What Credit Score Do You Really Need To Buy a Home?

According to Fannie Mae, 90% of buyers don’t actually know what credit score lenders are looking for, or they overestimate the minimum needed.

Let that sink in. That means most homebuyers think they need better credit than they actually do – and maybe you’re one of them. And that could make you think buying a home is out of reach for you right now, even if that’s not necessarily true. So, let’s look at what the data really says about credit scores and homebuying.

There’s No One Magic Number

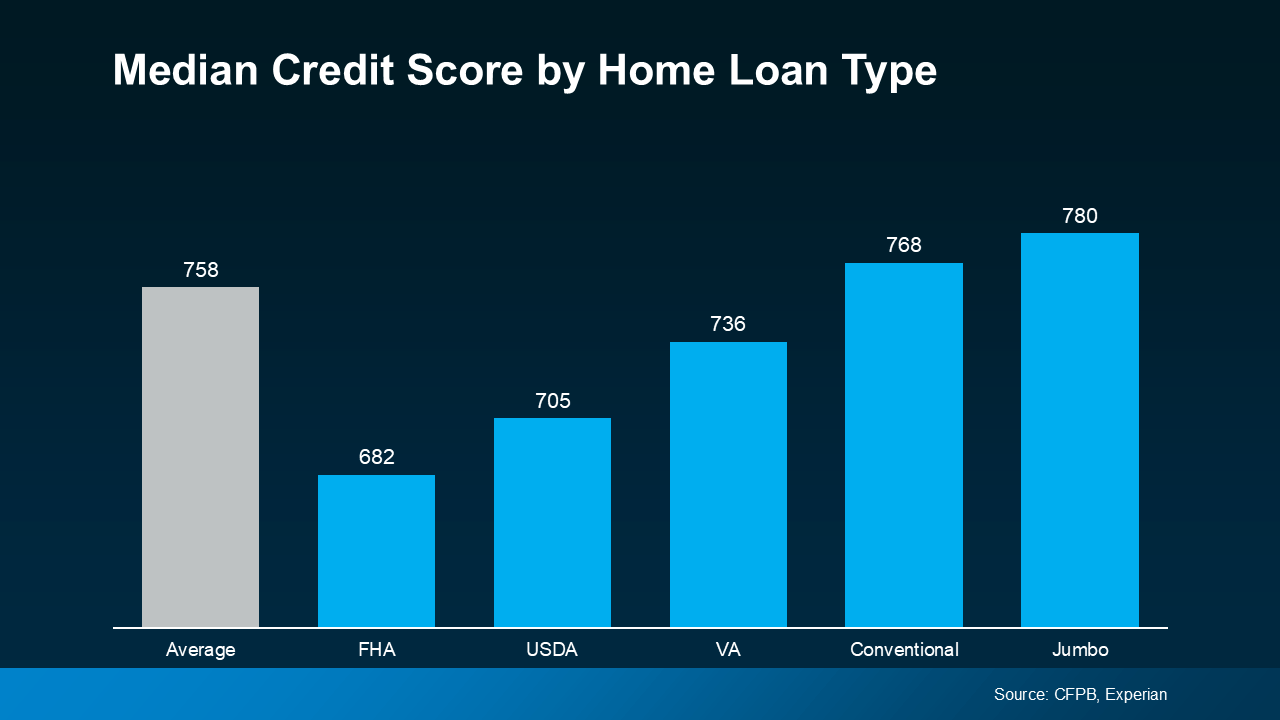

There’s no universal credit score you absolutely have to have when buying a home. And that means there’s more flexibility than most people realize. Check out this graph showing the median credit scores recent buyers had among different home loan types:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

Why Your Score Still Matters

When you buy a home, lenders use your credit score to get a sense of how reliable you are with money. They want to see if you typically make payments on time, pay back debts, and more.

Your score can impact which loan types you may qualify for, the terms on those loans, and even your mortgage rate. And since mortgage rates are a big factor in how much house you’ll be able to afford, that may make your score feel even more important today. As Bankrate says:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That still doesn’t mean your credit has to be perfect. Even if your credit score isn’t as high as you’d like, you may still be able to get a home loan.

Want To Boost Your Score? Start Here

And if you talk to a lender and decide you want to improve your score (and hopefully your loan type and terms too), here are a few smart moves according to the Federal Reserve Board:

- Pay Your Bills on Time: This is a big one. Lenders want to see you can reliably pay your bills on time. This includes everything from credit cards to utilities and cell phone bills. Consistent, on-time payments show you’re a responsible borrower.

- Pay Down Your Debt: When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible. That makes you a lower-risk borrower in the eyes of lenders – making them more likely to approve a loan with better terms.

- Review Your Credit Report: Get copies of your credit report and work to correct any errors you find. This can help improve your score.

- Don’t Open New Accounts: While it might be tempting to open more credit cards to build your score, it’s best to hold off. Too many new credit applications can lead to hard inquiries on your report, which can temporarily lower your score.

Your credit score doesn’t have to be perfect to qualify for a home loan. But a better score can help you get better terms on your home loan. The best way to know where you stand and your options for a mortgage is to connect with a trusted lender.

Read More About:

What Credit Score Do You Really Need To Buy a Home?

Introduction: Peering Behind the Numbers

In the labyrinth of homebuying, where emotions, finances, and timing converge, one gatekeeper quietly dictates the journey — your credit score. Whispered about in bank offices and fretted over during late-night online calculator sessions, the credit score has become a mythic number. It inspires dread in some and overconfidence in others. But here’s the pivotal question: What credit score do you really need to buy a home?

Spoiler: The answer is more liberating than most people imagine. While many envision an Everest-level number to clear, the reality — according to institutions like Fannie Mae and the Federal Reserve Board — is far more nuanced.

Let’s untangle the misconceptions, understand your options for a mortgage, and uncover how to get a home loan with confidence — especially if you’re exploring Affordable West Palm Beach home loans or looking for the best mortgage rates in West Palm Beach.

Chapter 1: A Misunderstood Barrier to Entry

A surprising 90% of homebuyers, according to a study by Fannie Mae, either underestimate or overestimate the credit score required to qualify for a home loan. That uncertainty has stopped countless would-be buyers from even trying to apply for a mortgage.

Many think they need a nearly perfect FICO Score to get their foot in the door. The truth? You don’t.

The Power of Perception vs. Reality

There’s no singular number etched in stone that every lender worships. The minimum credit score required depends on several variables: your loan type, the lender’s underwriting criteria, and your overall financial profile — including your available credit amount and repayment history.

This revelation changes the game. Suddenly, buying a home isn’t a far-off fantasy. It becomes an attainable milestone.

Chapter 2: The Myth of the Magic Number

Let’s obliterate the notion that there’s one omnipotent score you must achieve. A look at median credit scores across different home loan types unveils a rich tapestry of diversity. FHA loans, for instance, often accept scores as low as 580, while conventional loans may require something closer to 620–640.

Median Scores Across Home Loan Types

Different loans, different scorebands. Here’s the breakdown of common home loan types:

-

FHA Loans: Accept scores as low as 580

-

VA Loans: Often flexible with lower scores, particularly for veterans

-

Conventional Loans: Generally require scores of 620 and up

-

Jumbo Loans: Tend to demand higher scores — often 700 or more

And in West Palm Beach, with its eclectic mix of luxury condos, starter homes, and waterfront estates, there’s no shortage of lending options, from first-time home buyer loans in West Palm Beach to commercial mortgage brokers in West Palm Beach. There’s truly a fit for every scenario.

Chapter 3: Why Your Credit Score Still Holds Power

Let’s not get too relaxed, though. Just because a sky-high credit score isn’t mandatory doesn’t mean it isn’t influential. In the mortgage world, your credit score is a compass. It determines the terms on your home loan, your mortgage rate, and sometimes whether you’ll even be able to qualify for the loan.

The Domino Effect

A stronger score can unlock better conditions — like a lower interest rate, reduced private mortgage insurance (PMI), or a more flexible down payment requirement. A lower score, on the other hand, may trigger higher monthly payments or more stringent terms.

Bankrate explains it best:

“Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

This is why boosting your credit score is a priority if you’re aiming for the best mortgage rates in West Palm Beach or seeking West Palm Beach refinancing options.

Chapter 4: The Lender’s Lens

Let’s get into the psyche of lenders. When they examine your credit report, they’re not just evaluating numbers — they’re assessing risk, reliability, and responsibility.

They’re asking:

-

Do you pay your bills on time?

-

How much of your available credit amount are you using?

-

Are there derogatory marks or collection accounts?

-

Have you had multiple credit applications in a short timeframe?

In essence, they want to see a responsible borrower with a stable financial history.

If you appear as a lower-risk borrower, your odds of mortgage approval skyrocket — even more so when working with local mortgage lenders in West Palm Beach who understand the nuances of the area market.

Chapter 5: Tactical Ways to Boost Your Credit Score

So how can you become that dream client lenders love?

1. Pay Your Bills on Time

It sounds obvious, but timeliness is paramount. Even one late payment can knock points off your score. On-time payments signal maturity and stability.

2. Pay Down Your Debt

If you’re consistently utilizing a high percentage of your available credit amount, you may look financially stressed. Aim to keep usage below 30% — ideally under 10% — to signal strong management.

3. Review Your Credit Report

Errors happen. Misreported delinquencies or incorrect balances can drag your score down. Pull your credit report from all three bureaus and scrutinize every detail. Dispute inaccuracies immediately.

4. Don’t Open New Accounts Unnecessarily

Opening several lines of credit in a short time leads to multiple hard inquiries — a red flag to lenders. Unless strategically advised, avoid opening fresh accounts during the mortgage preapproval in West Palm Beach phase.

Chapter 6: Customizing the Mortgage for You

Now that the credit foundation is laid, let’s zoom out to the bigger picture — choosing a mortgage that fits like a glove.

Exploring Your Options for a Mortgage

-

Are you eligible for FHA or VA loans?

-

Will you benefit from first-time home buyer loans in West Palm Beach?

-

Do you need a jumbo loan for a luxury property?

-

Interested in West Palm Beach mortgage calculators to estimate costs?

-

Need tailored property loan advice in West Palm Beach?

The beauty of the modern mortgage market is personalization. No longer does one mold fit all.

A West Palm Beach mortgage broker can be your concierge, guiding you through loan types, helping you qualify for a mortgage, and ensuring you’re not leaving money on the table.

Chapter 7: Getting Preapproved — The Power Move

Before house-hunting in earnest, it’s wise to talk to a lender and get mortgage preapproval in West Palm Beach. Preapproval shows sellers you’re serious, gives you a concrete budget, and lets you move quickly when your dream home surfaces.

The lender will look at:

-

Your credit scores

-

Your loan type

-

Your debt-to-income ratio

-

Income stability

-

Assets and reserves

Think of it as your financial passport. And the stamp of approval opens the gates to buy a home.

Chapter 8: The Local Advantage — Why West Palm Beach Shines

In the sun-soaked, palm-lined avenues of West Palm Beach, opportunities abound. Whether you’re exploring affordable West Palm Beach home loans for a quaint bungalow or diving into commercial mortgage broker in West Palm Beach options for a mixed-use building, the landscape is rich and rewarding.

West Palm Beach’s real estate market favors the prepared and the proactive. With demand high and inventory evolving, aligning your credit score and mortgage approval early means you’ll stand tall when opportunity knocks.

Local lenders bring added value — insight into neighborhood trends, city tax structures, and competitive mortgage conditions — giving you a sharp edge.

Chapter 9: Beyond the Score — A Holistic View

Let’s step back and remember: credit scores are pivotal, but they’re one thread in a broader financial tapestry.

Lenders will also examine:

-

Employment history

-

Monthly liabilities

-

Savings for down payment and closing costs

-

Gifted funds

-

Co-borrowers and guarantors

Even with a mid-range score, strong performance in these other categories can help you qualify for the loan or negotiate better loan terms.

Chapter 10: Empowerment Through Education

Fear and misinformation keep many qualified buyers on the sidelines. But knowledge — real, up-to-date, practical knowledge — is your leverage.

By understanding how credit scores intersect with lending, by optimizing your profile, and by choosing the right partners like a trusted lender, you rewrite your narrative from “maybe someday” to “why not now?”

A higher credit score is a powerful ally, but not an immovable barrier. With deliberate action, strategic planning, and expert guidance, you can move from dreaming to buying a home — and enjoying the radiant sunsets from your West Palm Beach patio.

Conclusion: You’re Closer Than You Think

A home isn’t just a structure; it’s security, freedom, and legacy. And you’re closer to that reality than you might believe. Your credit score matters, yes — but it’s not a glass ceiling. It’s a stepping stone.

So whether you’re nurturing your credit, seeking affordable West Palm Beach home loans, or consulting with a West Palm Beach mortgage broker for personalized advice, now is the time to take bold steps forward.

Connect with a trusted lender. Talk to a trusted lender. Understand your options for a mortgage. Refuse to let assumptions dictate your financial destiny.

The keys to your future home may be just a few smart moves away.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Get Pre-Approved Today