3 Reasons Affordability Is Showing Signs of Improvement This Fall

Meta Title: Why Home Affordability Is Finally Improving This Fall: Rates, Prices & Wages Explained

Meta Description: Learn how falling mortgage rates, moderating home prices, and rising wages are making home affordability better this fall. Discover what it means for buyers and whether now is the right time to purchase.

Introduction: Why Homebuyers Are Getting a Break This Fall

For the past two years, many homebuyers have faced an uphill battle. Mortgage rates surged to highs not seen in two decades, home prices soared during the pandemic boom, and incomes couldn’t keep pace. For many would-be buyers, the math simply didn’t work.

Maybe you were one of them — browsing listings, running mortgage calculators, and then closing the laptop in frustration because the monthly payments were just too steep.

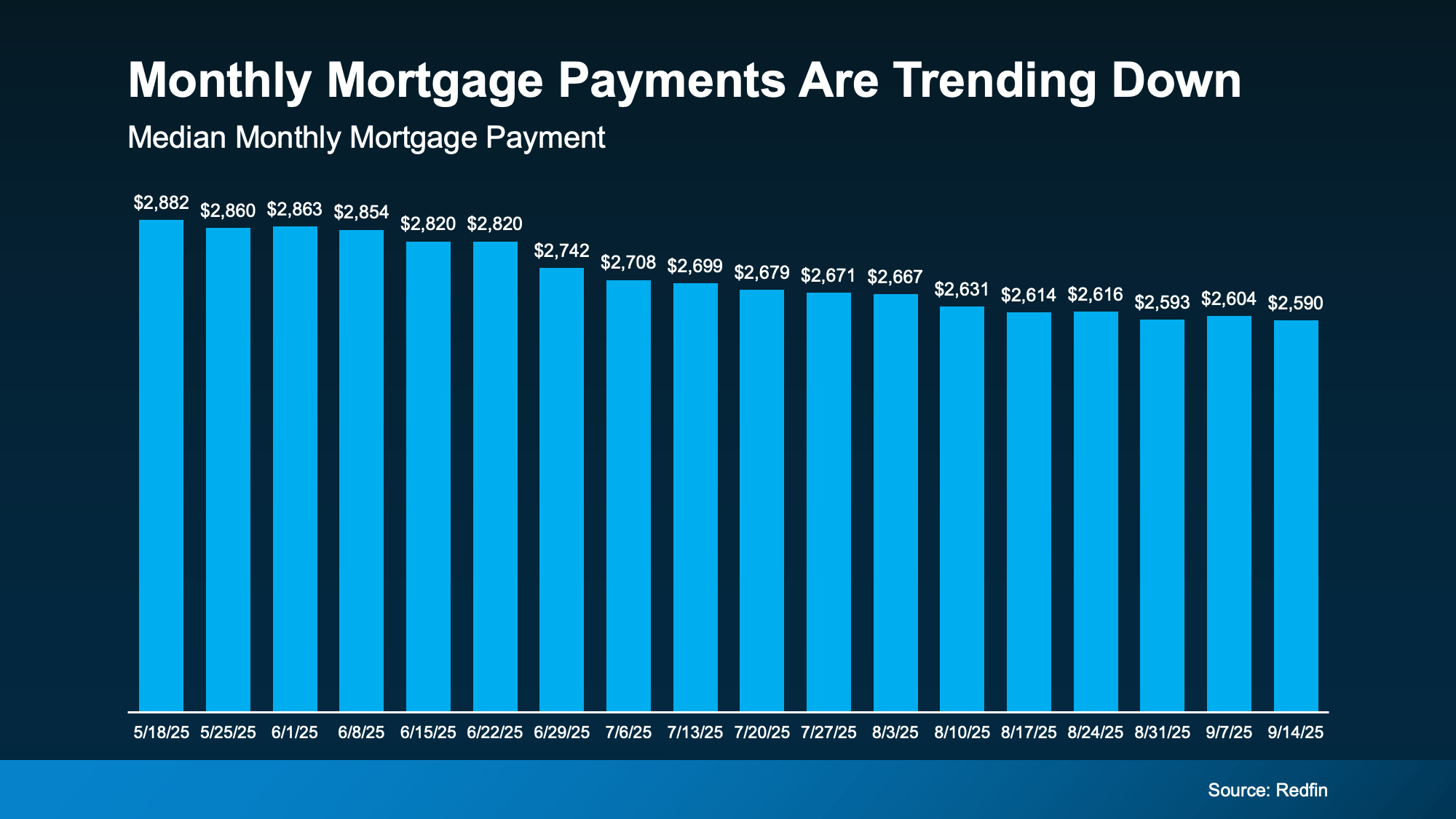

But this fall, the housing market is sending out some promising signals. For the first time in a long while, multiple affordability levers are shifting in buyers’ favor. According to recent Redfin data, the typical monthly mortgage payment has dropped more than $200 from its peak in May 2025. That’s not pocket change — that’s thousands of dollars saved over the course of a year.

So what’s behind this long-awaited break? Housing affordability boils down to three core factors:

-

Wages (your income)

And right now, all three are finally moving in the right direction — at the same time. That doesn’t mean buying a home has suddenly become “easy,” but it does mean it’s a little less daunting. Let’s break down the three reasons affordability is showing signs of improvement this fall.

1. Mortgage Rates Are Finally Easing — and It Matters More Than You Think

Why Mortgage Rates Play the Biggest Role in Affordability

When buyers talk about affordability, they often focus on the sticker price of a home. But the truth is, your monthly payment is more heavily influenced by mortgage rates than almost anything else.

Even small rate changes can mean the difference between a “manageable” payment and a “stretch-too-thin” one. For example:

-

A $400,000 loan at 7.0% = ~$2,660/month (principal + interest).

-

The same loan at 6.3% = ~$2,470/month.

-

That’s a $190 difference every month, or about $2,280 per year.

Multiply that over a 30-year loan, and you’re saving nearly $70,000.

This is why affordability headlines often focus on rates. They have an outsized impact on buying power.

The 2025 Rate Trend: From Peaks to Relief

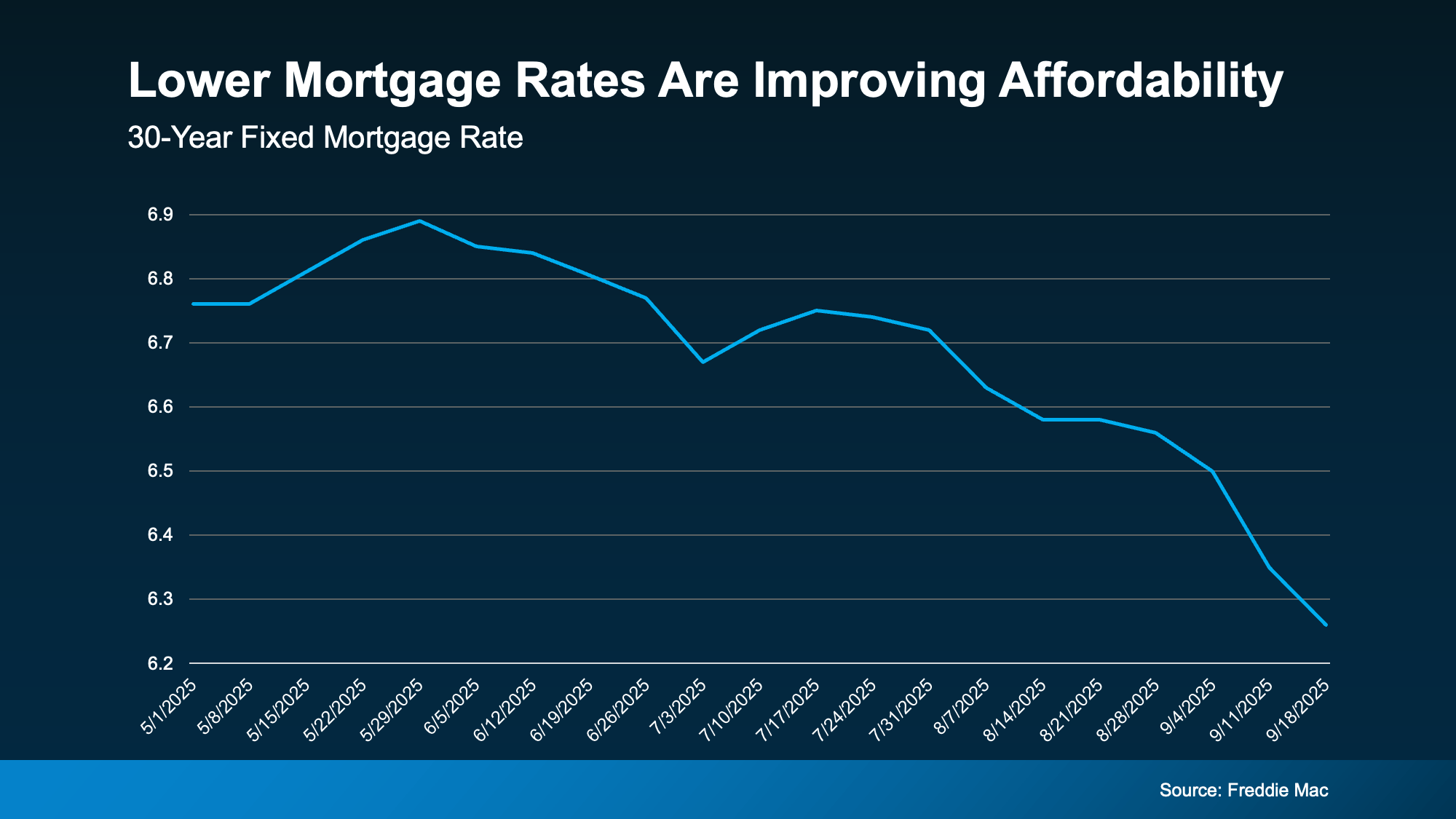

Earlier in 2025, mortgage rates climbed close to 7%, echoing the high levels we saw in 2023 and 2024. Many buyers simply walked away.

But as inflation cooled and the Federal Reserve signaled a pause on aggressive rate hikes, borrowing costs eased. As of fall 2025, 30-year fixed mortgage rates are trending between 6.2% and 6.6%.

That’s still higher than the sub-3% rates seen during the pandemic, but it’s a meaningful improvement compared to the 7%–8% territory of just a year ago.

Buyer Demand Responds to Lower Rates

We’re already seeing buyers respond to these changes. According to the Mortgage Bankers Association (MBA), purchase applications rose to their highest level since mid-2022 when rates dipped in September 2025.

As Joel Kan, VP and Deputy Chief Economist at MBA, explained:

“The downward rate movement spurred the strongest week of borrower demand since 2022. Purchase applications increased to the highest level since July and continued to run more than 20 percent ahead of last year’s pace.”

This signals renewed buyer confidence — something the housing market hasn’t felt in a while.

Voice-Search Friendly Q&A on Rates

-

Q: Will mortgage rates drop below 6% this year?

Economists are divided. Some believe rates could dip under 6% if inflation continues easing, but most forecasts expect them to hover in the mid-6% range through year-end. -

Q: How much can a 0.5% rate change save me?

On a $400,000 loan, even a half-point drop could reduce your payment by $100–$150 per month.

What Lower Rates Mean for You

For buyers, this rate relief could be the window of opportunity you’ve been waiting for. Whether you’re a first-time buyer using an FHA loan or a move-up buyer looking to lock in stability, the drop from 7% to mid-6% makes a tangible difference.

And here’s a pro tip: lenders don’t all offer the same rates. Shopping around could save you thousands. Even a 0.25% difference from one lender to another can shift your budget meaningfully.

2. Home Prices Have Stabilized — Finally Some Breathing Room

From Rapid Growth to Muted Increases

Between 2020 and 2023, home prices skyrocketed, climbing by double digits in many cities. Buyers who hesitated often found themselves priced out just months later.

But that relentless surge has cooled. As of fall 2025, national home price growth has slowed to low single digits. In fact, in some markets, prices have even dipped slightly.

As Odeta Kushi, Deputy Chief Economist at First American, explains:

“National home price growth remains positive, but muted — low single digits — and we expect this trend to continue in the second half of the year.”

This moderation is a welcome relief for buyers trying to plan budgets without the fear of “if I wait 30 days, it’ll cost $20,000 more.”

Regional Differences in Price Trends

The price story isn’t uniform across the U.S.:

-

Midwest and South: Still relatively affordable, with steady but modest growth.

-

West Coast: Many markets have seen slight dips as higher prices and cost of living cool demand.

-

Northeast: Growth has slowed, but inventory remains tight, keeping prices stable.

For buyers, this means opportunities vary widely depending on location. Some areas may offer rare price breaks, while others simply hold steady.

Why Price Moderation Matters for Buyers

Price stability gives buyers:

-

Budget Confidence: You can run numbers without worrying about huge swings.

-

Negotiation Power: In some markets, sellers are more willing to offer concessions.

-

Long-Term Security: Slower growth suggests the market is settling, reducing fears of overpaying.

Voice-Search Friendly Q&A on Prices

-

Q: Are home prices dropping in my city?

It depends. Some metros, especially on the West Coast, are seeing slight dips, while others remain stable. Checking local Redfin or Zillow reports is best. -

Q: Will home prices crash in 2025?

Experts say no. Instead, expect moderation and slower growth, not a full-scale drop.

3. Wages Are Outpacing Prices — A Subtle but Crucial Shift

The Wage Factor in Affordability

Even though rates and prices dominate headlines, wages play an equally important role. According to the Bureau of Labor Statistics, average hourly wages are growing at 3%–4% annually.

Why is this important? Because home price growth is slower than wage growth right now. In other words, your paycheck is finally gaining ground.

More Buyers Are Qualifying

As incomes rise:

-

Debt-to-income ratios look better on paper.

-

More households qualify for conventional loans.

-

Buyers feel more confident stretching into a higher price range.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Wage growth is now comfortably outpacing home price growth, and buyers have more choices.”

The Realistic Impact

To be clear, wage growth alone won’t suddenly make homes cheap. But paired with easing rates and slower price growth, it provides meaningful breathing room.

For example:

-

In 2023, a household earning $70,000 might have struggled to afford a $300,000 home.

-

Today, with wages closer to $85,000 and prices stabilizing, that same household could now realistically qualify — especially with a slightly lower rate.

Voice-Search Friendly Q&A on Wages

-

Q: Do higher wages make homes cheaper?

Not directly — but when incomes rise faster than home prices, affordability improves. -

Q: How much wage growth is needed to keep up with housing?

Experts suggest 3%–4% annual wage growth can offset low single-digit price increases, improving affordability over time.

What This Means for You: A Better Buying Window Is Opening

The combination of lower mortgage rates, slower price growth, and rising wages has made housing affordability better this fall than earlier in 2025.

That doesn’t mean buying a home is easy — inventory remains tight, and affordability is still stretched compared to pre-pandemic norms. But it does mean the numbers are working better than they have in years.

Redfin’s analysis shows the typical monthly mortgage payment is now $200–$300 lower than it was in May 2025. That shift alone could bring many sidelined buyers back into the market.

FAQs – Voice Search Optimized

-

Is fall 2025 a good time to buy a house?

Yes, it’s more favorable than earlier in the year. Lower rates, slower price growth, and stronger wages all contribute to better affordability. -

Will mortgage rates keep falling?

Rates may dip further if inflation eases, but most experts expect them to stay in the mid-6% range through the end of 2025. -

Are home prices expected to crash?

No — economists anticipate moderation, not a crash. Growth should remain in low single digits. -

How do wages affect affordability?

When incomes grow faster than home prices, your buying power improves, even if rates remain steady. -

Should I wait to buy until 2026?

Waiting could mean missing out on today’s lower rates and prices. If the math works for your budget now, it may be worth moving forward this fall.

Conclusion: Time to Reassess Your Numbers

If you’ve been waiting on the sidelines, this fall may be your chance to re-enter the housing market. Affordability isn’t perfect, but it’s finally moving in a better direction:

-

Rates are down from 7%+ highs.

-

Prices are stabilizing, offering more predictability.

-

Wages are rising, boosting buying power.

It may be the right time to run the numbers again, explore your local market, and see if homeownership now fits your budget.

After years of feeling like the market was running away, buyers finally have a little more breathing room — and that could make all the difference.

![]()

3 Reasons Affordability Is Showing Signs of Improvement This Fall

For the past couple of years, it’s been tough for a lot of homebuyers to make the numbers work. Home prices shot up. Mortgage rates too. And a number of people hit pause because it just didn’t feel possible. Maybe you were one of them.

But there’s some encouraging news. If you’ve been waiting for a better time to jump back in, affordability may finally be showing signs of improvement this fall.

The latest data from Redfin shows the typical monthly mortgage payment has been coming down, and is now about $290 lower than it was just a few months ago (see graph below):

And here’s why this is happening. The cost of buying a home really comes down to three things:

And here’s why this is happening. The cost of buying a home really comes down to three things:

- Mortgage rates

- Home prices

- Your wages

Right now, all three are finally moving in a better direction for you. While that doesn’t mean it’s suddenly easy to buy at today’s rates and prices, it does mean it’s not as challenging.

1. Mortgage Rates

Mortgage rates have come down compared to earlier this year. In May, they were roughly 7%. And now, they’re closer to 6.3% (see graph below):

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

And for some people, that’s been enough to make buying a home possible again. As Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), explained on September 10th:

“The downward rate movement spurred the strongest week of borrower demand since 2022 . . . Purchase applications increased to the highest level since July and continued to run more than 20 percent ahead of last year’s pace.”

2. Home Prices

After several years of prices rising very rapidly, price growth has finally slowed. As Odeta Kushi, Deputy Chief Economist at First American, puts it:

“National home price growth remains positive, but muted — low single digits — and we expect this trend to continue in the second half of the year.”

For buyers, that’s actually a big relief. That moderation makes it easier to plan your budget. And in some markets, prices have even dipped slightly. If you’re in one of the markets, you may be able to find something that’s more affordable than you’d expect.

3. Wages

According to the Bureau of Labor Statistics (BLS), wages are up near 4% annually. Lawrence Yun, Chief Economist at NAR, explains why that number is so important right now:

“Wage growth is now comfortably outpacing home price growth, and buyers have more choices.”

In other words, the typical paycheck is rising faster than home prices right now, which helps make buying a little more affordable. Now, it’s not a big difference, but in a market like this, every bit counts.

What This Means for You

Lower rates, slower price growth, and stronger wages might be enough to make the numbers finally work for you this fall.

While affordability is still tight, it’s a little easier on your wallet to buy now than it was just few months ago. Remember, data from Redfin shows the typical monthly mortgage payment is already around $290 lower than it was earlier this year.

Bottom Line

Have you been wondering if it’s worth taking another look at buying?

Let’s run the numbers together. We can go over your budget, see what’s changed, and figure out if this fall is the time to turn window-shopping into key-turning.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice