Think It’s Better To Wait for a Recession Before You Move? Think Again.

Fear of a recession is back in the headlines. And if you’re thinking about buying or selling sometime soon, that may leave you wondering if you should reconsider the timing of your move.

A recent survey by John Burns Research and Consulting (JBREC) and Keeping Current Matters (KCM) shows 68% of people are delaying plans to buy or sell due to economic uncertainty.

But it may not be for the reason you think. Not everyone is holding off because they’re worried. Some buyers are waiting because they’re hopeful. According to Realtor.com:

“In 2025Q1, 3 in 10 (29.8% of) surveyed homebuyers said a recession would make them at least somewhat more likely to purchase a home . . . This reflects a common dynamic where some buyers see a downturn as an opportunity. If the economy enters a recession, the Federal Reserve may respond by lowering interest rates to stimulate activity, potentially putting downward pressure on mortgage rates and easing affordability concerns. As a result, buyers—especially those with limited down payments—might view a recession as a more favorable time to enter the market.”

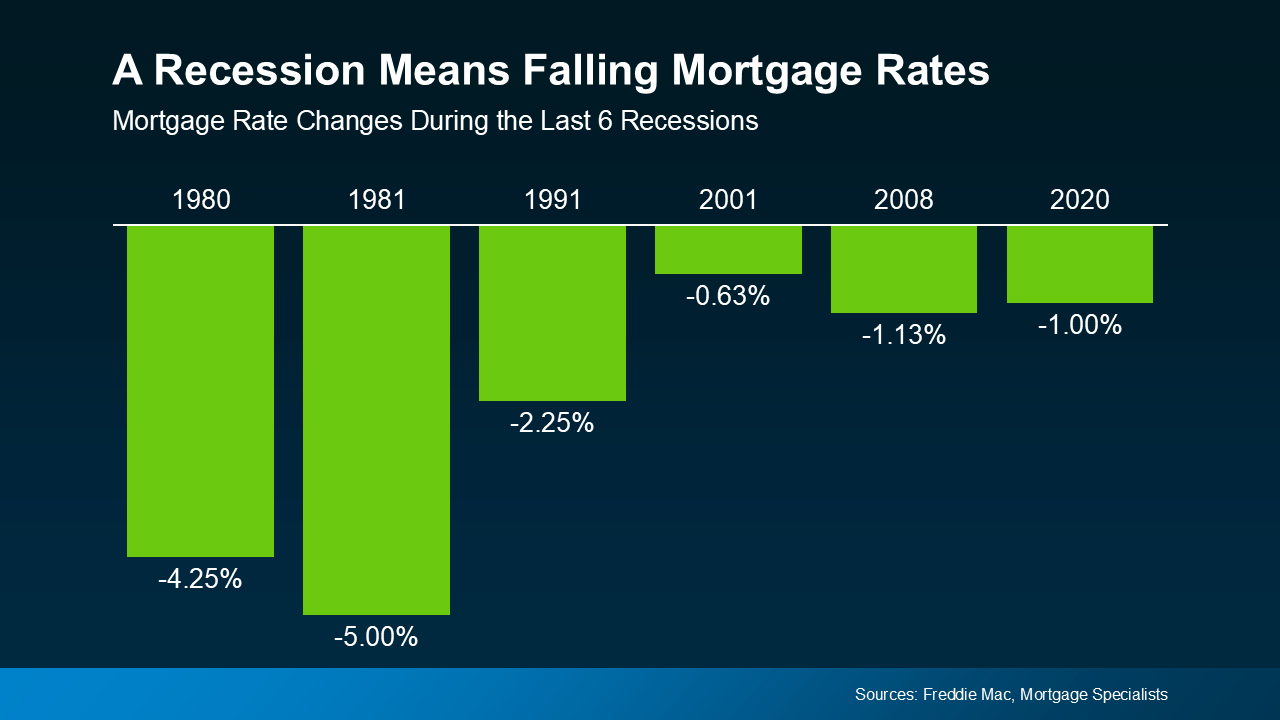

And there’s some truth to the idea that a recession could bring about lower mortgage rates. History shows mortgage rates usually drop during economic slowdowns. That’s not guaranteed – but it is a common pattern. Looking at data from the last six recessions, you can see mortgage rates fell each time (see graph below):

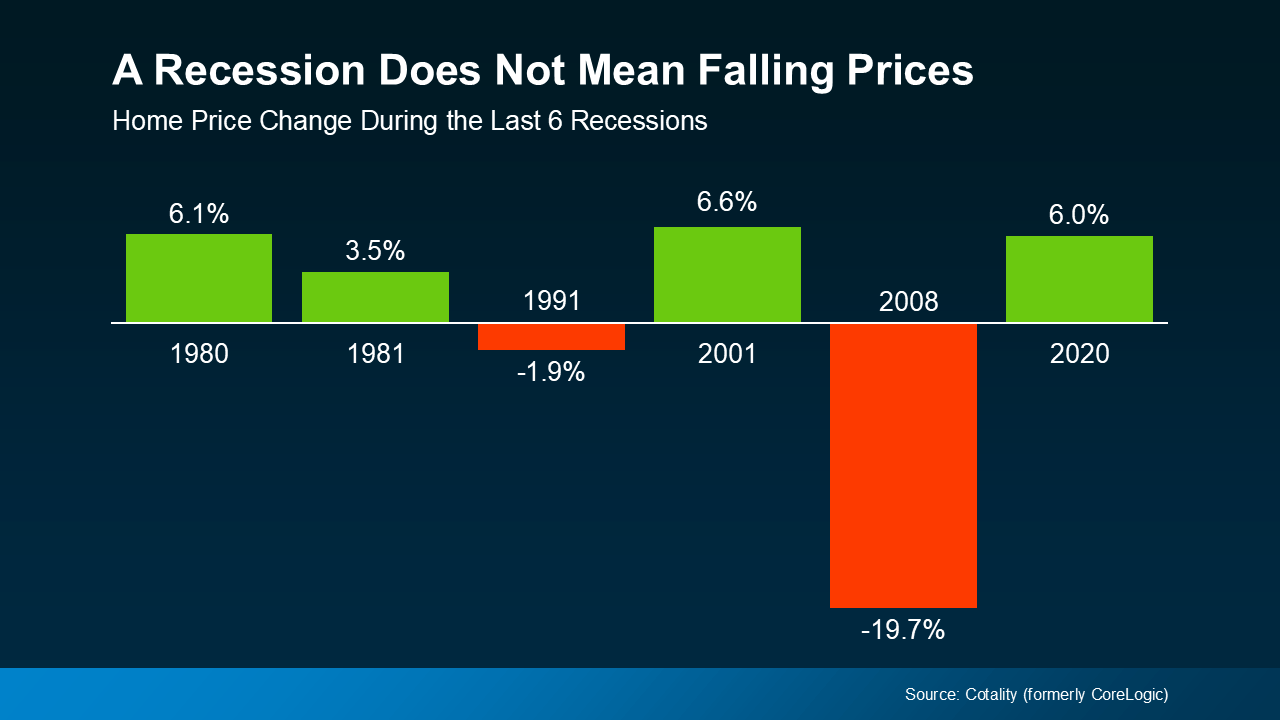

But here’s what those buyers may not be considering. Many of those hopeful buyers are assuming something else will happen too – that home prices will drop. And that’s where history tells a different story.

But here’s what those buyers may not be considering. Many of those hopeful buyers are assuming something else will happen too – that home prices will drop. And that’s where history tells a different story.

According to data from Cotality (formerly CoreLogic), home prices went up in four of the last six recessions (see graph below)

So, while many people think that if a recession hits, home prices will fall like they did in 2008, that was an exception, not the rule. It was the only time the market saw such a steep drop in prices. And it hasn’t happened since, mainly because there’s still a long-standing inventory deficit, even as the number of homes on the market is rising.

So, while many people think that if a recession hits, home prices will fall like they did in 2008, that was an exception, not the rule. It was the only time the market saw such a steep drop in prices. And it hasn’t happened since, mainly because there’s still a long-standing inventory deficit, even as the number of homes on the market is rising.

Since prices tend to stay on whatever path they’re already on, know this: prices are still holding steady or rising in most metros, although at a much slower pace. So, a big drop isn’t likely. As Robert Frick, Corporate Economist with Navy Federal Credit Union, explains:

“Hopes that an economic slowdown will depress housing prices are wishful thinking at this point . . .”

If you’ve been waiting for a recession to make your move, it’s important to understand what really happens during one – and what likely won’t. Lower mortgage rates could be on the table. But lower home prices? That’s far less likely.

Don’t wait for a market that may never come. If you’re thinking about buying or selling, let’s connect to talk through what today’s economy really means for you – and make a smart plan that works in your favor, regardless of what the headlines say.

Think It’s Better To Wait for a Recession Before You Move? Think Again.

The whispers of a Recession are growing louder again. From Wall Street to Main Street, uncertainty is hovering in the air like a summer thundercloud. And for anyone thinking about buying or selling, the temptation to wait it out may feel safer than diving into what appears to be turbulent waters.

But here’s the twist: what if the perceived storm is really just fog—and pushing through now is actually your smart move strategy?

Let’s untangle the myths, decipher the signals, and expose why waiting for a Recession to make a move could be the costliest delay in your real estate journey.

The Allure of Waiting: Fear or Hope?

Recent surveys paint a vivid picture. According to John Burns Research and Consulting (JBREC) and Keeping Current Matters (KCM), a staggering 68% of Americans have plans to buy or sell but are choosing to delay due to economic uncertainty. That’s not a small number—that’s a movement.

And it’s not just fear of another 2008 Housing Crisis that’s driving hesitation. Many believe a Recession could unlock better opportunities—particularly if mortgage rates and home prices tumble.

One-third of potential homebuyers told Realtor.com that a Recession would make them more likely to purchase a home. Why? Because historically, the Federal Reserve often lowers interest rates during downturns to stimulate the economy. That drop, in theory, could ease home affordability and reduce the cost of down payments.

It’s easy to understand the optimism. Who wouldn’t want to swoop in when the market dips and ride the rebound to equity heaven?

The Mortgage Mirage: Will Rates Really Fall?

If history is our guidebook, then yes—mortgage rates have often dipped during previous economic slowdowns. Looking at historical trends, the last six recessions each coincided with a fall in interest rates.

That’s not coincidence. It’s part of the Fed’s usual toolkit to prevent economic contraction. But today’s economic landscape isn’t quite textbook. Inflation is still a gnawing concern, labor markets remain resilient, and the Fed’s current posture is cautious. Any reduction in rates will be a surgical strike—not a sweeping slashing.

Even if West Palm Beach mortgage brokers start advertising the best mortgage rates in West Palm Beach, there’s no guarantee the drop will be substantial or sustained.

The Price Myth: Will Home Prices Plunge?

Here’s where many get it wrong.

The idea that home prices will drop in a recession is rooted in what happened during the 2008 Housing Crisis. But that was an anomaly—not the norm. According to data from Cotality (formerly CoreLogic), home prices actually rose in four out of the last six recessions.

Why? Because the housing market doesn’t follow the stock market’s erratic swings. It’s grounded in supply and demand. And right now? Supply is the missing ingredient.

Despite rising inventory levels, there remains a stubborn inventory deficit nationwide. The number of homes on the market simply isn’t enough to create a buyer’s paradise.

So even if the economy hits pause, home prices are likely to continue their steady—albeit slower—climb. As Navy Federal Credit Union economist Robert Frick put it, “Hopes that an economic slowdown will depress housing prices are wishful thinking at this point.”

The Demand Equation: What About Buyers?

Here’s where it gets really interesting.

Homebuyer sentiment is surprisingly strong. Millennials are entering peak buying years. Gen Z is already knocking on the door. And many Boomers are selling a home to downsize or relocate.

Even with higher mortgage rates, many are still intent on buying a home—they’re just being more strategic about it. And in hot locations like Florida, especially the booming Gold Coast, demand isn’t disappearing—it’s just shifting.

If you’re looking for Affordable West Palm Beach home loans, the local market remains robust. Whether it’s first-time home buyer loans in West Palm Beach or savvy West Palm Beach refinancing options, there’s activity brewing behind the headlines.

Market Timing: A Risky Game

Let’s address the elephant in the room—market timing.

Trying to time your real estate move with economic cycles is like waiting for the perfect moment to jump into double Dutch jump rope. You’ll wait, second-guess, hesitate—and likely miss your chance altogether.

By the time the real estate market shows clear signs of “bottoming out,” prices may have already rebounded and competition could be fierce. The best deals? They go to those who act while others hesitate.

And remember, the perfect moment often isn’t seen in the moment. It’s only recognized in hindsight.

The Real Cost of Waiting

Let’s run the numbers.

Imagine mortgage rates fall by 0.5% during a Recession. That’s good, right? But if home prices rise another 5-8% in that same period, your lower rate is offset by a higher purchase price. You may end up paying more over time—not less.

Then factor in lost opportunity costs—rising rents, missed equity gains, and inflation eating away at your savings.

Now contrast that with making a move today. You secure a fixed rate. You build equity as the market continues its upward march. You establish roots while others remain stuck in analysis paralysis.

And if you’re looking to crunch numbers in real time, West Palm Beach mortgage calculators offer localized insights that help you plan proactively, not reactively.

The West Palm Beach Factor: A Case Study in Action

Let’s zoom in on one of Florida’s real estate gems—West Palm Beach.

It’s not just the palm trees and sunshine that are heating up this market. It’s the lifestyle, the tax benefits, the robust job scene, and yes—the flood of demand.

Local mortgage lenders in West Palm Beach are seeing steady application volume. Property loan advice in West Palm Beach is in high demand. And the market remains competitive, not chaotic.

For buyers, this means preparing. Get your mortgage preapproval in West Palm Beach sorted early. Whether you’re eyeing a condo downtown or a quiet single-family in the suburbs, knowing your numbers gives you leverage.

For investors, commercial opportunities are rising too. A trusted commercial mortgage broker in West Palm Beach can help you navigate the unique dynamics of mixed-use developments and rental portfolios.

Your Next Move: Confidence, Not Caution

This isn’t about being reckless. It’s about being ready.

The headlines may suggest a wait-and-see approach. But history, data, and local dynamics all whisper a different message: Don’t delay. Prepare. Act with precision.

And if you’re thinking about buying or selling, now is not the time to sit on the sidelines. With the right lender, the right agent, and the right mindset, your next move could be your smartest yet.

Even in an uncertain economy, clarity comes to those who act with intention.

Final Thoughts: Rewriting the Narrative

Forget the myth that a Recession is your golden ticket to low prices and easy deals. That ship sailed in 2008—and even then, it was a shipwreck for many.

The 2008 Housing Crisis was the result of systemic failure, not a typical downturn. Today’s real estate market is fortified by equity-rich homeowners, stricter lending standards, and deep-seated demand.

So if your instincts are telling you to wait, challenge them. Use tools like West Palm Beach mortgage calculators, seek property loan advice in West Palm Beach, and get that mortgage preapproval in West Palm Beach locked down.

The market may shift. The economy may wobble. But opportunity? That’s reserved for those who lean in while others lean back.

Ready When You Are

Whether you’re gearing up to buy a home, sell a home, or simply explore your options, don’t let the shadow of a potential recession dim your vision.

Consult with your West Palm Beach mortgage broker, explore the best mortgage rates in West Palm Beach, or tap into first-time home buyer loans in West Palm Beach tailored to your unique situation.

Make the move that future you will thank you for.

The opportunity isn’t in waiting—it’s in waking up to what’s possible today.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice