Why Mortgage Rates Could Continue To Decline

When you read about the housing market, you’ll probably come across some information about inflation or recent decisions made by the Federal Reserve (the Fed). But how do those two things impact you and your homebuying plans? Here’s what you need to know.

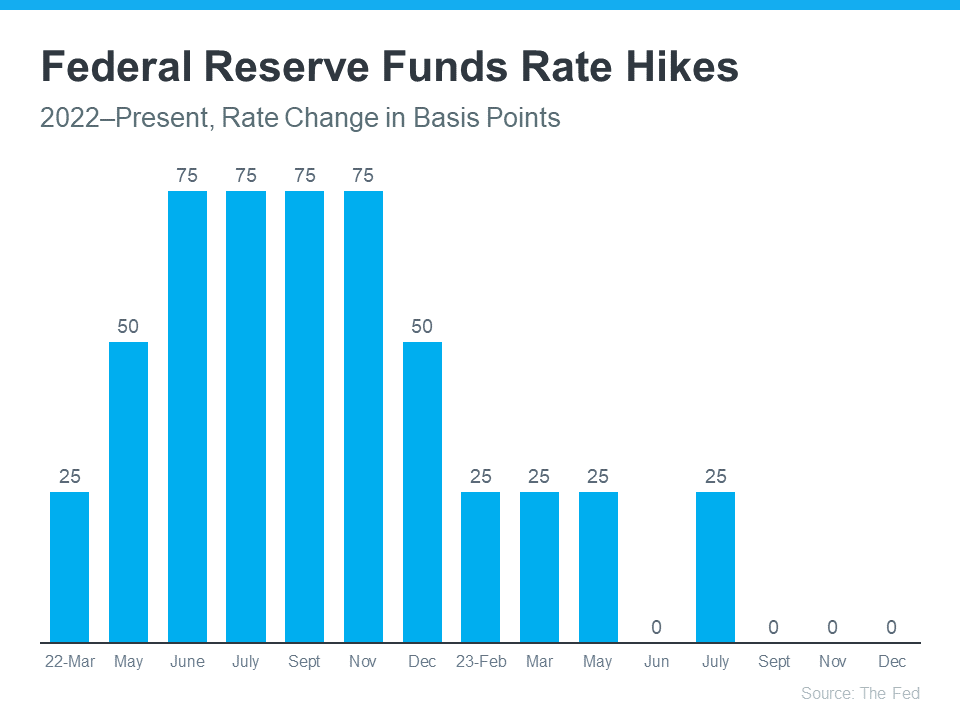

The Federal Funds Rate Hikes Have Stalled

One of the Fed’s primary goals is to lower inflation. In order to do that, they started raising the Federal Funds Rate to slow down the economy. Even though this doesn’t directly dictate what happens with mortgage rates, it does have an impact.

Recently inflation has started to cool, a signal those increases worked and are bringing inflation back down. As a result, the Fed’s hikes have gotten smaller and less frequent. In fact, there haven’t been any increases since July (see graph below):

And not only has the Fed decided not to raise the Federal Funds Rate the last three times the committee met, they’ve signaled there may actually be rate cuts coming in 2024. According to the New York Times (NYT):

“Federal Reserve officials left interest rates unchanged in their final policy decision of 2023 and forecast that they will cut borrowing costs three times in the coming year, a sign that the central bank is shifting toward the next phase in its fight against rapid inflation.”

This indicates the Fed thinks the economy and inflation are improving. Why does that matter to you and your plans to buy a home? It could end up leading to lower mortgage rates and improved affordability.

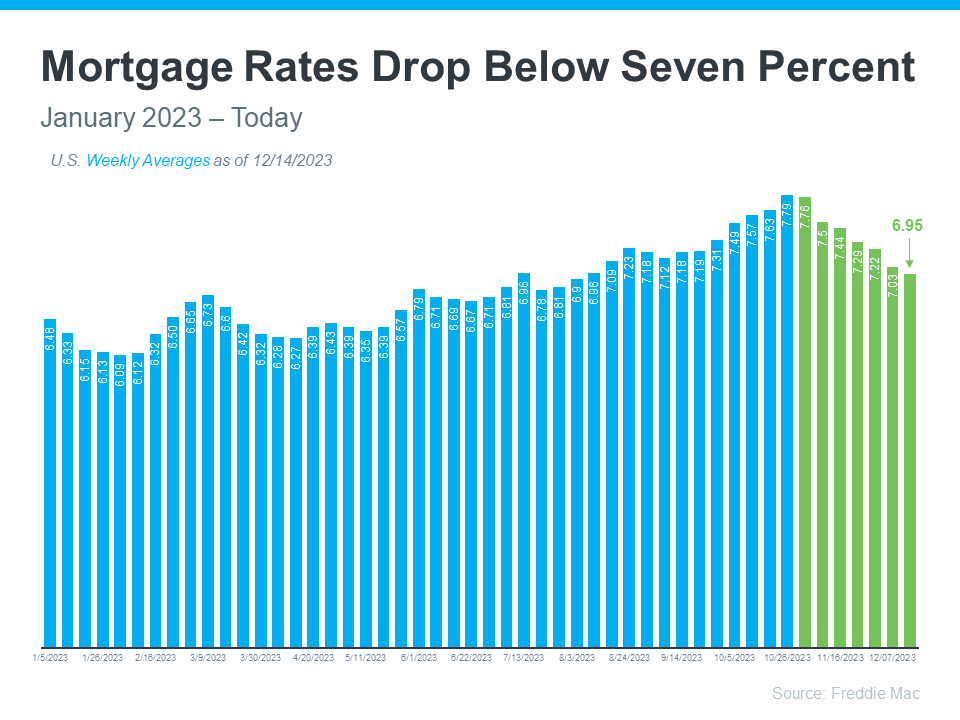

Mortgage Rates Are Coming Down

Mortgage rates are influenced by a wide variety of factors, and inflation and the Fed’s actions (or as has been the case recently, inaction) play a big role. Now that the Fed has paused the increases, it looks more likely mortgage rates will continue their downward trend (see graph below):

Although mortgage rates may remain volatile, their recent trend combined with expert forecasts indicate they could continue to go down in 2024. That would improve affordability for buyers and make it easier for sellers to move since they won’t feel as locked-in to their current, low mortgage rate.

Bottom Line

The Fed’s decisions have an indirect impact on mortgage rates. By not raising the Federal Funds Rate, mortgage rates are likely to continue declining. Let’s connect so you have expert advice about changes in the housing market and how they affect you.

Unlocking the Enigma: Why Mortgage Rates Might Continue Their Descent

In the intricate dance of economic forces, the Federal Reserve orchestrates a symphony that resonates through various sectors. One of the key crescendos in this financial composition is the pulse of mortgage rates. For those contemplating their homebuying plans, the interplay of factors shaping these rates can be both mystifying and crucial. Let’s delve into the labyrinth of financial dynamics and explore why the melody of low mortgage rates might persist, impacting not just individual plans to buy a home, but the broader canvas of the Housing Market itself.

The Conductor’s Baton: Federal Funds Rate

At the heart of this symphony is the elusive Federal Funds Rate. This interest rate, set by the Federal Reserve, serves as the conductor’s baton, guiding the rhythm of economic activities. As the economy waltzes through various phases, the Federal Reserve deftly adjusts this rate to maintain harmony.

Recently, inflation, the tempestuous dancer on the economic stage, has twirled into the spotlight. The Federal Reserve, donning the role of vigilant choreographer, is carefully assessing the impact of inflation on the economy. In response to the inflationary pirouettes, the central bank contemplates the delicate act of raising the Federal Funds Rate.

The Dance of Mortgage Rates

Now, how does this influence the intricate choreography of mortgage rates? Picture a waltz where each participant moves in tandem with the central rhythm – that’s the relationship between the Federal Funds Rate and mortgage rates. When the Federal Reserve adjusts the former, the latter follows suit.

In the realm of financial intricacies, the concept is simple yet profound. If the Federal Reserve raises interest rates, the dominos fall, nudging mortgage rates upward. Conversely, if the central bank opts for a gentler tune, keeping the Federal Funds Rate at a lower octave, mortgage rates may pirouette gracefully in a downward motion.

Economic Symphony and Homebuying Plans

For those contemplating their plans to buy a home, this financial ballet carries significant implications. A lower Federal Funds Rate often translates to low mortgage rates, an enticing melody for prospective homebuyers. Imagine the allure of securing a mortgage at historically favorable terms, a rare encore in the real estate world.

The allure is not lost on the astute observer. Individuals with homebuying plans find themselves at the crossroads of an economic sonata. The question lingers – will the music of low mortgage rates persist, or are we on the brink of a new movement?

The Pulse of the Housing Market

To discern the future cadence of mortgage rates, we must also scrutinize the heartbeat of the Housing Market. The market, a living entity shaped by myriad factors, is both responsive and anticipative.

As low mortgage rates become the melody du jour, the Housing Market experiences a surge in activity. Prospective buyers, enticed by the allure of affordable financing, are drawn to the stage. Sellers, sensing the opportune moment, choreograph their own moves – some for strategic entry, others for a graceful exit.

This symphony, however, is not without its own dramatic crescendos. Recently, inflation has cast a shadow on the economic stage, prompting cautious reflections among market participants. In this nuanced dance, the delicate balance between supply and demand, buyer enthusiasm, and seller motivation shapes the destiny of mortgage rates.

A Duet with Inflation

The recent inflationary saga introduces a compelling subplot to the narrative. As the Federal Reserve contemplates the rise of the Federal Funds Rate in response to inflation, the duet with mortgage rates gains complexity. Will the ascent of the Federal Funds Rate dampen the enchanting notes of low mortgage rates that have echoed through the real estate corridors?

The answer lies in the confluence of economic forces. While inflation may exert pressure on the central bank to raise interest rates, the broader economic ensemble also considers employment, growth, and the delicate equilibrium of the Housing Market. This intricate dance requires finesse, a choreography where each step is calibrated with precision.

Sellers on the Move

As the central bank contemplates its moves, sellers in the Housing Market ponder their own choreography. The prospect of rising mortgage rates can be a catalyst for those considering a strategic exit. In this ballet of real estate, timing is everything.

For those sellers with a discerning eye on the financial overture, the current scenario presents a delicate balance. The allure of low mortgage rates attracts buyers, yet the specter of potential rate hikes prompts strategic considerations. The decision to move, a dance of financial pragmatism, is influenced not just by the desire for change but by the pulse of economic variables.

The Ongoing Sonata

As the symphony of economic forces continues, the fate of mortgage rates remains an ongoing sonata. For those with plans to buy a home, the journey is one of anticipation, navigating the harmonies of economic policy, market dynamics, and the ever-present specter of inflation.

In conclusion, the convergence of factors – the nuanced dance between the Federal Funds Rate, inflation, and the ebb and flow of the Housing Market – shapes the trajectory of mortgage rates. The allure of low mortgage rates may persist, a melody echoing through the corridors of real estate. As the financial ballet unfolds, those with homebuying plans find themselves not just spectators but active participants in the ongoing narrative of economic rhythms.

Harmonizing Futures: The Melody of Mortgage Rates

Economic Counterpoint: Federal Reserve’s Overture

In the ever-evolving economic symphony, the Federal Reserve assumes the role of a skilled composer, orchestrating an overture that reverberates across markets. The anticipation of a potential rise in the Federal Funds Rate adds an intriguing note to this composition. As the central bank fine-tunes its policies in response to inflation, the harmonics of mortgage rates find themselves caught in the ebb and flow of economic nuances.

The intricacies of the financial ballet extend beyond mere interest rate adjustments. They weave into the fabric of market psychology, influencing not only homebuying plans but also the strategic maneuvers of sellers. In this intricate dance, both prospective buyers and seasoned sellers await cues, attuned to the tempo set by the Federal Reserve’s baton.

Inflation’s Pas de Deux with Mortgage Rates

The inflationary dance, characterized by its unpredictable pirouettes, introduces an element of suspense. Will the Federal Reserve raise the interest rate to counteract inflation, or will the current melody of low mortgage rates continue its enchanting refrain? This pas de deux between inflation and interest rates shapes the contours of the economic stage.

For those contemplating plans to buy a home, the interplay becomes a delicate consideration. The allure of favorable mortgage terms collides with the uncertainty of future rate movements. The decision to enter the real estate waltz becomes a strategic one, guided not just by personal aspirations but by a nuanced understanding of economic choreography.

Low Mortgage Rates and the Homebuyer’s Delight

In the current financial sonata, the resonance of low mortgage rates is a melody that echoes through the corridors of opportunity. Prospective homebuyers, eager to actualize their plans to buy a home, find themselves on a stage where the spotlight is cast on affordability. The allure of securing a mortgage at historically low rates becomes a tantalizing prospect, inviting individuals to partake in the narrative of homeownership.

As the interest rate pendulum sways, potential buyers engage in a contemplative dance. The timing of their entrance into the real estate theater becomes pivotal, influenced by a delicate balance of economic factors. The decision to embark on homeownership is not merely a financial transaction; it is a participatory act in the ongoing drama of economic rhythms.

Housing Market Choreography

Beyond individual decisions, the Housing Market itself becomes a stage for collective movements. Sellers, attuned to the dynamics of supply and demand, embark on their own choreographic endeavors. The prospect of rising mortgage rates may prompt some sellers to expedite their plans, seizing the current favorable conditions. In this symphony of real estate, the decision to move becomes a strategic maneuver, a dance with the market’s pulse.

For those sellers contemplating a change, the timing becomes an art. The allure of a vibrant Housing Market, fueled by low mortgage rates, is juxtaposed against the potential for a shift in the economic rhythm. Sellers become not just spectators but active participants, their decisions shaping the overarching narrative of the real estate ballet.

The Art of Financial Navigation

In this complex composition, financial pragmatism becomes the compass guiding both buyers and sellers. The allure of low mortgage rates persists, but it is accompanied by a sense of anticipation. The economic symphony, with its intricate movements, demands a nuanced understanding of the interplay between interest rates, inflation, and market dynamics.

As the sonata unfolds, those with plans to buy a home and sellers alike navigate the currents of change. The financial stage, with its ever-shifting dynamics, invites participants to engage in a dance of adaptability. The melody of mortgage rates continues, an evolving composition where each note resonates with the pulse of economic forces.

Conclusion: A Symphony in Flux

In the grandeur of economic symphonies, the trajectory of mortgage rates emerges as a dynamic melody, influenced by the interplay of central bank policies, inflationary movements, and the choreography of the Housing Market. The allure of low mortgage rates remains, inviting individuals to participate in the ongoing narrative of real estate.

As the financial ballet progresses, prospective homebuyers and strategic sellers find themselves engaged in a dance with the unknown. The harmonics of the economic overture unfold, shaping the future cadence of mortgage rates. In this ever-evolving symphony, the art lies not just in observation but in the ability to navigate the changing currents of the financial landscape. The melody continues, and the participants in this economic ballet remain both the audience and the performers, contributing to a harmonious, yet unpredictable, financial future.

Read from source: “Click Me”

– “Why Mortgage Rates Could Continue To Decline” –

The Christian Penner Mortgage Team | Cell/Text: (561) 316-6800

|

|

|

|

|

|

|

|

|

|

HomeBot: Build more wealth with your home

-

Homeowners👉https://hmbt.co/nwCdmG

-

Homebuyers👉 https://hmbt.co/G8fMT

-

Realtors 👉 https://youtu.be/wXROJXQWgug

-

Join here Realtors 👉 https://join.homebot.ai/sponsor/368289?type=real-estate-agent

Check Our Reviews:

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Get Pre-Approved Today