Why More Homeowners Are Giving Up Their Low Mortgage Rate

Why Homeowners in West Palm Beach Are Finally Giving Up Their Low Mortgage Rate for a Better Lifestyle

If you’re like a lot of homeowners around West Palm Beach, North Palm Beach, or Wellington, Florida — you may have thought: “I’d like to move… but I don’t want to give up my 3% rate.” That’s fair. That rate has been one of your best financial wins — and it can be hard to let go. But here’s what you need to remember…

A great rate won’t make up for a home that no longer works for you. Life changes, and sometimes, your home needs to change with it. And you’re not the only one making that choice.

The “Lock-In Effect” Is Starting to Ease

For years, many homeowners have been frozen in place by something experts call the “lock-in effect.” That’s when you won’t move because you don’t want to take on a higher rate on your next home loan. CNBC+2FHFA.gov+2

But data from Federal Housing Finance Agency (FHFA) — as analyzed by Redfin — shows the lock-in effect is slowly starting to ease for some people. Redfin+1

In the second quarter of 2025, the share of mortgaged homeowners with a rate of at least 6% rose to 19.7% — the highest level since 2015. Redfin+1

Meanwhile, the share of mortgages with a rate below 3% has shrunk to around 20.4% — down from peak levels during the pandemic housing boom. Redfin+1

What does this mean?

-

There are fewer low-rate loans in the system now.

-

More and more homeowners are realizing that staying put just because of a low rate might not make sense — especially if their life, space needs, or family goals have changed.

-

As a result, “rate-lock inertia” is loosening.

In other words: the emotional and financial weight of giving up a good rate is increasingly being outweighed by real, personal reasons to move.

Why More People Are Moving — Even if It Means Taking on a Higher Rate

You might wonder: why would someone agree to a higher mortgage rate after enjoying a low one for years? It’s simple: sometimes you can’t put your life on pause anymore. Families grow, jobs change, priorities shift — and a house that once fit perfectly may not fit at all anymore. And that’s okay.

Many homeowners across the U.S. — including those in Florida’s West Palm Beach, North Palm Beach, and Wellington — are recognizing that staying in a house simply because of a historic Mortgage Rate isn’t worth it if it no longer meets their needs.

According to Realtors and housing-market observers, the reasons people choose to move often have nothing to do with finance — but everything to do with lifestyle: needing more space for children, wanting to downsize after retirement, relocating for work, or simply desiring a change of scenery. Panza Home Group+1

For many, the emotional and practical benefits of a home that truly fits outweigh the pain of giving up a lower mortgage rate. They value the flexibility, peace of mind, and alignment with their real-life needs more than holding on to a 2–3% loan.

This “rate vs. life fit” trade-off has become more common — manifesting in more listings, more mobility, and a subtle but meaningful shift in homeowner behavior.

Market Conditions & Forecasts That Make Moving More Feasible

Another factor nudging homeowners toward action: market conditions are gradually improving — making a move less painful than it would have been during 2022–2024 period of peak rates.

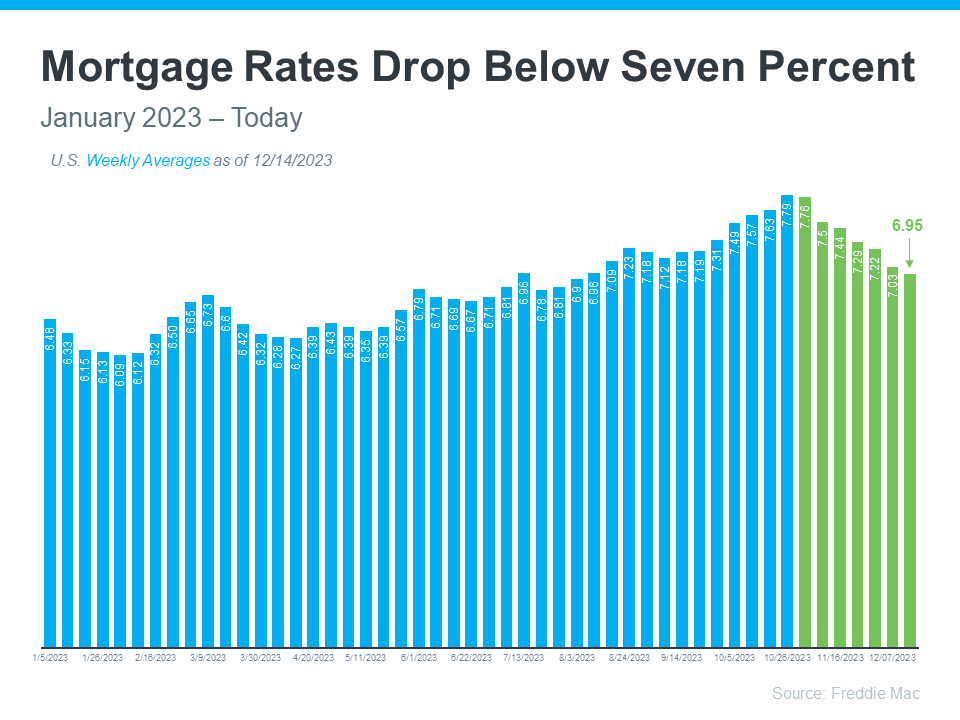

Across the U.S., and including markets in Florida, there are early signs that Mortgage Rates may continue to stabilize or even decrease modestly over the next 12–18 months. That possibility reduces the long-term penalty of giving up a low rate now. mortgage-underwriters.org+2Freddie Mac+2

Plus, as more people move, housing supply becomes less constrained — which may moderate price increases and give buyers and sellers more options. That’s particularly relevant for those seeking a different neighborhood or home style around West Palm Beach or Wellington.

For many homeowners, this “new normal” for rates makes the trade-off (rate vs home fit) more acceptable than it was during the early 2020s.

Life Priorities: The “5 D’s” That Often Outweigh a Low Rate

When you examine why people are choosing to move despite a previously low rate, you see recurring themes — life priorities that simply can’t wait. Real estate advisors often classify these under the “5 D’s” of life-driven moves:

-

Diplomas: A recent degree, a career boost, or a job change may give you more financial flexibility — enough to consider a better home in a different area.

-

Diapers: Growing families needing more bedrooms, bigger yards, or safer neighborhoods.

-

Divorce (or new marriage): Changing household dynamics — maybe it’s time for two households, or combining families — meaning your current home no longer fits.

-

Downsizing: Kids have grown and left; now you want less maintenance, lower costs, and a simpler lifestyle.

-

Death or family changes: Loss of a loved one, or desire to be closer to surviving family — prompting relocation closer to support networks.

These aren’t hypothetical scenarios. They reflect the real, sometimes emotional, decisions behind why homeowners choose to leave a “good rate” behind.

In markets like North Palm Beach, West Palm Beach, or Wellington, where community, family life, and lifestyle matter a lot — those priorities often end up outweighing financial attachment to a low rate.

Reframing the Question: “Should I Move?” → “How Long Am I Willing to Stay Somewhere That No Longer Fits My Life?”

For many homeowners, the old question — “Should I move even if it means giving up a low rate?” — is being replaced by a deeper one: “How much longer am I willing to stay somewhere that no longer fits my life?”

Because homes are more than financial investments — they are living spaces. They grow and shrink in value as our lives evolve.

Holding on to a low rate may feel like smart money. But if the house no longer serves your family’s goals, ambitions, or lifestyle — is that smart living?

If you’re working with a trusted professional such as Christian Penner — Mortgage Broker, Real Estate Advisor at America’s Mortgage Solutions (AMS) — you can run the numbers together to see:

-

What your equity looks like today,

-

What you can afford for your next home in West Palm Beach, North Palm Beach, or Wellington,

-

Whether the benefits of a new home outweigh the cost of a higher rate.

For many, the answer has become: yes — the trade-off is worth it.

What It Means for Prospective Movers, Sellers & Buyers in Florida

If you’re considering a move — here’s how this shift impacts you:

For Sellers

-

More homeowners willing to sell means increased inventory. In West Palm Beach, North Palm Beach, or Wellington — that could translate to more options for those looking to list.

-

With more supply, the pressure on prices may ease slightly — but demand remains stable among those needing real lifestyle changes.

For Buyers

-

More choices in neighborhoods and home styles: bigger homes, downsized homes, condos, newer builds, etc.

-

Less competition than during the pandemic peak — especially if some sellers price realistically.

-

Still pay attention to rates — but with guidance (e.g. from Christian Penner at AMS), you can structure a loan that balances affordability + lifestyle fit.

For Current Low-Rate Homeowners

-

Reassess: Are you staying only because of a low rate — or staying because the home fits your life?

-

If life has changed (family, career, preferences) — it may be time to consider selling or downsizing.

-

Work with a trusted advisor (like Christian Penner) to get up-to-date mortgage and home-value data, especially in your Florida locale.

Common Concerns — Addressed

What about “losing” the 3% rate?

It’s true: giving up a 3% (or other low) rate is a financial hit — but it’s only one piece of the puzzle. If your current home no longer works for you, the emotional and lifestyle benefits of moving can outweigh the cost.

Will taking on a higher rate always make financial sense?

Not always. That’s why it’s important to calculate: new mortgage payments, expected home-value appreciation, resale potential, and personal lifestyle benefits. An experienced mortgage broker like Christian Penner (AMS) can help assess if the move is financially sound.

Should I wait until rates drop?

You could — but waiting means potentially sacrificing quality of life, comfort, and alignment with your goals. For many people, the very real reasons you may need a new home outweigh the hope of a lower rate.

Real-Life Scenarios

Scenario 1: Family outgrows the home

The house you bought 8–10 years ago worked for a starter family. Maybe it had 3 bedrooms and a small yard. Now the kids need their own rooms. Maybe grandparents are moving in. You need more space, a bigger yard, and a better school district.

Yes — giving up your lower mortgage rate hurts. But the benefit of comfortable, practical living and more room for your family’s goals can make the move worth it.

Scenario 2: Downsizing after retirement or kids moved out

Kids are grown; the house feels too big. Maintenance, yard work, and bills are more than you want. You want a simpler lifestyle. A smaller home, less upkeep, and lower stress.

Even if it means a higher rate — downsizing can reduce other costs (utilities, maintenance) and improve quality of life.

Scenario 3: Career change, remote work, or lifestyle shift

A job transfer. Remote-work flexibility. Desire to live closer to friends, family, or amenities. Maybe you want a neighborhood with walkability, good community vibe, closer to beaches or modern conveniences — especially in Palm Beach/North Palm Beach area.

Your old home may not check these boxes anymore — and the trade-off again becomes about lifestyle and fit.

Why Working with a Trusted Advisor Matters — Spotlight on Christian Penner (AMS)

Making a decision like this is rarely just about interest rates. That’s why having an experienced Mortgage Broker / Real Estate Advisor makes a big difference.

With someone like Christian Penner at America’s Mortgage Solutions (AMS), you get:

-

Local expertise — knowledge about West Palm Beach, North Palm Beach, Wellington market dynamics.

-

A clear-eyed assessment of your home equity, potential sale value, and realistic budget for your next home.

-

Help balancing financial and lifestyle goals — ensuring that your next home aligns with where you are in life, not just your loan terms.

If you’re considering a move — connecting with a trusted advisor like Christian can help you make an informed decision — not just a financial one, but a life-based one.

Final Thoughts: Life Doesn’t Wait for the Perfect Rate — Maybe You Shouldn’t Either

Low mortgage rates were a blessing. They helped many families buy homes and build equity fast. But rates aren’t forever — and neither is your life situation.

Your home should grow with you. Whether it’s more space for a growing family, less house to maintain after retirement, or a fresh start in a new neighborhood — sometimes the financial sacrifice of giving up a low rate is worth it.

If your current home doesn’t fit your life anymore — or doesn’t support your family’s goals — maybe the more important question isn’t: “Should I move?” — but “How long am I willing to stay somewhere that no longer fits?”

With improving market conditions, mortgage rates stabilizing, and trusted advisors like Christian Penner (AMS) ready to guide you — your next home loan might be not just a financial step, but a step toward the life you deserve.

FAQ (Voice-Search Friendly Q&A)

Q: What is the “lock-in effect” in real estate?

A: The “lock-in effect” refers to homeowners’ reluctance to sell because they have historically low fixed mortgage rates — making them hesitant to take on a higher rate for a new loan.

Q: How many U.S. homeowners now have a mortgage rate above 6%?

A: As of the second quarter of 2025, about 19.7% of mortgaged homeowners have a rate of at least 6% — the highest share since 2015.

Q: Why would someone give up a low mortgage rate?

A: Because life changes — growing families, downsizing after retirement, job changes, desire for a different neighborhood — may outweigh the financial benefit of keeping a low rate.

Q: Are mortgage rates expected to fall again soon?

A: Many experts believe mortgage rates may modestly ease in the coming months, which could make moving or refinancing more attractive.

Q: How do I know if it makes sense to sell a home with a low mortgage rate?

A: Work with a trusted mortgage broker or real estate advisor — assess your equity, lifestyle goals, cost vs benefit of a new home, and rate forecasts.

Source: “America’s Mortgage Solutions (AMS)”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice