Is the Housing Market Going to Crash? What the Experts Say

Meta Description: Discover why the housing market is not expected to crash, what expert forecasts reveal about home values, and how this impacts buyers or sellers in our local market and nationally.

Introduction

If you’ve seen headlines or social-posts warning of a housing crash, it’s easy to wonder if home prices today are about to plummet. But here’s the truth: the data doesn’t point to a crash — it points to slow, continued growth of home values.

Whether you’re thinking about whether it’s time to buy or sell, what’s going on in the housing market, or how housing market experts view the next few years, this article lays out what the research and expert forecasts say — including insights from Fannie Mae.

So if you’re asking, “Is the housing market going to crash?” or “What are home prices doing now and next?” — keep reading. We’ll break it down in simple terms, offer actionable context for our local market, and help you make informed decisions.

Why Many Fear a Housing Market Crash

It’s understandable that many are worried about a crash in the housing market. The dramatic surge in home prices during the pandemic-era (2020-2022) created elevated expectations — and when things slow, the concern is that a correction might spiral into a crash.

In the mind of many: the saying “What goes up must come down” is applied to home values. Several factors fuel this fear:

-

The memory of the 2008 crash lingers. While the conditions were different, the fear is baked into public perception.

-

Affordability pressures: Elevated mortgage rates, high prices, and tight supply make many feel the market cannot sustain itself.

-

The fact that media headlines love dramatic language — “housing crash,” “price collapse,” “bubble bursts” — adds to the anxiety.

But here’s the key point: while declines in localized markets happen, a broad national crash like 2008 is not what the majority of research and experts are forecasting.

What Experts Are Forecasting for Home Prices

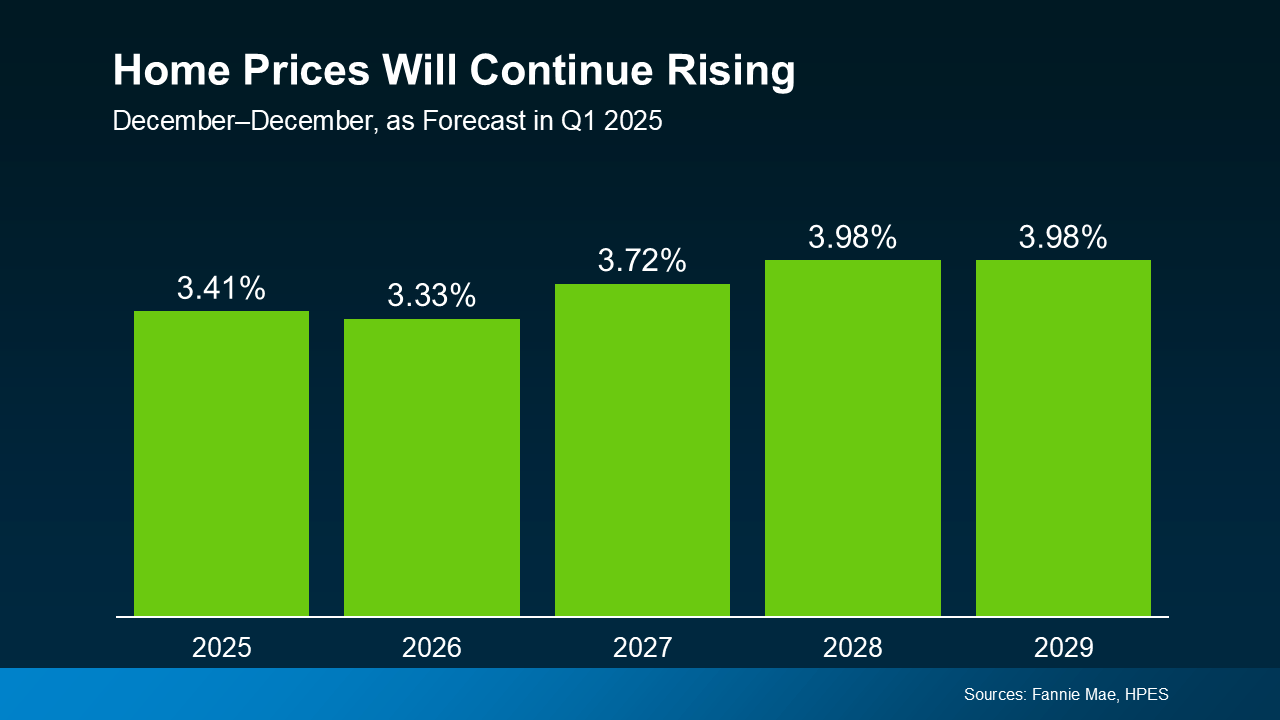

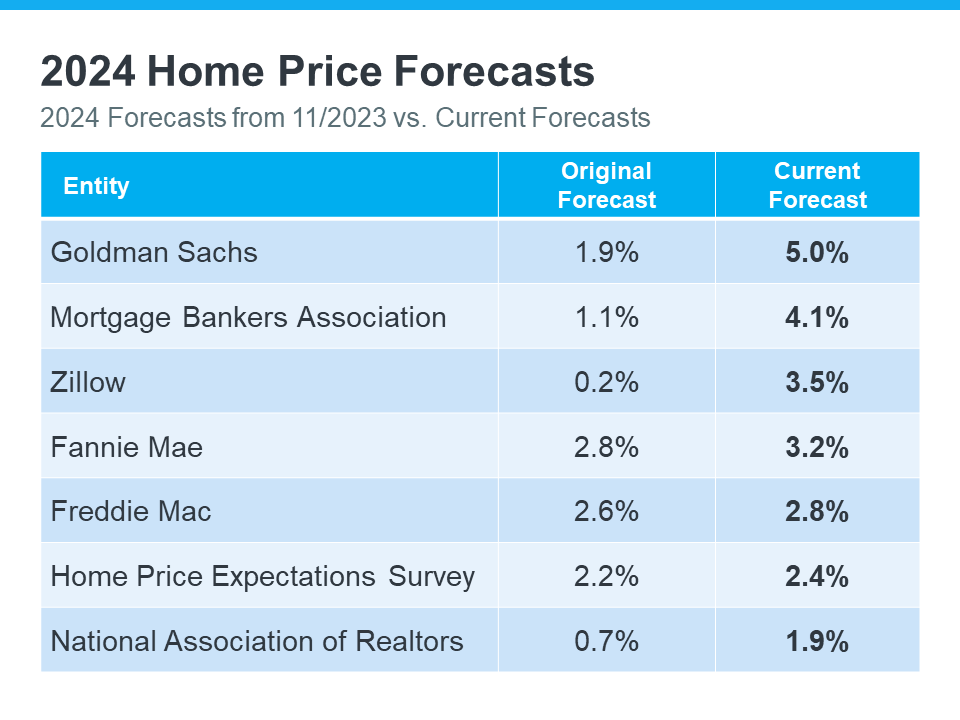

One of the most reliable indicators when trying to answer whether the housing market is about to crash comes from expert-surveys. Enter Fannie Mae’s Home Price Expectations Survey (HPES). This survey polls more than 100 housing and mortgage-market experts to forecast national home price changes. Fannie Mae+2Fannie Mae+2

Key findings

-

According to the Q2 2025 HPES, after a national growth rate of 5.3% in 2024, experts expect national home price growth to average approximately 2.9% in 2025 and 2.8% in 2026. Fannie Mae+1

-

The survey also noted that even in the most pessimistic scenarios, experts did not forecast a major decline in home values. Instead, modest appreciation is expected. Stock Titan+1

-

In earlier quarters, forecasts were slightly higher (e.g., 3.4% for 2025 in Q1 2025) but they have been revised downward — a reflection of moderating growth, not a crash. Fannie Mae+1

What this tells us

-

The fact that the expert panel expects positive growth (not negative) signals that we are not heading into a broad collapse of home values.

-

The moderation of growth (slowing compared to the fast gains of 2020-22) suggests the housing market is shifting into a more sustainable pace of appreciation — rather than the overheated phase that preceded crash-risk environments.

-

Because the forecasts come from many diverse experts, it adds credibility that the consensus is more about “less growth” rather than “big drop.”

How Today’s Growth Forecasts Compare to “Normal”

One of the challenges in interpreting these forecasts is setting the right benchmark. If you heard about double-digit gains in the housing boom years, then a forecast of 2-3% growth might feel like stagnation or decline. But context matters.

Historical baseline

Historically, average annual national home price appreciation has hovered around 4%–5% in the “normal” market environment. During boom years, we may see 8–10% or more; during downturns, we could see declines.

Current forecast vs. historical

-

Experts forecasting ~2.9% for 2025 is below the long-term average, but still positive.

-

This implies that while growth may slow, it is still occurring — which means home values are not expected to fall broadly.

-

It’s a transition from fast growth into steady growth — a more balanced phase.

Why that matters

Understanding this helps goals-setting for both buyers and sellers. If you expect 10%+ annual gains, you’ll be disappointed. But expecting a collapse may leave you sitting on the sidelines unnecessarily. With 2-3% annual gain forecasts, you can plan accordingly.

For example:

-

A homeowner who expects 3% annual appreciation understands the pace is modest — but still meaningful over 5+ years.

-

A buyer who thinks the market will crash may delay forever — potentially missing out on enjoying appreciation and home-ownership benefits.

Why the Housing Market Isn’t Expected to Crash

What’s preventing a crash across the board? Several structural factors point to resilience in the housing market even amid slower growth.

Supply + Demand dynamics

-

While affordability is challenged (high mortgage rates, tight budget constraints), the supply of homes for sale remains relatively low in many markets. A shortage of inventory supports home values.

-

Demand remains present. Many buyers still want to purchase; the question is timing and pricing.

-

Because the “bubble build-up” factors (wild speculation, widespread risky loans) are less prominent than in 2008, the risk of a blanket crash is lower.

Mortgage credit quality & underwriting

-

Unlike the pre‐2008 environment, mortgage credit underwriting standards remain stricter and regulated. This reduces the systemic risk of defaults that triggered the last crash.

-

This facet of the market gives the experts greater confidence that while gains may slow, the whole market is less likely to collapse.

Local market variation & incremental adjustments

-

While the national outlook may forecast ~2-3% growth annually, individual markets will differ. Some might see flat or minor declines (especially those with weak job markets or oversupply).

-

But the national consensus is not for a large downturn. That’s the nuance: national doesn’t mean everywhere.

-

Because many markets are simply returning to more sustainable patterns (rather than crashing), homeowners and buyers can calibrate expectations accordingly.

What This Means for Buyers & Sellers

For anyone in the housing lifecycle — thinking about whether to buy or sell — understanding these forecasts matters. Let’s break it down for both sides.

For Buyers

-

If you’ve been waiting for a crash (thinking you’ll buy when home values fall), you may be undervaluing the chance cost of waiting. With expected ~2-3% annual growth, delaying could mean missing modest but meaningful appreciation.

-

However, you still need to evaluate affordability, mortgage rates, location, and your personal timeline. Just because a crash isn’t forecast doesn’t mean prices will spike—it means stable, measured growth.

-

Use your local context: In our local market, even steadier growth can result in meaningful gains over 3-5 years.

-

For voice-search relevance: People often ask “Is now a good time to buy a house?” or “Will home prices go down?” Being ready, not hesitant, matters.

For Sellers

-

If you were expecting to ride a wave of double-digit appreciation, you may need to recalibrate. The big leaps of 2020-2022 are behind us.

-

But the good news: With no crash expected nationally, you’re less likely to face sharp declines. You can plan your next move with greater confidence in stability.

-

In our local market, this means positioning the property well (location, condition) rather than relying solely on rising tides.

-

Timing matters less when the market is not crashing — but listing strategy, pricing, and marketing still do.

For Investors

-

For investors looking at rental or flip yields, slower growth means fewer speculative upside bets — but also less downside risk.

-

Consider long-term hold strategies rather than short-term flips expecting large price jumps.

-

Focus on local factors (job growth, supply constraints, rental demand) rather than expecting large price corrections.

Local Market Matters — It’s Not Uniform

It’s important to recognize that when we talk about national trends — via Fannie Mae or other expert surveys — we’re dealing with averages. The real story in many cases is what’s happening locally.

Why local variation matters

-

Some metro areas may continue to see above-average growth due to strong job markets, limited new supply, or high migration.

-

Other regions may face flat or slightly negative growth if they have weaker economic fundamentals, oversupply, or high inventory.

-

Your decision to buy or sell should factor in our local market dynamics: how many homes are for sale, what demand looks like, what the job/employer outlook is, what new construction is coming.

Practical steps for local market perspective

-

Connect with a local real estate agent or professional who tracks local price movements, inventory levels, and demand/supply trends.

-

Compare current home prices today locally to national trends — are you ahead, behind, or aligned?

-

Ask: “In this neighborhood, are listings increasing? Are days-on-market going up or down? Are prices stable or shifting?”

-

For buyers and sellers alike, fund your strategy based on local data, not solely national narrative. While the national outlook shows moderate growth, your local result might differ.

Addressing Common Questions (Voice-Search Optimized)

Let’s pull in some of the common questions people ask — especially via voice search — and answer them plainly.

Q: Will the housing market crash soon?

No, the consensus among housing market experts is that a broad national crash is not expected. According to the most recent Fannie Mae Home Price Expectations Survey, the national average appreciation is forecast at ~2.9% for 2025 and ~2.8% for 2026 — positive growth, not negative. Fannie Mae+1

Q: Are home prices today going to fall?

On a national level, no — decline is not the baseline expectation. Some local markets might see stagnation or small dips, but the national outlook is for moderate growth in home values.

Q: Why aren’t home values crashing like in 2008?

Multiple reasons: stricter lending standards, less speculative buying, supply/demand imbalances still favoring sellers in many markets, and mortgage credit quality stronger than pre-2008.

Q: Should I wait to buy until home prices drop?

Waiting for a drop may not be the best strategy. With forecasts showing growth (albeit moderate), you may end up missing value rather than gaining from a drop. Instead, focus on rates, affordability, location, and your personal timeline.

Q: Does this national forecast apply to our local market?

Not fully. National trends provide the backdrop, but local market conditions vary widely. It’s essential to evaluate your specific region — your metro area, neighborhood, and how supply/demand are playing out locally.

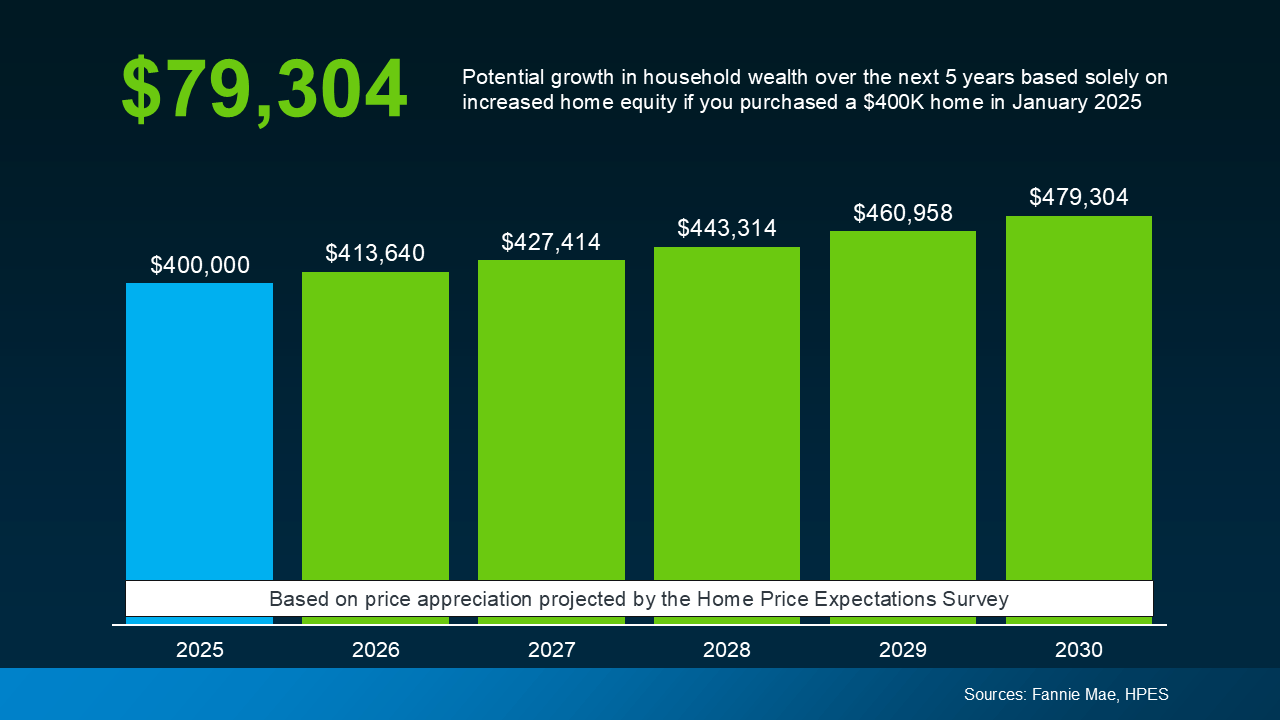

Q: How much might home values increase by 2030?

While long-term forecasts vary, assuming ~2.5% annual growth across five years could translate into roughly 13-15% cumulative growth nationally. Variables will differ greatly by region.

What to Watch in the Months Ahead

Staying informed on key indicators will help you interpret the market — whether you’re buying, selling, or simply holding. Here are top factors to monitor:

-

Mortgage interest rates:

Rates significantly impact affordability and demand. If rates drop, buying demand might pick up — boosting home prices. If rates rise further, it could dampen growth. Fannie Mae’s survey page indicates elevated but gradually moderating rates. Fannie Mae+1 -

Inventory levels (supply):

More homes on the market means more competition and potential for price softening. Less inventory supports price stability or growth. -

Job market and migration trends:

Regions gaining employers, population, and migration may see stronger home price growth. Conversely, regions losing population/employment may lag. -

Local affordability & wage growth:

If wages stagnate while home prices rise (even modestly), local markets may face stagnation or slight declines. -

New construction activity:

Large upticks in new builds can add supply and reduce upward pressure on home values in certain neighborhoods. -

Regulatory or economic shocks:

Although not predicted broadly, unexpected shocks (e.g., major economic slowdown, mortgage crisis) could alter trends quickly.

By paying attention to these signs, you’re not just following headlines — you’re aligning with a data-driven approach in the housing market.

The Bottom Line

So, where does that leave us? If you’ve been waiting for a crash so you can buy a home at a bargain price, you may want to rethink that strategy. The majority of housing market experts, including those surveyed by Fannie Mae, expect moderate growth — not a collapse — in home values over the next few years.

Here’s what to retain:

-

National forecasts point to positive growth, albeit at a slower pace (~2-3% per year) rather than the double-digit gains of recent hot years.

-

A crash — at least at a national level — is not the baseline outcome.

-

Home prices today may seem high compared to historic norms, but the supporting fundamentals (tight supply, willing buyers) make a dramatic drop less likely.

-

Local market conditions matter significantly. Your experience could differ from the national average — always evaluate our local market rather than assuming the national narrative fully applies.

-

Whether you plan to buy or sell, your strategy should be based on realistic expectations, your financial situation, and local data — not fear of a crash or speculation of huge gains.

If you’re considering making a move — buying your first home, selling your current one, or simply monitoring the market — now is the moment to act with informed confidence rather than waiting indefinitely for an ideal scenario that may not arrive.

![]()

Is the Housing Market Going To Crash? Here’s What Experts Say

If you’ve seen headlines or social posts calling for a housing crash, it’s easy to wonder if home values are about to take a hit. But here’s the simple truth.

The data doesn’t point to a crash. It points to slow, continued growth.

And sure, it’s going to vary by local area. Some markets will see prices rise more than others. And some may even see small, short-term declines. But the big picture is: home prices are expected to rise nationally, not fall, over the next 5 years.

The Real Story Is in the Expert Forecasts

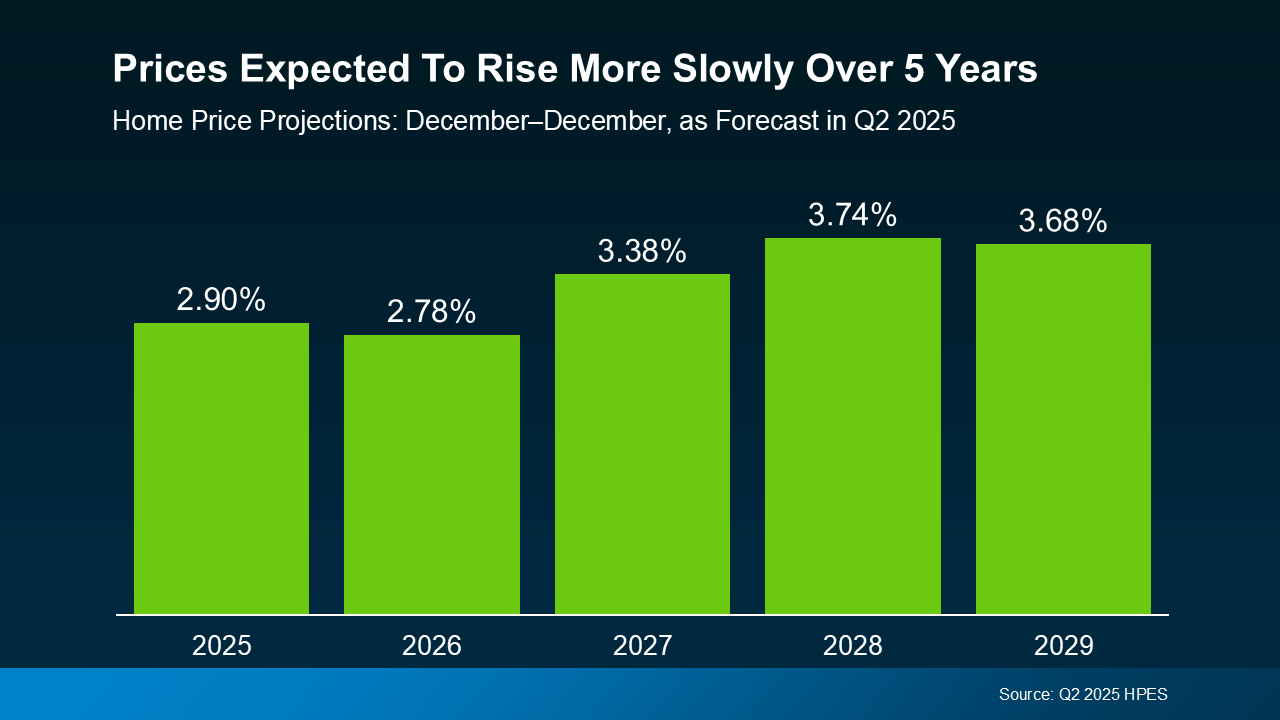

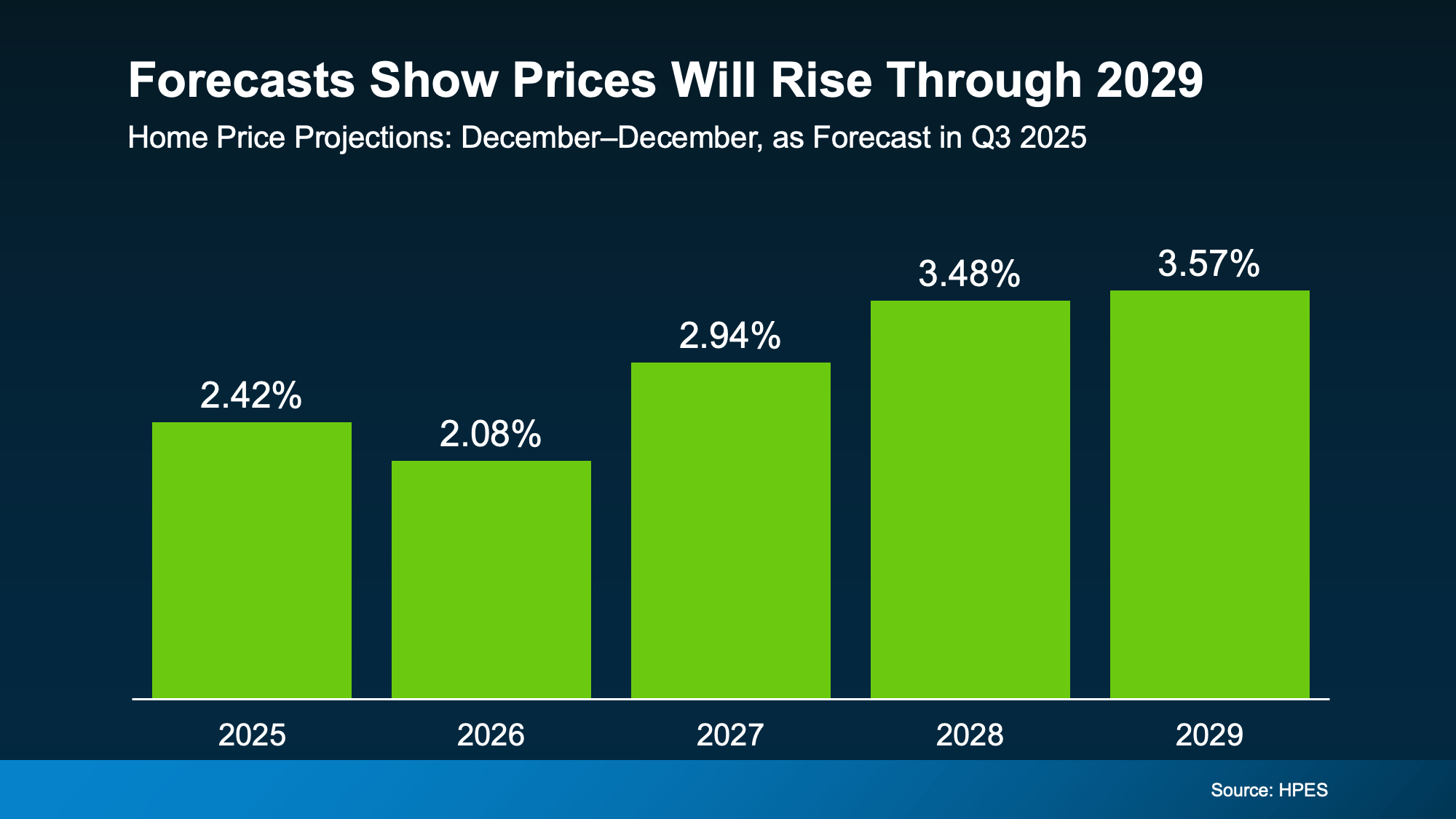

In the Home Price Expectations Survey (HPES) from Fannie Mae, each quarter over 100 leading housing market experts weigh in on where they project home prices will go from here. And in the report that was just released, the experts agree prices are projected to climb nationally through at least 2029 (see graph below):

Here’s how to read this visual. Each bar in that graph shows an increase, not a loss. It’s just that the anticipated pace of that appreciation varies year-to-year.

Here’s how to read this visual. Each bar in that graph shows an increase, not a loss. It’s just that the anticipated pace of that appreciation varies year-to-year.

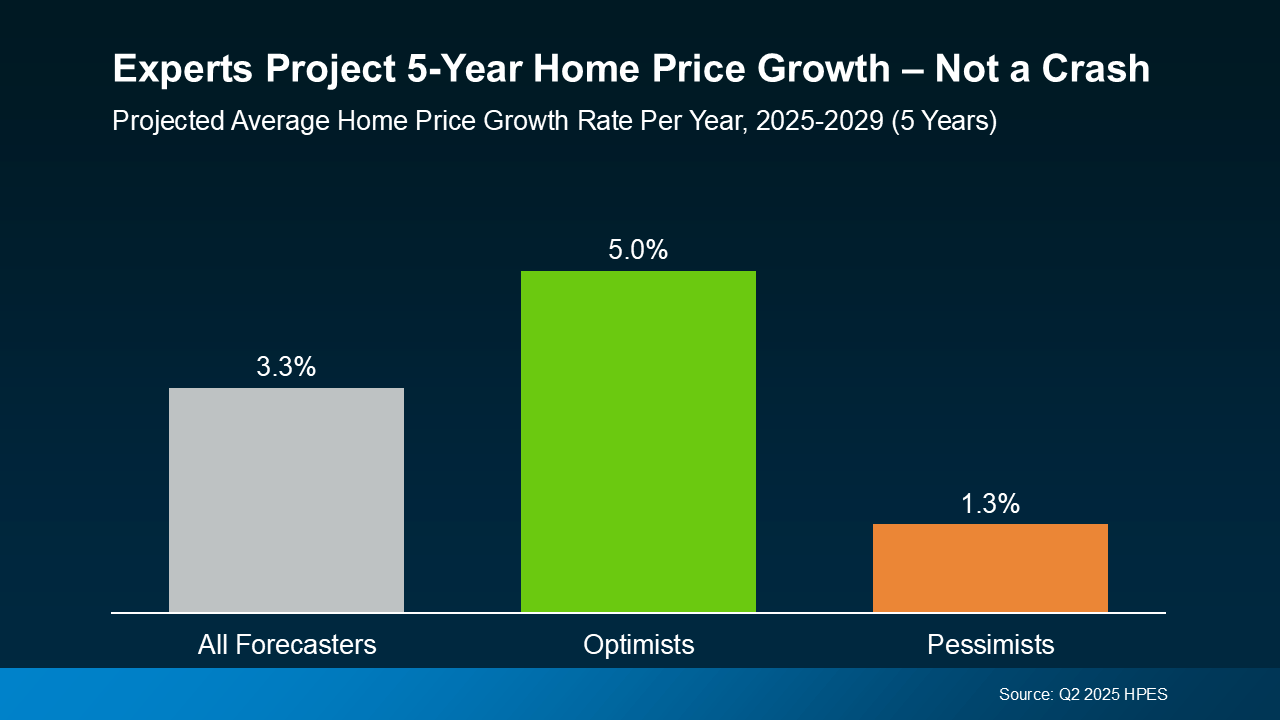

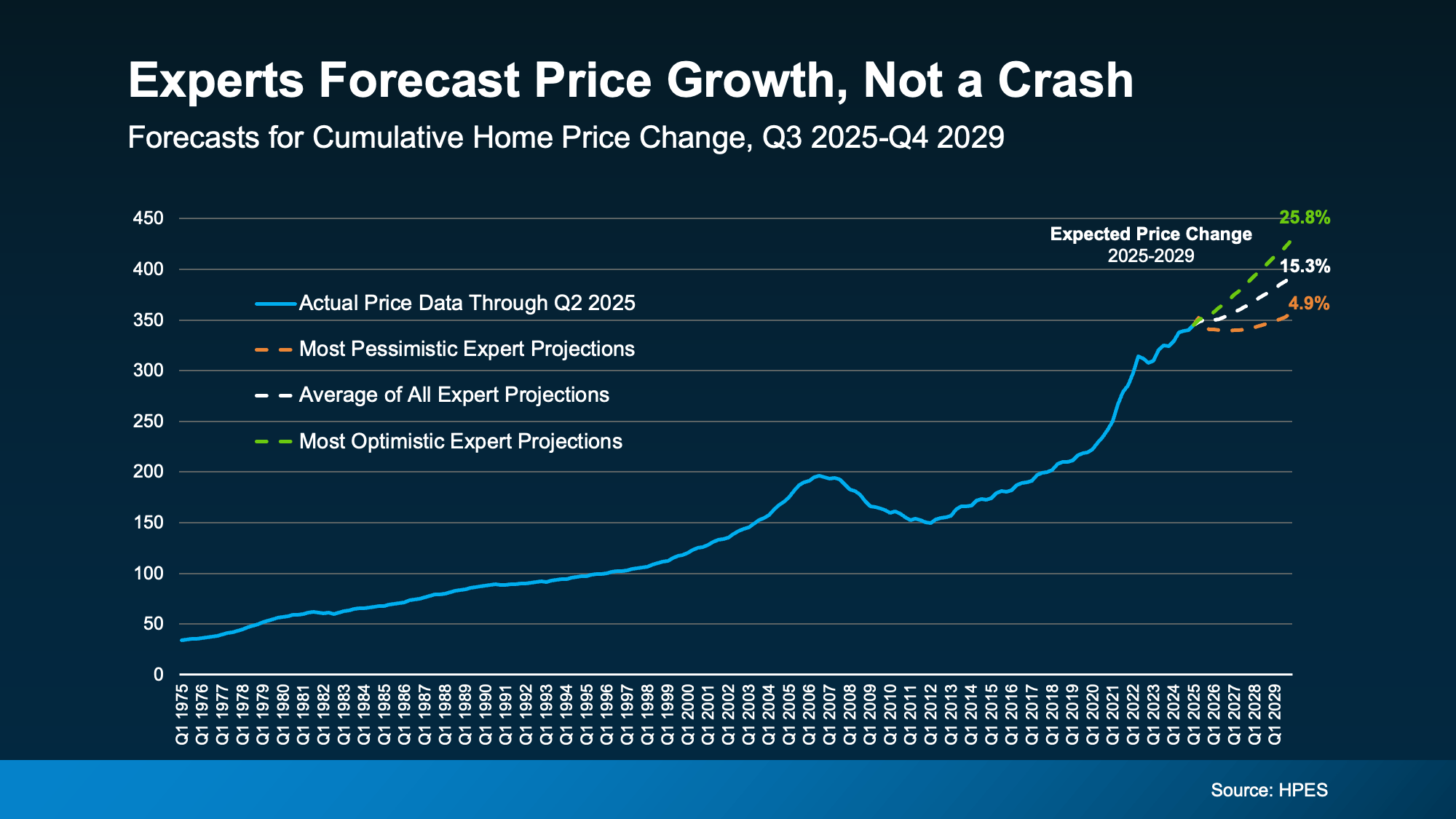

And to further drive this home, let’s look at another view of where prices are and where they’re expected to go. In this version, the expert forecasts are broken into 3 categories: the overall average, the most optimistic projections, and the most pessimistic projections (see chart below):

Notice how even the most pessimistic forecasters say we’ll see prices rise by almost 5% over the next few years.

Notice how even the most pessimistic forecasters say we’ll see prices rise by almost 5% over the next few years.

- Overall, prices are expected to rise about 15% from now through the end of 2029.

- The optimists say we’ll beat that and see a roughly 26% increase.

- And even the pessimists anticipate prices will go up by 5% during that period.

What sticks out the most? None of these groups who study the market are forecasting a crash, or even a decline, over the next 5 years.

How This Compares to “Normal” for the Market

Now, focus back on the first graph. The projections call for 2-3.5% price increases in each of the next five years. For context, the average rate of appreciation for the last 25 years was closer to 4-5% annually.

So, while that’s slightly below the historical average, it’s much more sustainable and typical than where the market was in 2020, 2021, and 2022.

Back then, prices rose too much, too fast based on record-low supply and record-high demand. Some places even saw prices climb by 15-20%.

So, while it may feel like prices are stalling compared to those pandemic-era surges, what’s really happening is that the market is finally finding balance again.

Why Prices Aren’t Expected To Crash

A lot of the chatter about home prices today is based on that rapid rise and the old saying that what goes up, must come down. But historically, that’s not really true. Home prices almost always rise.

And the main reason we’re not heading for a repeat of 2008 is simple: supply and demand.

Even though affordability challenges have made it harder for some people to buy over the past few years, there still aren’t enough homes for everyone who wants one. And that ongoing shortage is keeping upward pressure on prices nationally.

That’s why experts across the board can confidently agree: we’re not headed for a price collapse, but for steady, long-term appreciation.

And just in case it’s the economy that’s got you worried, remember this. Over the past 50 years, there have been plenty of economic events that have impacted the market. And one thing that’s consistently been true throughout time is the housing market always recovers. And we’re coming through that turn right now and going into a recovery.

Bottom Line

If you’ve been waiting to buy or sell because you’re worried about a crash, it’s time to look at the data – not the headlines.

The question isn’t if home prices will rise, it’s by how much.

Let’s connect so you know what’s happening in our local market and what these forecasts mean for your next move.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice