressures.

Whether you’re tapping into first time home buyer loans in West Palm Beach or exploring West Palm Beach refinancing options, the key is understanding your lending ecosystem.

Chapter 10: Know Your Resources

Tap into the goldmine of tools available:

-

West Palm Beach mortgage calculators help you project payments with real-time updates.

-

Property loan advice in West Palm Beach offers personalized insight based on neighborhood trends.

-

Seeking funding for a retail buildout or a small office space? A commercial mortgage broker in West Palm Beach is your go-to.

-

Looking for competitive edges? Local mortgage lenders in West Palm Beach often have access to exclusive regional products.

-

Ready to make offers? Get your mortgage preapproval in West Palm Beach and boost your buying power.

Chapter 11: Buyer Profiles and Smart Strategy

Every buyer is unique—and every strategy should be too.

First-time buyer? Lean into education, lender relationships, and down payment assistance programs.

Upgrading? Focus on your net equity gain and how to reinvest it.

Refinancing? Crunch the numbers. Sometimes a slight drop in the latest mortgage rate can still offer big savings over time.

Relocating to Florida? Tap into the climate knowledge of your West Palm Beach mortgage broker to avoid common pitfalls and capitalize on timing.

Chapter 12: The Shape of Tomorrow — Tracking Housing Market Trends

What do the housing market trends say?

Inventory is still tight, but gradually building. Demand remains strong, especially in lifestyle-centric cities like West Palm. Homebuilders are ramping up, but materials and labor costs continue to pinch timelines.

Overall? It’s still a seller-favoring market, but the balance is shifting. As more listings hit the market, and mortgage rate forecasts stabilize, buyers are beginning to reclaim some leverage.

The takeaway: the market isn’t crashing. It’s maturing.

Chapter 13: When to Move Now

If you’ve been debating, now is the time to move now.

Why?

Because stability has returned. Because timing the market is a gamble. Because rate lock protections can offer security. Because buying now means building equity sooner. And because waiting for perfection often leads to missed opportunity.

The right time is the time when your finances, lifestyle, and market reality align—not when you see a magical number on a mortgage chart.

Chapter 14: Conclusion — Clarity Through the Chaos

In a year where hope, headlines, and hesitation often collide, clarity is your superpower. The latest mortgage rate forecasts may not dazzle with promises of rock-bottom financing, but they offer something better: dependability. Predictability. A framework for decisive action.

So whether you’re navigating interest rates, making a home buying decision, connecting with a West Palm Beach mortgage broker, or simply browsing listings with cautious optimism—know this:

This market favors those who act intelligently, not impulsively. Who lean into logic, not lore. And who partner with professionals who can cut through the noise.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Don’t Make These Mistakes When Selling Your House

Don’t Make These Mistakes When Selling Your House

Are you thinking about selling your house? Some common mistakes today can make the process more stressful or even cost you money.

Fortunately, they’re easy to avoid, as long as you know what to watch for. Let’s break down the biggest seller slip-ups, and how an agent helps you steer clear of them.

1. Overpricing Your House

It’s completely natural to want top dollar for your house, especially if you’ve put a lot of work into it. But in today’s shifting market, pricing it too high can backfire. Investopedia explains:

“Setting a list price too high could mean your home struggles to attract buyers and stays on the market for longer.”

And your house sitting on the market for a long time could lead to price cuts that raise red flags. That’s why pricing your house right from the start matters.

A great real estate agent will look at what other homes nearby have sold for, the condition of your house, and what’s happening in your market right now. That helps them find a price that’s more likely to bring in buyers, and maybe even more than one offer.

2. Spending Money on the Wrong Upgrades

The housing market has nearly a half million more sellers than buyers according to Redfin. That means you have more competition as a seller and may have to do a bit more to get your house ready to sell. But not all projects are going to be worth it. If you spend money on the wrong projects, it could really cut into your profit.

A local real estate pro knows what buyers in your area are really looking for, and they can help you figure out which projects are worth it, and which ones to skip. Even better, they’ll know how to highlight any upgrades you make in your listing, so your house stands out online and gets more attention.

3. Refusing To Negotiate

Now that inventory has grown, it’s important to stay flexible. Buyers have more options – and with it comes more negotiating power. U.S. News explains:

“If you’ve received an offer for your house that isn’t quite what you’d hoped it would be, expect to negotiate . . . make sure the buyer also feels like he or she benefits . . . consider offering to cover some of the buyer’s closing costs or agree to a credit for a minor repair the inspector found.”

That’s where your agent comes in. They’ll help you understand what buyers are asking for, what’s normal in today’s market, and how to find a win-win solution. Sometimes making a small compromise can keep the deal moving and help you move on to your next chapter faster.

4. Skipping Research When Hiring an Agent

All of these mistakes are avoidable with the help of a skilled agent. So, you want to be sure you’re working with the right partner. Still, according to the National Association of Realtors (NAR), 81% of sellers pick the first agent they talk to.

Many homeowners may skip basic steps like reading reviews, checking sales history, and interviewing a few agents. But that’s a mistake. You want someone you know you can rely on – someone with a good track record. The right agent can help you price your house right, market it well, and sell it quickly (and maybe for more money).

Selling a house doesn’t have to be stressful, especially if you have an experienced agent by your side. Let’s connect so you have an expert to help you avoid these common mistakes and make the most of your sale.

What’s one thing you’d want expert advice on before putting your house on the market?

More About:

Don’t Make These Mistakes When Selling Your House

Selling your home is a thrilling and transformative moment. Yet amidst the flurry of packing tape, open houses, and daydreams about your next address, there’s a minefield of missteps that could cost you dearly—emotionally and financially. In the shifting market we find ourselves in, it’s never been more crucial to navigate the sale with precision, patience, and power.

Here’s a comprehensive breakdown of the major mistakes sellers make—and how to steer clear of them—so you can sell your house smart, fast, and for top dollar.

1. Overpricing: The First (and Most Costly) Mistake

Every homeowner wants top dollar for your house. It’s only natural. Years of renovations, memories, and meticulous care seem priceless. But when it comes to setting a list price, emotions need to step aside. The housing market is not sentimental—it’s strategic.

Overpricing can backfire spectacularly. When a home lingers on the market, it sends a clear signal to home buyers: something’s wrong. According to Investopedia, overpricing often results in fewer showings, prolonged listing periods, and dreaded price cuts that chip away at your leverage.

An Experienced agent understands the delicate dance of pricing your house right. They perform nuanced market research, analyze the condition of your house, study the sales history of comparable properties, and synthesize the current market conditions. They know when to list high for a bidding war or lean conservative to attract attention quickly.

Pricing your house right from the outset means less time waiting and more time planning your next move.

2. Ignoring the Importance of Home Presentation

Want to stand out online? You’ll need more than a few fresh flowers and some ambient music playing during showings.

To get your house ready to sell, you must embrace the art of staging and the science of first impressions. With more inventory flooding the market than in recent years, your home needs to pop—on camera and in person.

From sprucing up curb appeal to ensuring the lighting flatters every room, even the smallest details matter. Home upgrades don’t need to be extravagant. What’s essential is strategy.

Before you start ripping out countertops or ordering new flooring, consult with a local real estate pro. They understand buyer psychology and regional expectations. They’ll tell you which upgrades increase value—and which ones won’t.

More importantly, they know how to highlight upgrades in your listing and photography, boosting online visibility and increasing foot traffic. Better exposure means more interest, more showings, and potentially multiple offers.

3. Wasting Money on the Wrong Renovations

Not all renovations pay dividends. Overspending on luxurious, niche improvements can chip away at your seller’s profit and leave buyers underwhelmed.

The key lies in balance. Tackle minor repairs, modernize outdated fixtures, and aim for clean, neutral design choices that appeal to the broadest audience.

A Skilled Agent or West Palm Beach mortgage broker—especially one seasoned in your specific market—can help you prioritize. They’ll advise you on the ROI of new flooring versus repainting, or whether energy-efficient appliances are worth the investment.

This kind of expert advice is golden.

4. Failing to Factor in Negotiation

Too many sellers dig their heels in, refusing to flex during negotiations. But remember: buyers have options. And with Buyers’ Negotiating Power growing in today’s housing market, rigidity is risky.

U.S. News highlights the importance of compromise. Maybe the buyer requests a credit for repairs after inspection. Or perhaps they ask you to cover closing costs to sweeten the deal.

These aren’t defeats—they’re strategic plays.

Your agent is your tactical advisor here. They understand how to negotiate offers that benefit both parties. They’ll help you keep your bottom line intact while moving the deal forward. Sometimes a minor concession now means a faster close and fewer complications later.

5. Going Solo: The Danger of Selling Without a Guide

Selling your house without a seasoned guide is like navigating a stormy sea without a compass.

Many sellers skip the crucial step of hiring an agent, thinking they’ll save money. But the data proves otherwise. The National Association Of Realtors (NAR) reports that homes sold with the help of a skilled agent typically sell for significantly more than FSBO (For Sale By Owner) listings.

The benefits are manifold. A great real estate agent brings savvy marketing, negotiation expertise, and a robust network of connections. They manage everything—from open houses to appraisals to paperwork—with precision.

The right real estate agent does more than just help you sell. They increase value, reduce stress, and maximize potential.

6. Not Doing Due Diligence When Hiring an Agent

Here’s a stunner: 81% of sellers choose the first agent they speak with. That’s a gamble with one of your most valuable assets.

Interviewing agents is essential. Examine their track record, read agent reviews, and ask about their listing strategy. Are they seasoned in your neighborhood? Have they sold homes in your price range? Do they understand the pulse of your city?

Your right partner should demonstrate insight, professionalism, and the hustle to get results.

7. Underestimating the Power of Marketing

Marketing your home is not just about sticking a sign on the lawn and uploading a few photos online. It’s a comprehensive, multi-channel effort that starts with professional photography and extends to virtual tours, social media ads, and targeted email campaigns.

In a tech-savvy era where online visibility makes or breaks deals, your listing price must be paired with stunning visuals, compelling copy, and a call to action that converts.

A real estate agent well-versed in digital marketing can launch your listing into the right feeds, inboxes, and search results. They’ll create buzz, build momentum, and drive interest from buyers who are pre-approved, primed, and ready to act.

8. Forgetting About Pre-Approval on the Buyer Side

Sellers often focus so much on their own checklist that they forget to evaluate buyer readiness.

A qualified West Palm Beach mortgage broker can verify whether a buyer has obtained mortgage preapproval in West Palm Beach. This distinction is critical. Prequalified isn’t the same as preapproved.

If your buyer hasn’t done their financial homework—secured an Affordable West Palm Beach home loan, checked with local mortgage lenders in West Palm Beach, or used West Palm Beach mortgage calculators—the deal might collapse late in the process, costing you time and money.

9. Neglecting Local Market Nuances

Not all markets are created equal. Selling your house in a beachside condo community in West Palm is different from offloading a suburban ranch in Ohio.

Knowing your neighborhood’s quirks is crucial. That’s where a local real estate pro shines. They understand how inventory, buyer demand, school districts, and seasonality affect your listing.

An agent who knows West Palm inside out can also connect you with the best Property loan advice in West Palm Beach or even introduce a trusted Commercial mortgage broker in West Palm Beach if your property fits that bill.

10. Forgetting to Plan Your Next Steps

Here’s something many sellers don’t consider until it’s too late: what comes next?

Are you upsizing? Downsizing? Renting for a while?

If you’re buying again, start scouting financing now. Look into First time home buyer loans in West Palm Beach if applicable, explore West Palm Beach refinancing options, and study the best mortgage rates in West Palm Beach available today.

This isn’t just about getting ready to sell—it’s about being ready to move forward with clarity and confidence.

11. Letting Emotions Run the Show

Selling a home can stir nostalgia, pride, and even anxiety. It’s easy to overvalue your home based on emotion.

But emotion rarely wins at the negotiation table.

Lean on your agent for impartial guidance. Their job is to remove the emotion, read the market, and give you expert advice rooted in data, not feelings.

They’ll tell you when to counter. When to accept. When to walk away. That kind of objectivity is priceless.

12. Ignoring the Numbers That Matter

Sellers often overlook the importance of running the numbers like a CFO.

What are your estimated closing costs? How much equity do you have? What are the tax implications? Will your sale proceeds cover your next purchase?

Use West Palm Beach mortgage calculators to gauge affordability. Review your payoff amount. Estimate your seller’s profit after fees and expenses. Ask your West Palm Beach mortgage broker to help you forecast various outcomes.

The more informed you are, the better decisions you’ll make—without surprises at the finish line.

13. Being Unavailable or Uncooperative

Showings are inconvenient. Negotiations are stressful. But inflexibility kills momentum.

Buyers want access. They want answers. They want a seller who’s engaged.

Be responsive. Be open to feedback. Be ready to act when opportunity strikes.

And most of all—trust your agent to manage the chaos while you focus on the outcome.

Final Thoughts: Selling Smart in Today’s Market

In today’s complex, competitive housing market, selling a house is no longer a DIY project. It’s a strategic transaction. A blend of timing, presentation, pricing, and negotiation—backed by professionals who know how to get results.

Avoiding common seller mistakes requires foresight, planning, and the help of a skilled agent. With the right preparation and partnerships, you can move from “For Sale” to “Sold” without leaving money on the table.

Ready to sell smarter, not harder? Let the experts help you shine.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Why a Newly Built Home Might Be the Move Right Now

Why a Newly Built Home Might Be the Move Right Now

Are you looking for better home prices, or even a lower mortgage rate? You might find both in one place: a newly built home. While many buyers are overlooking new construction, it could be your best opportunity in today’s market. Here’s why.

There are more brand-new homes available right now than there were even just a few months ago. According to the most recent data from the Census and the National Association of Realtors (NAR), roughly 1 in 5 homes for sale right now is new construction. So, if you’re not looking at newly built homes, you’re missing out on a big portion of what’s available.

And with more new homes on the market, builders are motivated to sell their current inventory. As a result, many are taking steps to draw in buyers.

Builders Are Cutting Prices

According to Buddy Hughes, Chairman of the National Association of Home Builders (NAHB):

“Almost 40% of home builders reduced sales prices in the last month . . .”

That means builders are being realistic about today’s market and adjusting to what buyers can afford. It’s their way to keep their inventory moving.

So, builders may be more willing to negotiate price than you’d expect – and that means your dollar may go further if you buy a newly built home. Lean on your agent to see what’s available and what incentives builders are offering in and around your area.

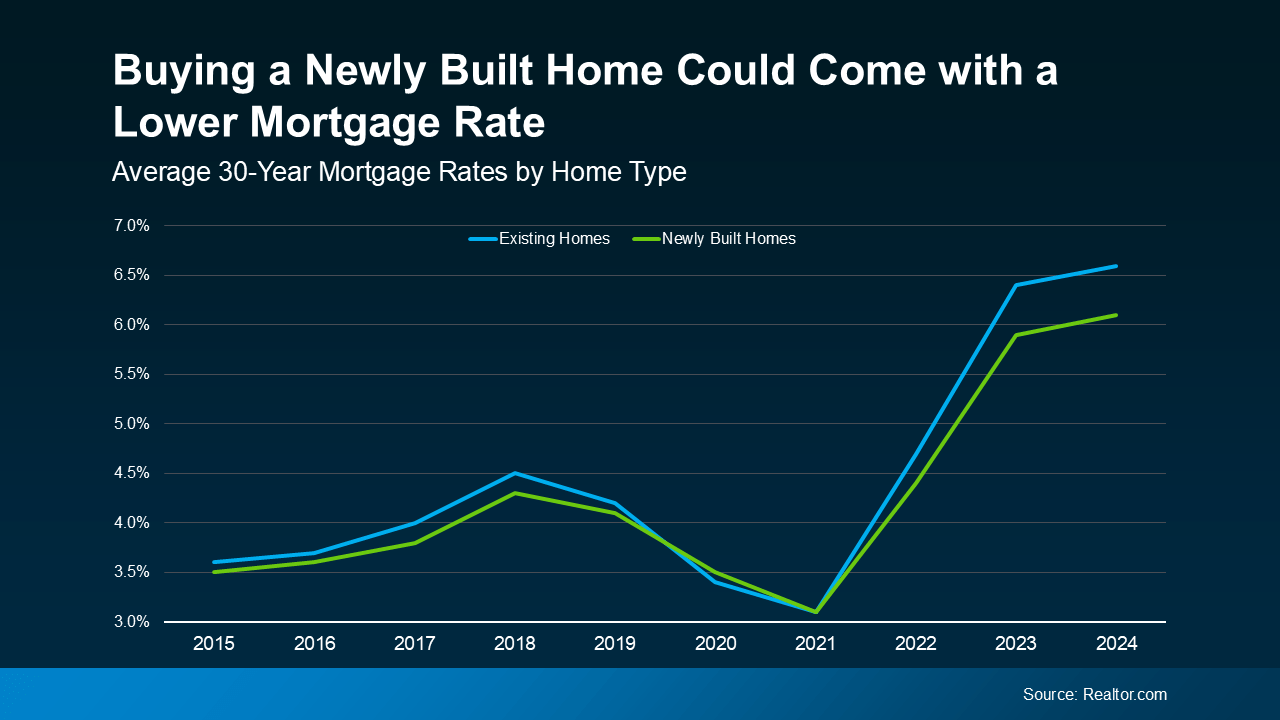

Builders Are Offering Lower Mortgage Rates

Here’s something most people don’t know. Right now, buyers of brand-new homes often get better mortgage rates than buyers of existing homes.

That’s because many builders are also offering rate buydowns to make their homes more attractive and keep sales moving. Basically, they’re willing to chip in to lower your rate, so you’re more likely to buy one of their homes.

Data from Realtor.com shows, in 2023 and 2024, buyers of newly built homes got a mortgage rate around half a percent lower compared to those who bought existing homes (see graph below):

That kind of savings adds up and makes a big difference when you’re figuring out your monthly budget.

That kind of savings adds up and makes a big difference when you’re figuring out your monthly budget.

So, if you haven’t found something you love yet, it’s time to add newly built homes to your search. You may find that what you’ve been looking for is already out there, it’s just in a new home community.

More choices, the potential to negotiate on the price, and maybe even better mortgage rates make these options a bright spot in today’s housing market.

If you haven’t considered a newly built home yet, what’s holding you back?

Let’s talk about it and see if it’s worth checking out new builds in and around our area.

Read More About:

Why a Newly Built Home Might Be the Move Right Now

The sun may be setting on the era of hunting endlessly for a diamond-in-the-rough fixer-upper. In today’s housing market, the spotlight has shifted toward a rising contender: the newly built home. Beyond the glimmering paint and untouched appliances, these homes come bundled with opportunities that stretch beyond aesthetics. For many buyers, especially in competitive regions, new construction may be the key to unlocking affordability, interest savings, and the bliss of stress-free moving.

A Changing Landscape in the Housing Market

Market conditions are evolving rapidly. Inventory of existing homes is tight, sellers are hesitant to trade up their low mortgage rates, and price tags on resale properties continue to climb. Meanwhile, builders have quietly and aggressively entered the ring, flooding the market with brand-new homes available at competitive sales prices. In fact, recent data from the National Association of Realtors (NAR) and the Census Bureau reports that nearly one in five homes for sale today is a newly built home.

That’s no small statistic—it represents a powerful shift in the choices available to consumers navigating the choppy waters of today’s market.

More New Homes on the Market = More Housing Options

The spike in inventory has emboldened home builders to sweeten the deal. They’re not only listing brand-new homes, but also slashing prices, offering rate buydowns, and stacking up builder incentives to lure savvy buyers.

What does that mean for you? It means now is a prime time to buy a newly built home. With more new homes on the market, buyers are no longer forced into bidding wars or compromising on their must-haves. Instead, they can tour move-in-ready properties in stunning new home communities, negotiate with motivated builders, and tap into benefits typically reserved for institutional investors.

The Power of Builder Incentives

The National Association of Home Builders (NAHB) recently shared that nearly 40% of builders are cutting prices and offering financing help. That means lower sales prices are becoming the norm, not the exception.

But it doesn’t stop there. Builders are also reducing upfront costs, covering closing fees, or offering lavish interior upgrades—all strategies aimed at tipping the scale in your favor. With each concession, the barrier to homeownership erodes, bringing the dream closer for families, retirees, and first time home buyer loans in West Palm Beach clients alike.

For those looking for better home prices, this is an era of strategic opportunity.

Even Better Mortgage Rates from Builders

Here’s a little-known truth: many brand-new homes come with even better mortgage rates than their existing homes counterparts. Why? Because builders are eager to close deals fast. By partnering with local mortgage lenders in West Palm Beach or national firms, they can offer rate buydowns that shave crucial percentage points off your interest.

According to data from Realtor.com, in 2023 and 2024, buyers of new construction properties secured rates up to 0.5% lower than existing homes purchasers. That fractional difference translates into significant mortgage savings over the life of a loan—and a more manageable monthly budget.

For those crunching numbers with West Palm Beach mortgage calculators, the difference is more than academic. It’s thousands of dollars in interest savings.

The Smart Play: Affordability without Sacrificing Luxury

Affordability doesn’t mean settling. Quite the opposite. Today’s newly built homes are architectural symphonies of open layouts, energy-efficient features, smart-home integrations, and pristine finishes. They require fewer repairs, carry lower utility costs, and are built to today’s environmental and safety standards.

That’s why more families in Florida are skipping over existing homes and heading straight for Affordable West Palm Beach home loans and master-planned communities with pools, trails, and top-rated schools.

Add in local programs like mortgage preapproval in West Palm Beach, and the dream becomes distinctly attainable.

Lean On Your Agent—Because Timing Matters

Navigating the growing sea of housing options takes more than enthusiasm; it takes strategy. This is where a seasoned real estate agent earns their stripes. A great agent will not only identify the best builder incentives, but also help you negotiate price, timing, and contingencies to ensure your investment is sound.

Whether you’re targeting commercial mortgage broker in West Palm Beach properties or scoping out suburban sanctuaries, an agent who understands the nuances of new construction contracts and the priorities of home builders is your best ally.

When the Numbers Work, the Choice Is Clear

Let’s take an example. Suppose you’re house hunting with a fixed monthly budget of $2,500. An existing home might max out that threshold with a higher mortgage rate, older insulation, and the looming need for a new roof.

Now compare that to a newly built home, which comes with lower mortgage rate options, tighter insulation, and warranties that eliminate surprise expenses. Add in mortgage savings from rate buydowns, and the math quickly favors the new.

It’s the difference between scraping by and thriving.

West Palm Beach: A Market Ripe for New Builds

Few areas exemplify this shift better than West Palm Beach. The surge in brand-new homes available throughout the region has created a playground of potential for eager buyers.

Whether you’re eyeing first time home buyer loans in West Palm Beach or considering West Palm Beach refinancing options, the path to ownership is paved with new developments that offer value-packed solutions. Many of these are backed by experienced home builders working in tandem with West Palm Beach mortgage broker networks to deliver seamless, low-friction financing experiences.

These local mortgage lenders in West Palm Beach understand the unique pressures of the Florida market—from coastal insurance premiums to hurricane codes—and they’re equipped to guide you toward the best mortgage rates in West Palm Beach.

Embracing the Future of Homeownership

The tides of today’s housing market are shifting. As inventory of existing homes stagnates, builders are stepping into the gap with elegant, efficient, and affordable solutions. For those willing to embrace modernity, the rewards are manifold: upgraded living, interest savings, and peace of mind.

The truth is, the home of your dreams may not be hidden behind ivy-covered brick or hardwood floors with stories. It might be gleaming under the sun in a new home community, complete with all the bells and whistles—and none of the hidden repairs.

Final Thought: The Smart Move Is a Newly Built Home

If you’ve been grinding through a home search, watching your options dwindle, and losing sleep over rising home prices, this is your wake-up call. Buy a newly built home.

Lean on your agent. Use property loan advice in West Palm Beach. And explore West Palm Beach mortgage calculators to fully understand your options.

In this moment of transition, where market conditions align with fresh opportunity, stepping into a newly built home might not just be the smart move—it might be your best one.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Mortgage Rates Are Stabilizing – How That Helps Today’s Buyers

Mortgage Rates Are Stabilizing – How That Helps Today’s Buyers

Over the past few years, affordability has been the biggest challenge for homebuyers. Between rapidly rising home prices and higher mortgage rates, many have felt stuck between a rock and a hard place.

But, something pretty encouraging is happening. While affordability is still tight, mortgage rates have shown signs of stabilizing in recent months. And that may finally make it a bit easier to plan your move.

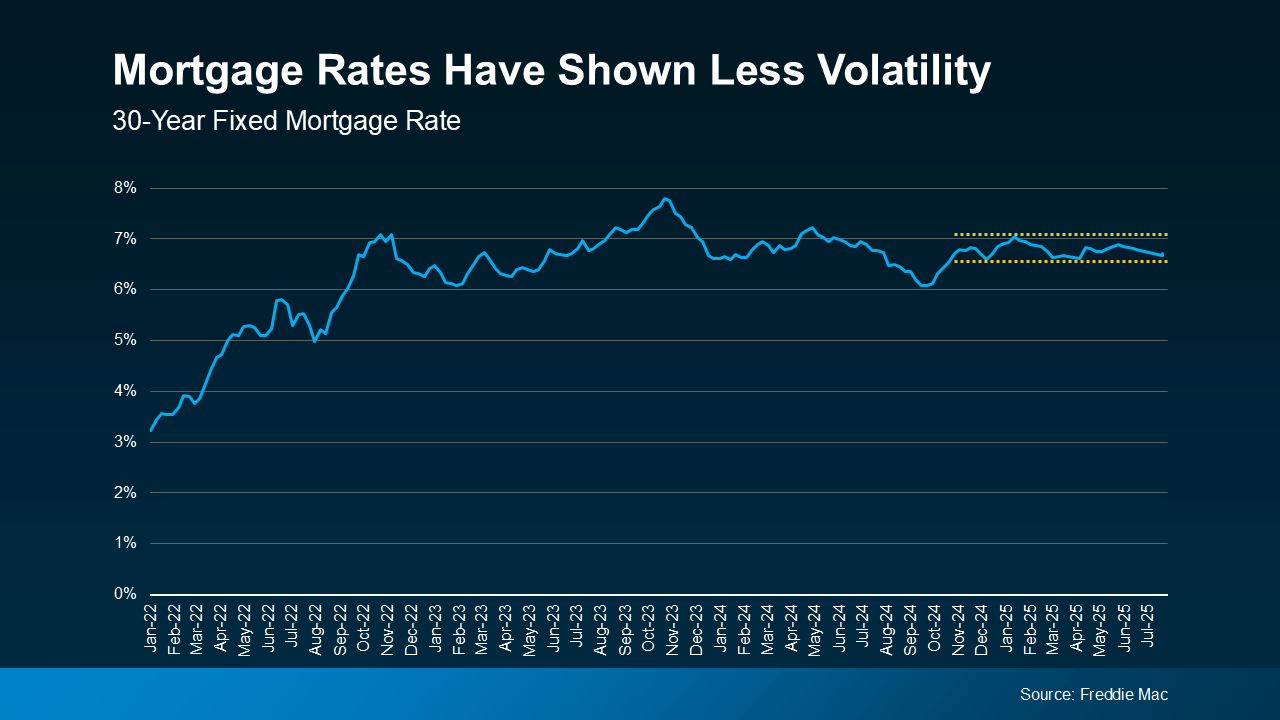

Mortgage Rates Have Stabilized – For Now

Over the past year, mortgage rates have had their share of ups and downs, making it tough for buyers to know what to expect. But recently, rates have started to level out and have settled into a more narrow range (see graph below):

As the graph shows, rates have stayed within that half-percentage-point since late last year. Yes, there’s been movement within that range, but wild swings and sudden ups and downs just haven’t been the story lately. And that’s a bigger deal than you may realize. As HousingWire explains:

As the graph shows, rates have stayed within that half-percentage-point since late last year. Yes, there’s been movement within that range, but wild swings and sudden ups and downs just haven’t been the story lately. And that’s a bigger deal than you may realize. As HousingWire explains:

“Analysts, economists and mortgage professionals are coining this quarter’s activity as one of the most “calm” periods for mortgage rates in recent memory.”

How This Helps Today’s Buyers

Let’s be real. Unpredictability makes it tough to plan ahead. When rates are bouncing around and making big jumps week to week, it’s easy to be intimidated. But with rates staying in a pretty steady range over the past several months, you have a clearer picture of what your potential monthly payment could look like. That makes moving feel less uncertain – and more doable.

So, stop waiting. And start planning. Even though rates may not be where you want them to be right now, they have been much less volatile for quite some time.

Will This Stability Last?

According to the experts, it looks like that stability might hang around for a bit. Rates may come down ever so slightly in the months ahead, but it’ll likely be a slow and mild change. As Danielle Hale, Chief Economist at Realtor.com, says:

“I expect a generally downward trend for rates this year, but at a slow enough pace that it might not be noticeable in any given month.”

So, if you’ve been holding out for the perfect mortgage rate, the best advice is to avoid trying to time the market. It may not look terribly different than the opportunity you already have in front of you. As Jeff Ostrowski, Housing Market Analyst at Bankrate, explains:

“Trying to time mortgage rates is really difficult. There’s no guarantee that rates are going to be any more favorable in three months or six months.”

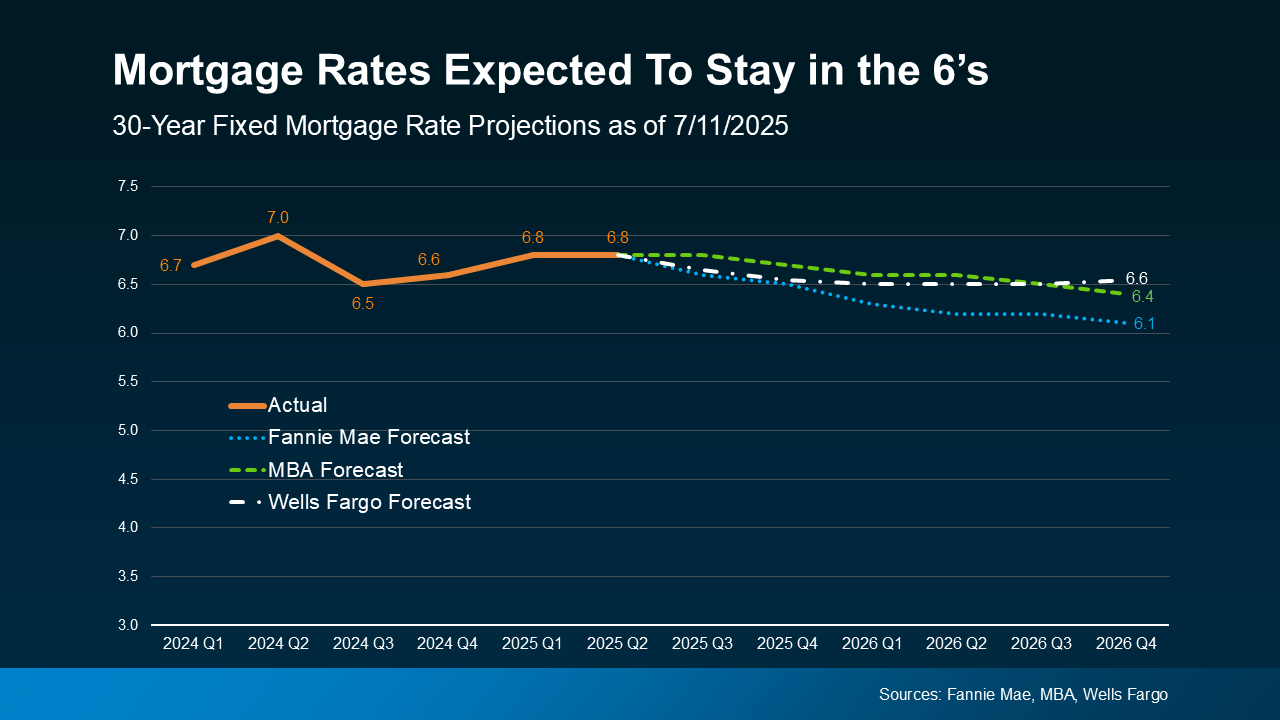

And if we look at the latest expert forecasts that go out a bit further, even those tell much of the same story. Two out of the three projections say rates will still likely be in the mid-6% range by the end of 2026 (see graph below):

This puts today’s buyers in a much better spot. As Sam Khater, Chief Economist at Freddie Mac, explains:

This puts today’s buyers in a much better spot. As Sam Khater, Chief Economist at Freddie Mac, explains:

“Mortgage rates have moved within a narrow range for the past few months . . . Rate stability, improving inventory and slower house price growth are an encouraging combination . . .”

Just remember, mortgage rates are still going to react to changing economic conditions, inflation, and more – and that means they could shift again. But right now, you’ve got more predictability, and that means more opportunity, too.

While affordability is still a challenge, the market may be offering a bit more stability – and that makes planning your next move a lot easier.

Let’s connect if you want to run the numbers and see what a monthly payment would look like in today’s market. That way you can stop waiting and start planning.

Read More About:

Mortgage Rates Are Stabilizing – How That Helps Today’s Buyers

The Winds Are Shifting: A New Era in Homebuying

For the last several years, the path to Buying A Home has felt like crossing a rickety bridge in a storm—high home prices, relentless interest rates, and a market teetering on unpredictability. But something’s changed. The gales have calmed, and the landscape, while not perfect, is more navigable.

Welcome to the calm period for mortgage rates.

It’s not just a breather—it’s a beacon. After months of economic unrest and price frenzy, Mortgage Rates Are Stabilizing, offering homebuyers a much-needed moment of clarity. And when you look beneath the surface, this pause could very well be the market opportunity smart buyers have been waiting for.

Why Mortgage Rate Stability Changes Everything

A year ago, watching rate fluctuations was like tracking a wildfire—unpredictable, fast-moving, and downright stressful. But now, we’re seeing Mortgage Rates settle into a narrow range, hovering with more consistency.

This newfound rate stability does something remarkable: it creates predictability in rates. And with that predictability comes power. Buyers can finally sit down, crunch numbers, and plan with a real sense of control.

Whether it’s calculating a monthly payment or analyzing mortgage forecasts, the game has changed. Less volatility. More strategy.

As noted by HousingWire, this isn’t just a short break from chaos—it’s one of the most composed chapters in mortgage rate history:

“Analysts, economists, and Mortgage Professionals are coining this quarter’s activity as one of the most calm periods for mortgage rates in recent memory.”

Let that sink in. This isn’t just relief—it’s renaissance.

How Buyers Benefit From Rate Stability

When interest rates were leaping like acrobats from week to week, real estate planning became an exercise in futility. Buyers were paralyzed by the fear of locking in a loan one day, only to see better numbers the next. That uncertainty killed momentum.

Now, with Stabilizing mortgage rates, the fog is lifting.

The steadiness of todays market gives buyers something critical: confidence. They’re no longer scrambling to “catch the dip” or worried about making a move in a hyper-volatile environment. The numbers may not be at historic lows, but they’re predictable—and that alone can swing the scales from hesitation to action.

Here’s what’s happening now:

-

Homebuyers are better able to estimate what their monthly payment will look like.

-

Lenders are providing more reliable quotes and timeframes.

-

Realtors and financial advisors can strategize effectively with clients.

-

And in places like Florida? The search for Affordable West Palm Beach home loans is getting a boost from lenders encouraged by rate steadiness.

Rebuilding Affordability in a Shifting Market

Yes, affordability is still a hurdle. But let’s look at the math.

Pairing Mortgage Rates that are no longer skyrocketing with signs of slower house price growth means that buyers are getting closer to a sustainable balance between income and housing costs.

Housing affordability is inching back into the conversation—and not just nationally. In hotspots like South Florida, the door is cracking open wider. With the help of a West Palm Beach mortgage broker, buyers are finding real options to make ownership attainable.

Tools like West Palm Beach mortgage calculators are turning dreams into digits. Buyers can now project costs with a level of accuracy not possible six months ago. That’s power. That’s progress.

Economic Conditions and the Bigger Picture

Let’s not ignore the elephant in the room: the macro landscape. Economic conditions remain in flux. Inflation has cooled slightly but still hovers above comfort levels. Wage growth is real but uneven. The Fed still watches from the wings.

Still, with all these variables, the latest expert forecasts point to continued stability—or even a slow rate change downward.

According to Realtor.com’s Chief Economist, Danielle Hale:

“I expect a generally downward trend for rates this year, but at a slow enough pace that it might not be noticeable in any given month.”

That’s not fireworks. That’s a gentle, almost imperceptible current—exactly the kind of subtle momentum that seasoned buyers capitalize on.

Stop Trying To Time the Market

The idea of waiting for the perfect mortgage rate? It’s time to shelve that strategy.

Jeff Ostrowski, Housing Market Analyst at Bankrate, cuts to the chase:

“Trying to time the market is really difficult. There’s no guarantee that rates are going to be any more favorable in three months or six months.”

He’s right. The smart money doesn’t wait for magic. It moves with intention in the window that exists now. And that window—while not a grand opening—is a clear one.

Inventory Is No Longer the Villain

Here’s another plot twist: Inventory is rising.

Yes, the ghost town that was the housing shelf in 2022 is slowly restocking. Improving inventory levels are giving buyers more options—and more leverage. This combination of better supply and stabilized rates means negotiations are getting less cutthroat.

This shift is especially pronounced in cities with aggressive growth and strong loan infrastructure. In South Florida, buyers have a wider selection and access to more favorable lending tools like:

-

First time home buyer loans in West Palm Beach

-

West Palm Beach refinancing options

-

Local mortgage lenders in West Palm Beach

-

Mortgage preapproval in West Palm Beach

-

Even niche offerings through a Commercial mortgage broker in West Palm Beach

The doors aren’t just open—they’re being held wide.

A Spotlight on West Palm Beach

Let’s zero in on one market that’s benefiting greatly from this stability: West Palm Beach.

A region once infamous for bidding wars and razor-thin margins is now seeing a renaissance in buyer confidence. With Best mortgage rates in West Palm Beach holding steady, aspiring homeowners are finally finding their footing.

For those considering making their move, having a trusted West Palm Beach mortgage broker by your side is invaluable. From navigating West Palm Beach mortgage calculators to securing Property loan advice in West Palm Beach, the resources available today outpace what was accessible during the chaos of previous years.

And let’s not forget the magic of preapproval. A fast-track mortgage preapproval in West Palm Beach could be your golden ticket in a climate where timing and preparation matter more than ever.

Where We Go From Here

It’s tempting to get comfortable with the word “stable.” But Mortgage Professionals know better: markets shift, tides turn, and tranquility isn’t forever.

Mortgage Rates are still sensitive to broader economic conditions—especially if inflation takes another unexpected turn. But for now, the outlook remains cautiously optimistic.

Freddie Mac’s Chief Economist, Sam Khater, underscores this sentiment:

“Mortgage rates have moved within a narrow range for the past few months… Rate stability, improving inventory, and slower house price growth are an encouraging combination.”

Translation? Opportunity is no longer hypothetical—it’s here.

What To Watch For

If you’re still on the fence, keep your eyes on these key indicators:

-

Inflation trends and how they influence Fed policy

-

Changes in wage growth vs. home prices

-

Ongoing updates from expert projections and financial institutions

-

Local trends—especially in West Palm Beach, where lenders are uniquely positioned to offer regionalized insights

As Mortgage forecasts evolve, staying informed and working with localized experts—especially Local mortgage lenders in West Palm Beach—can give you an edge.

Making Your Move in Today’s Market

Whether you’re a first-time buyer, an investor, or just someone looking to put down roots, todays market offers clarity we haven’t seen in years.

And clarity is currency.

Let go of outdated expectations about 2% rates or once-in-a-lifetime deals. Instead, embrace the current climate for what it is: a season of strategy. Use tools. Ask questions. Leverage insights. Lean on pros like a Commercial mortgage broker in West Palm Beach if your plans include multi-unit or investment properties.

This isn’t about waiting for perfection. It’s about acting during the calm period for mortgage rates, when the waters are smooth enough to chart a real course forward.

Final Thought

Affordability is still a battle—but we’re no longer fighting blind.

With Stabilizing mortgage rates, more inventory, and actionable insights from the latest expert forecasts, this is no longer the treacherous terrain of last year. It’s a path with guardrails. A road with direction.

And in places like West Palm Beach, the combination of Affordable West Palm Beach home loans, smarter tools, and seasoned Mortgage Professionals means you’re not going it alone.

The time to move isn’t someday. It’s now.

And this time? The bridge looks a lot sturdier.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Why More Sellers Are Choosing To Move, Even with Today’s Rates

Why More Sellers Are Choosing To Move, Even with Today’s Rates

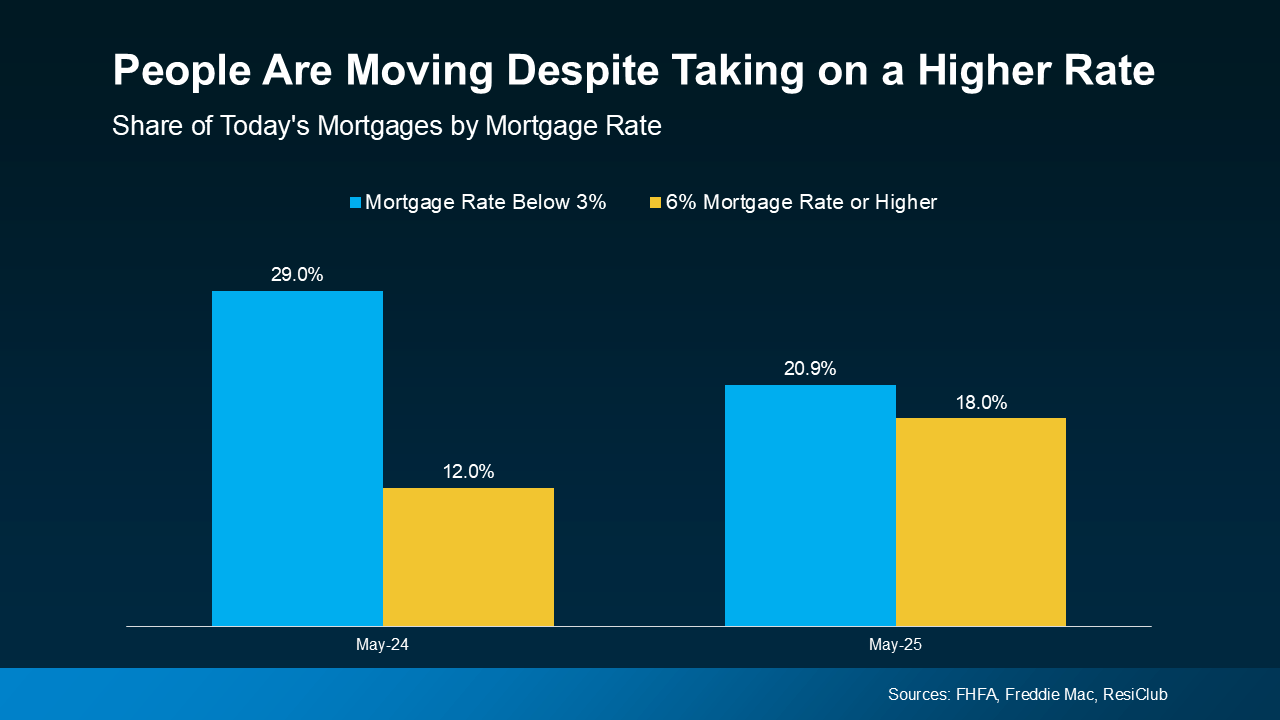

It’s hard to let go of a 3% mortgage rate. There’s no question about it. It’s the main reason why so many homeowners have delayed their move in recent years. But here’s something to consider.

While your low rate might be ideal, it doesn’t make up being too cramped, having a staircase your knees can’t handle anymore, or being 1,000 miles from your family. And those real-life needs are pushing more sellers off the fence despite today’s rates.

Data shows the share of homeowners with a mortgage rate below 3% is dropping as more people move. And, as a result, the share of homeowners taking on a mortgage rate above 6% is rising, too (see graph below):

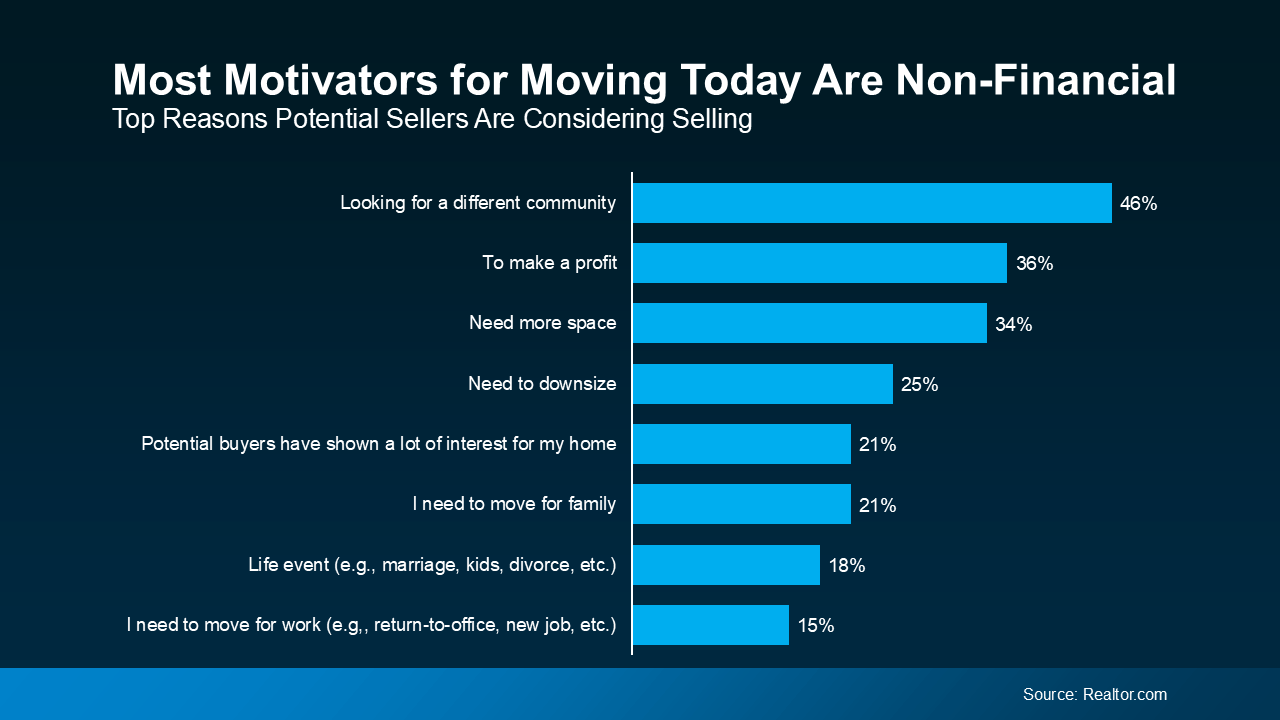

The Biggest Reasons People Are Moving Right Now

Why are some homeowners willing to take on a higher rate? A survey from Realtor.com helps shed light on that. It shows 79% of homeowners considering selling today are doing it out of necessity. And that same survey says most of the necessary reasons people are moving are non-financial in nature (see graph below):

Do any of these reasons resonate for you, too?

Do any of these reasons resonate for you, too?

- You Need More Space: Whether it’s a new baby, children needing their own rooms, or having your parents move in so it’s easier to take care of them, outgrowing your space can happen fast.

- You Need Less Space: The kids are out of the house now and you’re craving a life that’s a little simpler. Downsizing can be a major relief: fewer rooms to clean, less to maintain, and lower utility bills, too.

- You Want to Be Closer to Family: Whether it’s to help with grandchildren or care for aging parents, sometimes the pull of being near loved ones outweighs the math.

- A Relationship in Your Life Has Changed: Divorce, separation, or moving in together after a marriage or new partnership – all can create the need for a fresh start and a new place to call home.

- Your Job Is Taking You Somewhere New: If you finally landed your dream job or your partner’s company is relocating, you may need to move too.

What About Mortgage Rates?

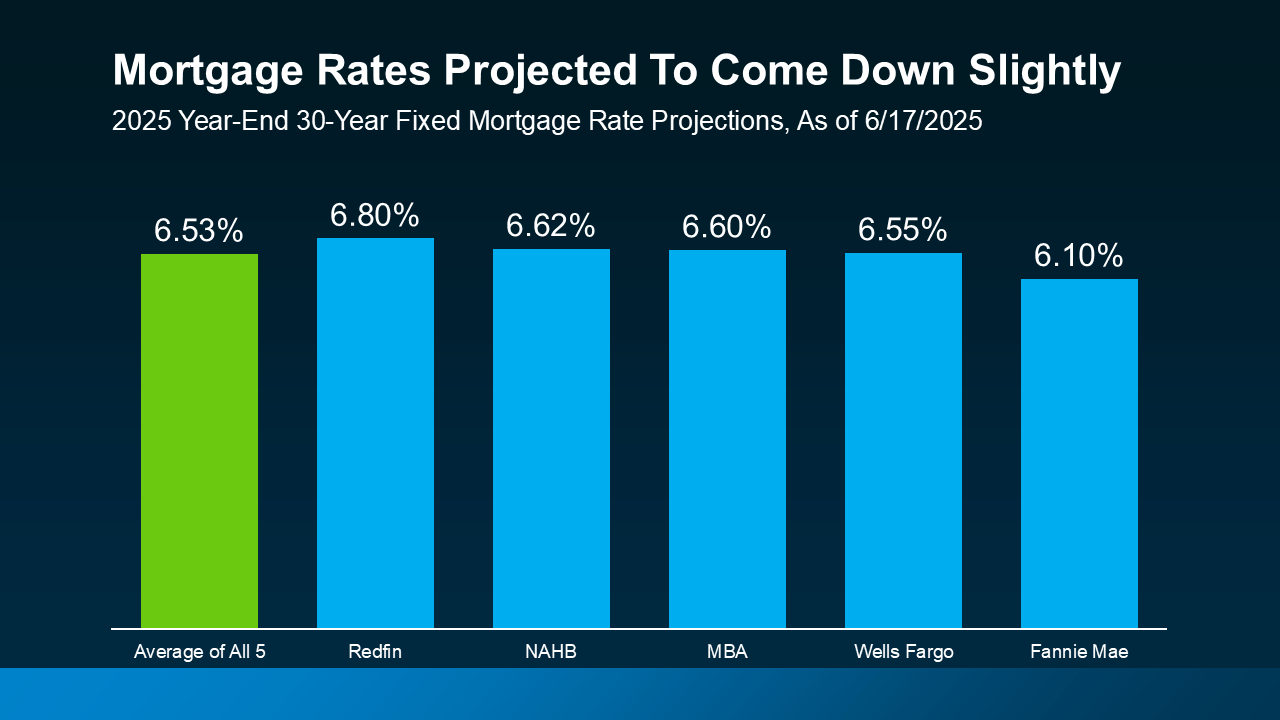

Yes, experts expect mortgage rates to ease, but slowly. The latest projections show only modest declines this year – not the 3% you may be hoping for (see graph below):

So, while waiting for a big drop in rates might sound strategic, it could just mean more time feeling stuck in a space that no longer fits. And for many, that waiting game has already gone on long enough.

So, while waiting for a big drop in rates might sound strategic, it could just mean more time feeling stuck in a space that no longer fits. And for many, that waiting game has already gone on long enough.