Is It Better To Buy Now or Wait for Lower Mortgage Rates? Here’s the Tradeoff

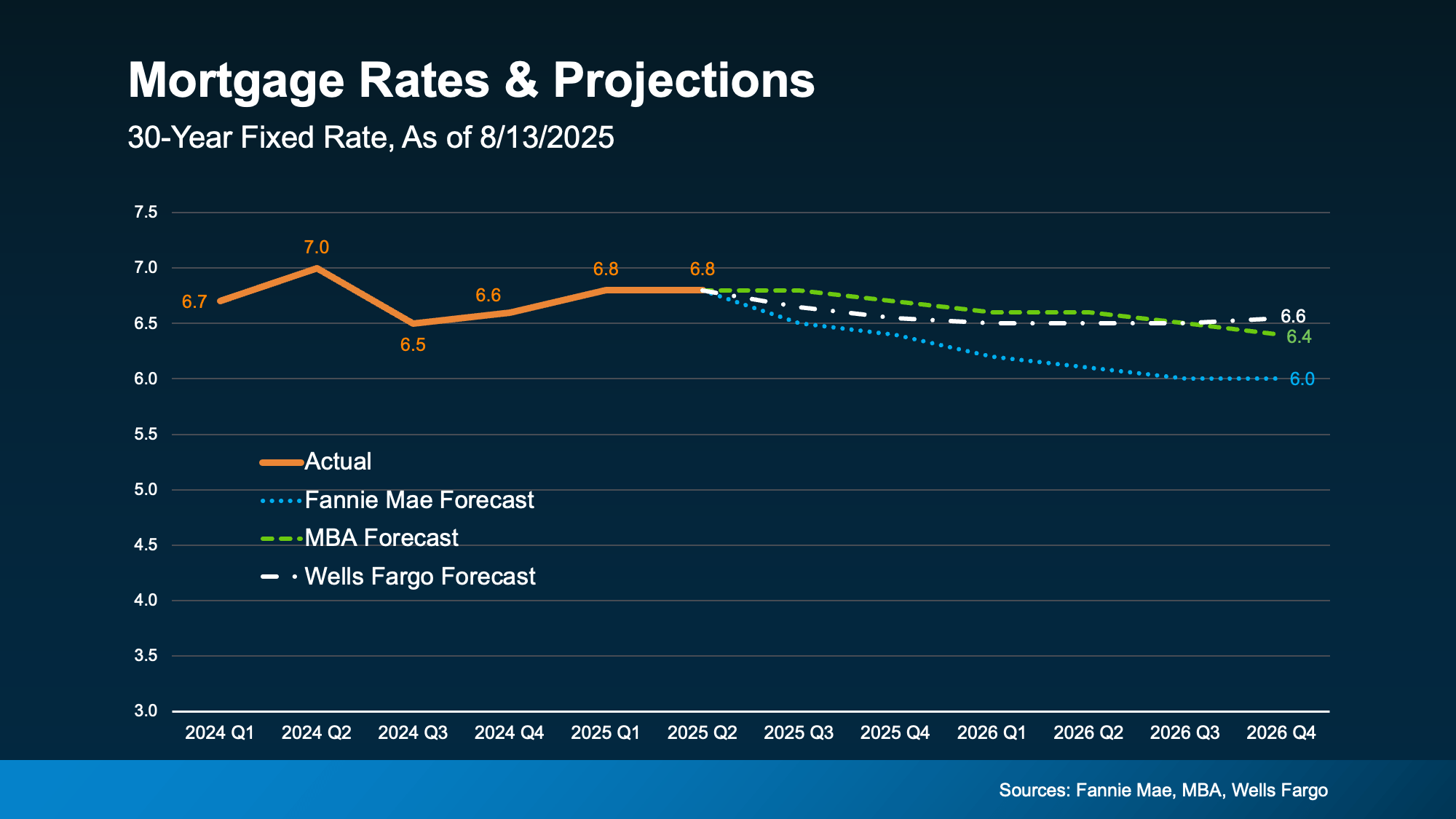

Mortgage rates are still a hot topic – and for good reason. After the most recent jobs report came out weaker than expected, the bond market reacted almost instantly. And, as a result, in early August mortgage rates dropped to their lowest point so far this year (6.55%).

While that may not sound like a big deal, pretty much every buyer has been waiting for rates to fall. And even a seemingly small drop like this reignites the hope we’re finally going to see rates trending down. But what’s realistic to expect?

According to the latest forecasts, rates aren’t expected to fall dramatically anytime soon. Most experts project they’ll stay somewhere in the mid-to-low 6% range through 2026 (see graph below):

In other words, no big changes are expected. But small shifts, like the one we just saw, are still likely.

In other words, no big changes are expected. But small shifts, like the one we just saw, are still likely.

Each time there’s changing economic news, there’s a chance mortgage rates will react. And with so many reports coming out this week, we’ll get a better feeling of where the economy and inflation are headed – and how rates will respond.

What Rate Would Get Buyers Moving Again?

The magic number most buyers seem to be watching for is 6%. And it’s not just a psychological benchmark; it has real impact. A recent report from the National Association of Realtors (NAR) says if rates reach 6%:

- 5.5 million more households could afford the median-priced home

- And roughly 550,000 people would buy a home within 12 to 18 months

That’s a lot of pent-up demand just waiting for the green light. And if you look back at the graph above, you’ll see Fannie Mae thinks we’ll hit that threshold next year. That raises an important question: Does it really make sense to wait for lower rates?

Because here’s the tradeoff. If you’re waiting for 6%, you need to realize a lot of other people are too. And when rates do continue to inch down and more buyers jump into the market all at once, you could face more competition, fewer choices, and higher home prices. NAR explains it like this:

“Home buyers wishing for lower mortgage interest rates may eventually get their wish, but for now, they’ll have to decide whether it’s better to wait or jump into the market.”

Consider the unique window that exists right now:

- Inventory is up = more choices

- Price growth has slowed down = more realistic pricing

- You may have more room to negotiate = you could get a better deal

These are all opportunities that will go away if rates fall and demand surges. That’s why NAR says:

“Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.”

Rates aren’t expected to hit 6% this year. But when they do, you’ll have to deal with more competition as other buyers jump back in. If you want less pressure and more negotiating power, that opportunity is already here – and it might not last for long. It all depends on what happens in the economy next.

Let’s talk about what’s happening in our area and whether it makes sense to make your move now, before everyone else does.

![]()

Is It Better To Buy Now or Wait for Lower Mortgage Rates? Here’s the Tradeoff

The housing market in 2025 is a labyrinth of shifting numbers, market whispers, and big financial decisions. For those pondering whether to leap into homeownership now or bide their time for lower mortgage interest rates, the question isn’t just about timing—it’s about opportunity. The reality is, every tick in the bond market, every dip in a jobs report, and every subtle move in inflation can create ripples that alter the course of the housing market.

In early August, we saw a prime example: a weaker-than-expected jobs report spurred the bond market into action, triggering a notable rate drop—the lowest mortgage rates we’ve seen this year at 6.55%. At first glance, that’s hardly seismic. But in a market where every fraction of a percent impacts affordability, even a small shift can reignite the aspirations of thousands of home buyers.

The Mirage of the Perfect Moment

According to latest forecasts, dramatic plunges in mortgage rates are unlikely in the short term. Many real estate forecasts suggest rates will hover in the mid-to-low 6% range well into 2026. This means the coveted 6% mortgage rate benchmark—the number that so many prospective buyers watch—might still be months, if not a year, away.

Fannie Mae projects this symbolic threshold could be reached next year, sparking what experts call a buyer demand surge. And therein lies the paradox: the very moment buyers believe will be their golden entry point could be the same moment the market becomes more competitive, with home prices escalating and inventory tightening.

The Power and Pressure of 6%

The National Association of Realtors (NAR) offers some illuminating figures. If mortgage rates dip to 6%, approximately 5.5 million more households could afford the median-priced home. Beyond that, roughly 550,000 individuals are expected to buy a home within 12 to 18 months. That’s the definition of pent-up demand—buyers poised on the sidelines, waiting for the starter pistol to fire.

Yet this surge doesn’t only mean bustling open houses. It means heightened competition, dwindling choices, and potential bidding wars. If price growth accelerates alongside this influx of demand, the financial advantage of securing a slightly lower rate may be quickly overshadowed by rising home prices.

Why Waiting Could Be Costly

The allure of lower mortgage rates is undeniable. Lower rates reduce monthly payments and expand purchasing power, boosting affordability. But the decision to wait ignores a critical factor—market opportunities that exist now.

Currently, inventory is higher than it has been in previous cycles, price growth has moderated, and sellers are often more willing to negotiate. This confluence of factors grants today’s buyers significant negotiation power—a rare advantage that may vanish if rates decline and the floodgates of buyer demand surge open.

The Current Advantage in Numbers

In West Palm Beach, for example, local market conditions present a compelling case for action. A West Palm Beach mortgage broker can guide buyers toward the best mortgage rates in West Palm Beach, particularly when partnered with local mortgage lenders in West Palm Beach who understand neighborhood nuances.

For those seeking affordable West Palm Beach home loans, today’s rate climate—though not the lowest—offers stability. By leveraging West Palm Beach mortgage calculators and securing mortgage preapproval in West Palm Beach, buyers position themselves ahead of the competition, ready to act before the inevitable buyer demand surge reshapes the landscape.

Timing, Economics, and the Unseen Variables

Every shift in the economy and inflation feeds into the mortgage rates equation. Economic news—from wage growth to employment statistics—carries weight. A single jobs report can signal either market resilience or vulnerability, influencing investor behavior and bond market yields.

While no one can predict with precision, the interplay of these variables is clear: the longer you wait for that perfect rate drop, the more you expose yourself to external forces—forces that can drive home prices higher or reduce inventory without warning.

Local Insights: The West Palm Beach Perspective

The South Florida real estate environment, particularly West Palm Beach, is dynamic. Demand for both residential and commercial properties remains robust, drawing investors from across the country. Partnering with a commercial mortgage broker in West Palm Beach ensures investors tap into favorable West Palm Beach refinancing options or secure first time home buyer loans in West Palm Beach under optimal terms.

With property loan advice in West Palm Beach, buyers can navigate not only interest rate considerations but also neighborhood-specific growth patterns, zoning changes, and infrastructure developments—factors just as critical as the mortgage rates themselves.

The Tradeoff in Plain Sight

Choosing whether it’s better to buy now or wait isn’t about predicting the lowest possible rate; it’s about understanding tradeoffs. If you move now, you secure:

-

Broader inventory selection

-

Slower price growth

-

More negotiation power

-

Reduced competition

If you wait for the 6% mortgage rate benchmark, you might gain:

-

Slightly improved monthly payment

-

A boost in purchasing power

But you risk:

-

Entering a hotter housing market

-

Facing a buyer demand surge

-

Seeing home prices escalate faster than the savings from the lower rate

Psychological Benchmarks vs. Financial Realities

It’s easy to become fixated on the 6% mortgage rate benchmark. Psychologically, it feels like a gateway to affordability. But the market doesn’t respond to psychology alone—it responds to numbers, supply and demand dynamics, and macroeconomic conditions.

The National Association of Realtors underscores this reality: waiting for lower mortgage rates might give you a win on paper, but in practice, you could be buying into a more expensive, less forgiving market.

Strategic Approaches for Today’s Buyers

Those considering a move in 2025 should think in terms of strategic positioning. Work with a West Palm Beach mortgage broker to identify flexible financing products. Explore West Palm Beach refinancing options that allow for rate adjustments if significant rate drops occur post-purchase.

For first time home buyer loans in West Palm Beach, explore programs that combine competitive rates with down payment assistance. Local mortgage lenders in West Palm Beach often have access to niche products that national banks overlook, particularly for affordable West Palm Beach home loans in emerging neighborhoods.

The Future Is a Moving Target

The path ahead is shaped by more than real estate forecasts. Global events, domestic policy changes, and unforeseen economic shifts all contribute to rate movements. Fannie Mae’s prediction of hitting the 6% mortgage rate benchmark next year is credible, but not immutable.

This unpredictability is why many financial advisors recommend acting when local market conditions are favorable rather than waiting for a national metric to align perfectly.

Conclusion: The Window That Exists Right Now

The decision to buy a home in today’s market is deeply personal, but also inherently strategic. Current market opportunities—from healthier inventory levels to moderated price growth—are tangible advantages that could be gone within months. The risk in waiting is that you exchange these benefits for the uncertainty of a future that might not materialize as expected.

In West Palm Beach, the opportunity is heightened. With the best mortgage rates in West Palm Beach currently accessible, plus the guidance of experienced professionals—from commercial mortgage brokers in West Palm Beach to those offering property loan advice in West Palm Beach—buyers can step forward with confidence. Whether your goal is to lock in affordable West Palm Beach home loans or secure favorable terms through West Palm Beach refinancing options, the foundation you build today can be as valuable as any future rate drop.

The tradeoff is clear: secure your space in the housing market now, while negotiation power and choice are on your side, or gamble on a future where lower mortgage rates might come hand-in-hand with higher prices, tighter supply, and fierce competition.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice