What Everyone’s Getting Wrong About the Rise in New Home Inventory

Meta Description:

Rising new home inventory has many worried about another housing crash. Here’s why today’s market isn’t 2008—and what buyers and sellers should know.

Introduction

If you’ve been scrolling through real estate headlines recently, you’ve probably seen a lot of noise about new home inventory. Some outlets say new construction inventory is at its highest level since the 2008 crash, sparking fears of a repeat housing collapse. For anyone who lived through that painful downturn, these comparisons can feel unsettling.

But here’s the truth: not everything you’re seeing online is the full picture. Many headlines are designed to grab clicks, not provide balanced context. The reality is that today’s rise in new home inventory signals something very different from what we saw leading up to the 2008 crash.

By breaking down the latest data, listening to housing economists, and comparing today’s conditions with the past, we’ll uncover why this situation is fundamentally different from 2008. More importantly, you’ll walk away knowing what it really means for buyers, sellers, and the future of the housing market.

The Fear Behind Rising New Home Inventory

There’s no denying it: new home inventory has surged to its highest levels in years. On the surface, that sounds alarming. After all, the last time new homes piled up like this was before the housing bubble burst.

But here’s the catch: rising new home inventory doesn’t automatically signal oversupply or a market crash.

-

Why headlines look scary: News outlets love framing the data as “highest since the crash” because it draws attention.

-

The truth: Without context—like existing home inventory and demand levels—this statistic alone can be misleading.

🔎 Q&A:

-

“Is new home inventory in 2025 like 2008?”

No. In 2008, the issue was oversupply across both new and existing homes combined. In 2025, we’re seeing new builds increase, but total supply is still far below crash-era levels.

Why This Isn’t Like the 2008 Housing Crash

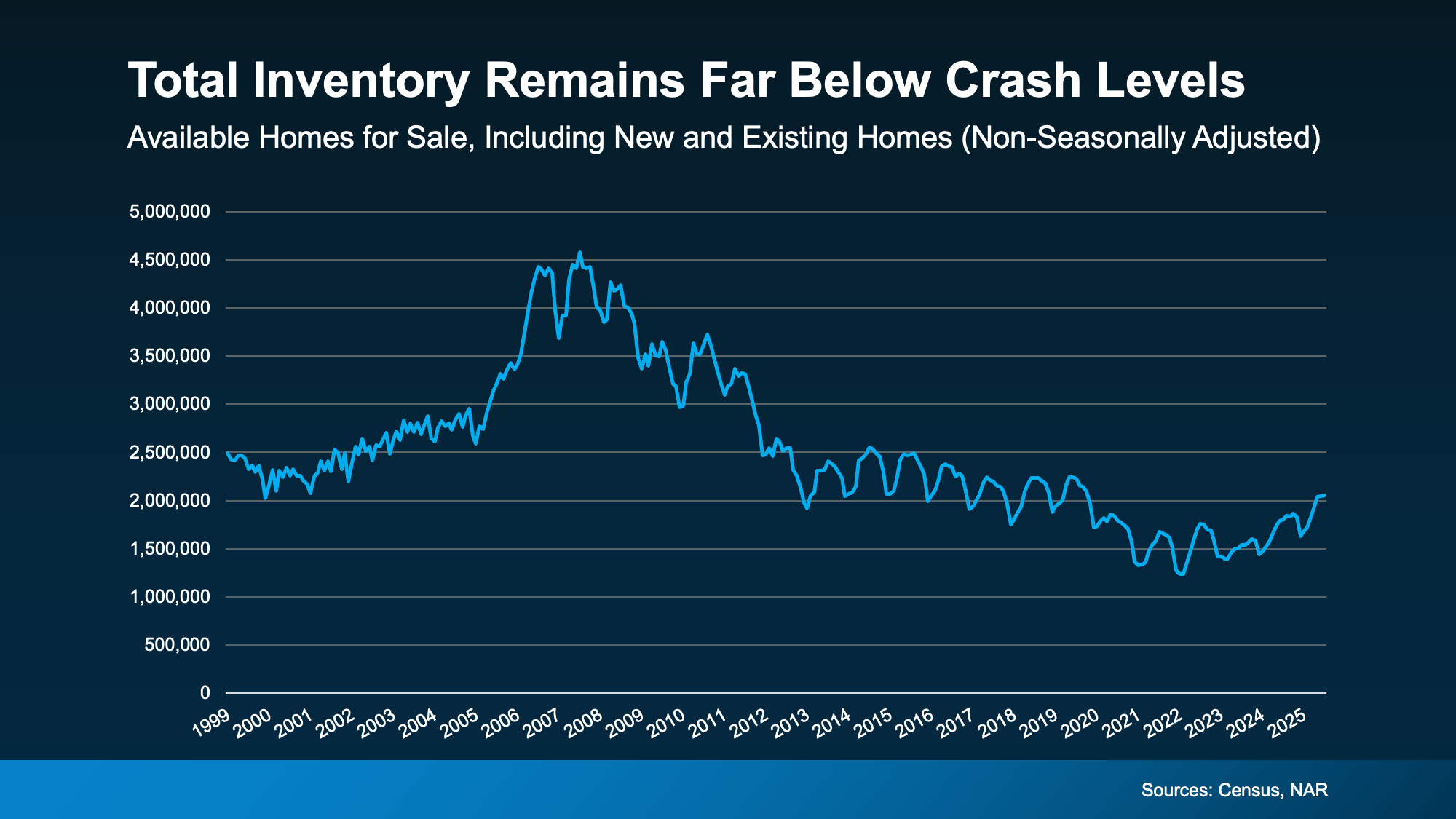

To understand why today isn’t a repeat of the crash, you need to look at total inventory—not just new homes.

-

2008 market: Builders overproduced, and existing homeowners flooded the market with distressed sales, pushing supply to unsustainable highs.

-

2025 market: While new home supply has increased, existing home supply remains constrained. Many homeowners are “locked in” with ultra-low mortgage rates and aren’t selling.

Key Data Points:

-

In 2008, housing supply reached over 10–11 months nationwide.

-

In 2025, total supply (new + existing) is still well below 8 months, which economists say is the danger zone for sustained price declines.

📊 Takeaway: Saying new home inventory is “at 2008 levels” ignores the full picture. Today’s total supply is nowhere near a crash-level surplus.

🔎 Q&A:

-

“How much housing supply do we have in 2025?”

As of mid-2025, new homes average 9.2 months of supply, while existing homes are just 4.7 months, putting the national total below crash territory.

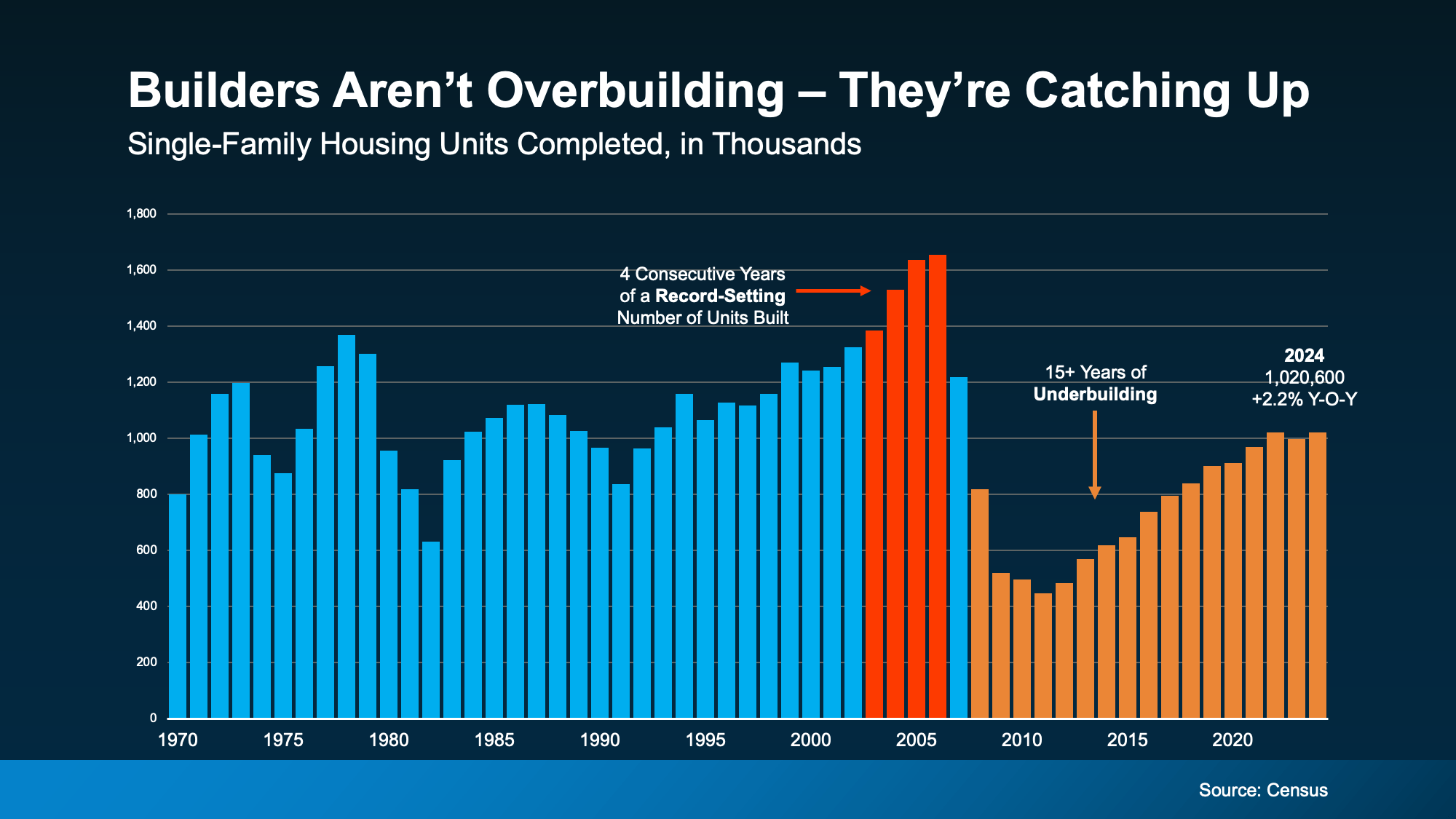

Builders Have Underbuilt for Over a Decade

Perhaps the most overlooked fact in this conversation is the long stretch of underbuilding since 2008.

When the housing market collapsed, builders slammed on the brakes. Construction slowed dramatically, and for the next 15 years, they didn’t build enough homes to keep up with demand.

The Result:

-

By 2023, the U.S. faced a housing shortage of 7.2 million homes.

-

Realtor.com estimates it could take another 7.5 years of strong building to close the gap.

-

Even with today’s increase in construction, the market is still digging out of a deep supply hole.

📊 Data Visualization (Described):

-

Red zone (pre-2008): Overbuilding leading to surplus.

-

Orange zone (2008–2023): Prolonged underbuilding, creating shortage.

-

Blue zone (2024–2025): Gradual recovery, but still far from balanced supply.

🔎 Q&A:

-

“Why are we still short on homes after 2008?”

Because builders underproduced for more than a decade, creating a supply deficit that will take years to fix.

The Current Inventory Surge Explained

So why are we suddenly seeing more new homes available?

-

Builders Catching Up: They’re finally responding to years of pent-up demand.

-

Affordability Pressures: Higher mortgage rates have slowed buyer activity, leaving some new builds sitting longer.

-

Discounting Strategies: To attract buyers, many builders are offering incentives and lowering prices.

New vs. Existing Prices

-

As of summer 2025, new homes are selling for an average of $19,000 less than existing homes.

-

This reversal (new builds cheaper than resales) is unusual, highlighting the pressure builders face to move inventory.

🔎 Q&A:

-

“Are builders lowering home prices in 2025?”

Yes. Many are offering price cuts, mortgage rate buy-downs, and incentives to attract buyers as rates remain elevated.

Why Total Inventory Still Signals Strength

When you add new and existing homes together, supply looks very different from 2008.

-

New Homes: 9.2 months of supply (elevated).

-

Existing Homes: 4.7 months of supply (tight).

-

Combined: Still below levels associated with a housing crash.

Expert Consensus:

Economists agree that while certain local markets may feel more balanced, there’s no national glut of housing. Demand continues to outpace supply overall, especially in affordable price ranges.

🔎 Q&A:

-

“Does more new home inventory mean prices will fall?”

Not necessarily. Builders are discounting to move homes, but total inventory is still too low to trigger nationwide price declines.

Lessons from the Past: 2008 vs. 2025 Market Dynamics

Comparisons to the crash ignore the very different fundamentals of today’s market:

-

Lending Standards: In 2008, risky subprime loans fueled unsustainable buying. In 2025, lending requirements remain strict.

-

Equity Levels: Homeowners today have record-high equity, reducing foreclosure risk.

-

Investor Behavior: Speculative buying drove the bubble; today’s demand is rooted in real household growth.

🔎 Q&A:

-

“Why won’t the housing market crash like 2008?”

Because today’s buyers are financially stronger, lending is stricter, and supply is still historically low.

What Buyers Should Know in 2025

For buyers, today’s market presents unique opportunities:

-

New Construction Discounts: Builders are cutting prices and offering incentives.

-

Less Competition: Higher mortgage rates have reduced bidding wars.

-

Long-Term Outlook: Buying during a shortage positions owners for appreciation once rates normalize.

🔎 Q&A:

-

“Is 2025 a good year to buy a home?”

Yes—especially if you’re considering new construction where discounts and incentives are available.

What Sellers Should Know in 2025

For sellers, it’s important to recognize:

-

Demand Remains Strong: Especially for well-priced, move-in-ready homes.

-

Competitive Pricing Matters: With new builds offering incentives, sellers need to stay realistic.

-

Market Varies by Region: Some areas may feel tighter than others.

🔎 Q&A:

-

“Should I sell my home now or wait until 2026?”

If you’re moving anyway, selling now makes sense. Waiting for a “better market” may not guarantee higher returns.

The Future of Housing Supply

Looking ahead, the housing market is expected to remain undersupplied for years:

-

Realtor.com Forecast: Roughly 7.5 years needed to close the gap.

-

Challenges: Labor shortages, zoning restrictions, material costs, and high rates limit rapid building.

-

Long-Term Outlook: A more balanced market may emerge in the early 2030s.

🔎 Q&A:

-

“When will the housing shortage end?”

Experts estimate not before 2032–2033, assuming consistent building activity.

Bottom Line

Yes, new home inventory is at its highest level since 2008. But no, this is not 2008 all over again.

-

Today’s surge reflects builders finally catching up after more than a decade of underbuilding.

-

Total inventory is still well below the dangerous oversupply levels that triggered the last crash.

-

Homeowners are financially stronger, lending standards are tighter, and demand continues to outpace supply.

👉 If you’re a buyer, there are opportunities in today’s market—especially with builder discounts. If you’re a seller, demand remains strong but competitive pricing is key. Either way, the data shows we’re not on the verge of a housing crash.

If you have questions or want to talk about what builders are doing in our area, let’s connect.

FAQs

1. Will the housing market crash in 2025?

No. Total inventory remains too low to trigger a nationwide crash, and lending standards are stronger than in 2008.

2. Why are new homes cheaper than existing homes in 2025?

Builders are discounting prices and offering incentives to attract buyers as mortgage rates remain high.

3. How many homes are we short in the U.S.?

As of 2024, the U.S. faced a shortage of around 7.2 million homes.

4. Is it better to buy new construction or existing homes in 2025?

New construction may offer better deals and incentives, but existing homes in desirable areas remain competitive.

5. When will housing inventory return to normal levels?

Experts say it may take 7–10 years of steady building before the shortage is fully resolved.

(see graph below)

If you have questions or want to talk about what builders are doing in our area, let’s connect.

(read more and see graph below)

![]()

What Everyone’s Getting Wrong About the Rise in New Home Inventory

You may have seen talk online that new home inventory is at its highest level since the crash. And if you lived through the crash back in 2008, seeing new construction is up again may feel a little scary.

But here’s what you need to remember: a lot of what you see online is designed to get clicks. So, you may not be getting the full story. A closer look at the data and a little expert insight can change your perspective completely.

Why This Isn’t Like 2008

While it’s true the number of new homes on the market hit its highest level since the crash, that’s not a reason to worry. That’s because new builds are just one piece of the puzzle. They don’t tell the full story of what’s happening today.

To get the real picture of how much inventory we have and how it compares to the surplus we saw back then, you’ve got to look at both new homes and existing homes (homes that were lived in by a previous owner).

When you combine those two numbers, it’s clear overall supply looks very different today than it did around the crash (see graph below):

So, saying we’re near 2008 levels for new construction isn’t the same as the inventory surplus we did the last time.

So, saying we’re near 2008 levels for new construction isn’t the same as the inventory surplus we did the last time.

Builders Have Actually Underbuilt for Over a Decade

And here’s some other important perspective you’re not going to get from those headlines. After the 2008 crash, builders slammed on the brakes. For 15 years, they didn’t build enough homes to keep up with demand. That long stretch of underbuilding created a major housing shortage, which we’re still dealing with today.

The graph below uses Census data to show the overbuilding leading up to the crash (in red), and the period of underbuilding that followed (in orange):

Basically, we had more than 15 straight years of underbuilding – and we’re only recently starting to slowly climb out of that hole. But there’s still a long way to go (even with the growth we’ve seen lately). Experts at Realtor.com say it would roughly 7.5 years to build enough homes to close the gap.

Basically, we had more than 15 straight years of underbuilding – and we’re only recently starting to slowly climb out of that hole. But there’s still a long way to go (even with the growth we’ve seen lately). Experts at Realtor.com say it would roughly 7.5 years to build enough homes to close the gap.

Of course, like anything else in real estate, the level of supply and demand is going to vary by market. Some markets may have more homes for sale, some less. But nationally, this isn’t like the last time.

Bottom Line

Just because there are more new homes for sale right now, it doesn’t mean we’re headed for a crash. The data shows today’s overall inventory situation is different.

If you have questions or want to talk about what builders are doing in our area, let’s connect.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice