2026 Housing Market Outlook: What Buyers, Sellers & Investors Need to Know

Meta Title: 2026 Housing Market Outlook — Forecasts for Prices, Rates & Sales

Meta Description: Dive into the 2026 housing market forecast: mortgage rate trends, home price growth, sales projections, risks, and how to prepare whether you’re buying or selling.

2026 Housing Market Outlook: What Buyers, Sellers & Investors Need to Know

Over the past few years, the U.S. housing market has felt like it was stuck in a holding pattern — high mortgage rates, affordability constraints, and a “lock-in effect” that discouraged many homeowners from moving. But 2026 is shaping up to be a potential turning point.

In this comprehensive forecast, we’ll explore:

-

What’s driving renewed activity

-

Projections for mortgage rates, home prices, and sales volume

-

Regional variations and risk factors

-

What it means for homebuyers, sellers, and investors

-

Strategic tips to prepare now

Let’s dive in.

Why 2026 Could Be a Turning Year

Pent-Up Demand, Shifting Incentives & Market Psychology

Even in a stagnant market, underlying demand persists. People move for jobs, family, downsizing, upgrading, or lifestyle changes. What’s held many back recently is affordability — particularly high borrowing costs and tight credit.

But signals are emerging that sentiment could shift:

-

Lock-in effect weakening: Many existing homeowners locked in historically low rates (below 5%) have been reluctant to trade up because they’d have to give up that cheap capital. As mortgage rates ease slightly, some may feel the tradeoff is more acceptable.

-

Equity gains: Over recent years, many homeowners have built up equity. That equity cushion can make relocating or upsizing more feasible.

-

Inventory start points: In some markets, inventory has slowly risen. More listings can give buyers more options — fueling optimism.

-

Expectation dynamics: Once buyers and sellers begin to believe things will change, behavior changes — even small shifts in optimism can catalyze movement.

In short: 2026 may not be a boom, but it could be the year momentum returns.

Projected Trends in Home Sales

Rising Transaction Volume

Forecasters generally agree: more homes will change hands in 2026 compared to recent years.

-

Lawrence Yun of the National Association of Realtors (NAR) expects existing home sales to rise 11% in 2026. National Mortgage Professional

-

New home sales are also projected to rise — by ~5% according to some forecasts. National Mortgage Professional

-

Analysts cite that even a modest drop in mortgage rates could free up tens or hundreds of thousands of buyers who were previously priced out. Mortgage Professional Australia+4Barron’s+4Business Insider+4

But don’t expect a meteoric leap — the constraint will continue to be affordability, supply, and macro uncertainties.

Geographic & Segment Variations

Not all markets will rise equally. In fact, where you live (or where you invest) will matter more than ever.

-

Some Sun Belt and high-growth metro areas may see more robust demand.

-

Conversely, markets that have already seen price run-ups or are experiencing supply gluts may lag or even decline.

-

Certain property types — e.g. entry-level homes, condominiums — may outperform luxury tiers in markets where affordability becomes critical.

So while national statistics offer a broad picture, local trends will decide winners and losers.

Mortgage Rate Forecasts & What They Mean

Current Landscape & Recent Moves

As of late 2025, mortgage rates remain elevated:

-

The 30-year fixed rate recently dipped to ~6.3% per Freddie Mac — its lowest in roughly a year. AP News

-

But prior to that, rates had hovered in the mid-6% to high-6% band. Mortgage Professional Australia+3AP News+3Fingerlakes1.com+3

-

Economists caution that even though downward movement is expected, it will likely be gradual, not steep. The Close+3Mortgage Professional Australia+3Fannie Mae+3

In short: rates remain a hurdle, but relief is tentatively on the horizon.

Forecasts Into 2026

We don’t see a return to ultra-low rates (e.g. sub-4%) anytime soon. But many expect mid-6% levels to gradually soften.

-

Fannie Mae now foresees the 30-year fixed mortgage rate ending 2026 around 6.2% (down from their prior estimate of 6.3%). Fannie Mae+2The Street+2

-

Their earlier models had projected 6.0% by end-2026 in some scenarios. Mortgage Professional Australia+1

-

A Reuters survey (of property analysts) expects rates falling to 6.33% in 2026, and 6.29% in 2027. Mortgage Professional Australia

-

Some economists remain cautious, pointing to persistent inflation, bond yields, and global uncertainty as wildcards. Mortgage Professional Australia+3Capital Economics+3Fortune+3

-

Goldman Sachs remains conservative, arguing that rates will stay elevated unless inflation falls decisively. Business Insider

Thus the expected path is a staircase decline — gradual, with intermittent bumps.

Voice-Search Friendly Q&A

“What will the 30-year mortgage rate be in 2026?”

Analysts typically expect ~6.2% by year’s end if inflation moderates and the Fed eases cautiously.

Rate Sensitivity & Behavioral Thresholds

While forecasts matter, what drives behavior is perception:

-

Many prospective buyers say crossing beneath 6.0% would be psychologically meaningful. Mortgage Professional Australia+4Barron’s+4Business Insider+4

-

A 0.5% interest drop, even if moderate on paper, can translate into meaningful monthly savings — enough to move someone from “just out of reach” to “within budget.”

-

In some markets, that threshold shift may trigger a cascade: more listings, more showings, more offers.

But given rate expectations, the timeline for that “breakthrough” may stretch into late 2026 or beyond.

Home Price Forecast & Housing Supply Dynamics

Conflicting Signals & Recent Revisions

Price forecasts have been volatile and frequently downwardly revised:

-

Zillow now expects U.S. home prices to fall ~0.9% between April 2025 and April 2026. ResiClub Analytics

-

Its revised map of 400+ markets shows projected annual declines of –1.0% in many markets. ResiClub Analytics

-

Because affordability is tightening and active listings are rising, Zillow economists argue upward pressure is muted. ResiClub Analytics+2ResiClub Analytics+2

-

That said, some local metros (especially in the Northeast and parts of the Midwest) may see modest gains if supply remains constrained. ResiClub Analytics+2ResiClub Analytics+2

These conflicting signs underscore the difficulty in national forecasts. Local supply, demand, and sentiment will matter more than ever.

National Models & Expectations

Despite Zillow’s caution, broader surveys still expect modest growth:

-

Reuters surveyed 27 property analysts, who forecast ~3.5% annual gains through 2027. Reuters

-

In that same Reuters poll, analysts see rates easing to 6.33% in 2026 and 6.29% in 2027 — supporting modest price growth. Mortgage Professional Australia

-

Some economists maintain that prices will continue upward — albeit slowly — because supply isn’t catching up. Capital Economics+2The Close+2

-

NAR’s forecasts anticipate ~4% median home price appreciation in 2026. NAR Realtor+2The Close+2

-

The Close cites Fannie Mae’s view that the 30-year fixed rate might settle at ~6.2% in 2026, enabling some upward pressure on prices. The Close

In sum, many believe moderate price growth is likely, unless macro or supply constraints intervene.

Inventory, Construction & Supply Constraints

One of the biggest wildcards remains housing supply:

-

Inventory levels nationwide remain well below pre-pandemic norms in many markets — meaning demand will hit a persistent ceiling unless more homes are built. Capital Economics+2Reuters+2

-

Construction and labor costs, permitting bottlenecks, land constraints, and material shortages still hamper robust new home growth. Reuters+2Capital Economics+2

-

Tariffs, supply chain disruptions, and regulatory burdens could further slow building momentum. Reuters+1

-

Because many segments (especially entry-level) have been undersupplied, those segments may outperform more saturated tiers.

Hence, unless supply constraints ease, even modest demand increases may push prices upward in some markets.

Risks, Wildcards & Downside Scenarios

No forecast is foolproof. Here are key risk factors that could disrupt even the best-laid projections:

Persistent Inflation & Fed Reaction

-

If inflation refuses to fall, the Fed may delay rate cuts or even increase rates — reversing mortgage relief. Capital Economics+2Fortune+2

-

Bond yields (particularly 10-year Treasury) are a forcing function for mortgage rates; volatility in global markets could push yields upward.

-

Unforeseen economic shocks (energy price spikes, supply chain crises, geopolitical tensions) could reignite inflation pressures.

Economic Growth Slowing / Recession Risks

-

If GDP growth slows more than expected, it could weaken buyer confidence, increase unemployment, and depress housing demand.

-

Credit standards could tighten, pulling marginal buyers out of the race.

-

Some forecasts remain cautious about the pace of broader economic recovery. Capital Economics+1

Local Market Imbalances & Overcorrection

-

Some overbuilt, slower-growth, or high-debt markets may face steeper corrections.

-

Luxury or speculative segments may underperform if borrowing costs rise again.

-

Regions reliant on a single industry (e.g. energy, manufacturing) may see outsized swings.

Policy, Tax, & Regulation Shifts

-

Changes in tax law (e.g. property tax, mortgage deductibility) or housing regulation could shift incentives.

-

Subsidies, land use policy, zoning shifts, or incentives for affordable housing could materially affect supply/demand.

-

A government shutdown or federal program disruption (e.g. flood insurance, mortgage guarantees) could slow closings or raise uncertainty. Reuters

In short — the path to 2026 is not linear. Many moving parts could push projections off course.

What It Means for Buyers, Sellers & Investors

For Homebuyers

-

Be prepared now

-

Get your finances in order (credit score, down payment, debt reduction)

-

Monitor rate trends and lock when you see value

-

Have your must-haves vs. nice-to-haves clearly ranked

-

-

Time and patience matter

-

A drop from 6.5% → 6.2% may not seem huge, but on a $300,000 loan it can reduce payments by $50–$100+ monthly.

-

In many markets, more listings and less frenzied competition could give buyers more negotiating power.

-

-

Focus on resilient markets

-

Look for metros with growing jobs, population influx, supply constraints.

-

Consider value in fringe areas or secondary markets that may see spillover demand.

-

-

Use flexibility to your advantage

-

Build in buffer for interest rate shifts

-

Be open to alternatives (e.g. adjustable-rate mortgages, longer term horizons)

-

Voice-Search Friendly Q&A

“Should I wait until 2026 to buy a home?”

If you can afford now and rates are acceptable, waiting may not yield much additional upside. But if you’re flexible, waiting for modest rate relief and more inventory in 2026 could give you better options.

For Sellers

-

Get ahead of rising inventory

-

As more homeowners decide to list in 2026, competition will increase.

-

Move now while supply is still constrained.

-

-

Price carefully

-

Overpricing is riskier in an era of cautious buyers — being too aggressive may lead to stale listings.

-

Use comps, agent insights, and be realistic.

-

-

Stage, improve, and present well

-

In markets where buyers have options, presentation and differentiation matter.

-

Invest in repairs, staging, and curb appeal.

-

-

Time your listing window

-

Spring and early summer tend to remain strong listing seasons.

-

Monitor mortgage rate announcements — listing when rates dip (or after a positive signal) may yield stronger interest.

-

For Investors & Long-Term Players

-

Focus on rental demand & yield buffer

-

If homeownership becomes harder for buyers, rental demand may stay strong, especially in younger demographic zones.

-

Look at markets with strong employment and limited supply.

-

-

Layer in optionality

-

Consider value-add opportunities (renovations, subdividing, accessory units)

-

Stretch horizons — exit timing flexibility is helpful.

-

-

Diversify geographically

-

Don’t bet solely on overheated metros.

-

-

Watch macro cues closely

-

Interest rates, cap rates, supply pipelines, credit conditions matter heavily for real estate returns.

-

Regional & Metro-Level Caveats

Because national forecasts mask local disparities, here’s how to think at a more granular level:

-

Sun Belt & Southeast metros: likely to see stronger demand if job, population growth hold — but some overbuilding risk.

-

Rust Belt & slower growth markets: weaker performance possible if stagnant wages, outmigration, or local industry struggles.

-

High-cost metros (Bay Area, NYC, San Francisco, etc.): Price sensitivity is greater; affordability constraints stronger.

-

Secondary & tertiary markets: may become more appealing as buyers look for value or escape dense markets.

For example, Zillow’s maps show many southern Louisiana, parts of Texas, and coastal metro areas facing projected price declines, while smaller Northeast or Midwest metros may hold firmer. ResiClub Analytics+1

Another variable: migration flows. If remote work trends persist, buyers may continue relocating to lower-cost regions. That inflow could accelerate growth in “new growth corridors.”

Illustrative Scenarios: Base, Upside & Downside

To ground expectations, here are possible paths:

| Scenario | 30-Year Rate Estimate | Home Price Growth | Sales Volume | Notes |

|---|---|---|---|---|

| Base | ~6.2% by end 2026 | +1–3% nationally | +8–12% | Steady but cautious return |

| Upside | ~5.8–6.0% | +3–5% | +12–18% | Inflation eases faster, Fed cuts earlier |

| Downside | ~6.5%+ | 0% to slight decline | Flat or down | Inflation sticks, economic headwinds |

These are illustrative; the actual path may mix elements from each.

Strategic Takeaways & How to Prepare Now

For Buyers & Would-Be Homeowners

-

Lock when you see a deal — waiting too long may mean losing favorable rates

-

Build flexibility — choose options that allow for refinance or conversion

-

Be selective in markets — look for places with good fundamentals, not just hype

-

Plan for rate buffers — don’t overextend yourself

For Sellers

-

Act ahead of peak inventory — list before too many others flood the market

-

Optimize presentation & pricing — don’t rely on frenzied bidding wars

-

Stage for comparisons — buyers will be more discerning

-

Consider incremental improvements — small upgrades can pay outsized returns

For Investors & Developers

-

Monitor cost curves — building costs, regulatory risk, financing spreads

-

Use conservative underwriting — assume mild growth rather than booms

-

Leverage niche demand — affordable housing, multi-family, adaptive reuse

-

Stay nimble — shift between hold/sell, markets, asset types as data evolves

For Lenders & Mortgage Players

-

Offer flexibility — lower initial rates, adjustable products, incentive packages

-

Educate buyers — help people understand the impact of small interest shifts

-

Watch credit tightening — navigate which buyers remain viable in shifting conditions

Conclusion: Is 2026 Your Year?

2026 is unlikely to be a blockbuster rebound — but it may well be the year the housing market unsticks. With a modest easing in rates, some growth in sales, and continued supply constraints, opportunities will emerge for buyers, sellers, and investors who are alert, flexible, and prepared.

If you’ve been waiting for a window, this could be it — but the key will be timing, local insight, and being ready to act when conditions align.

![]()

2026 Housing Market Outlook

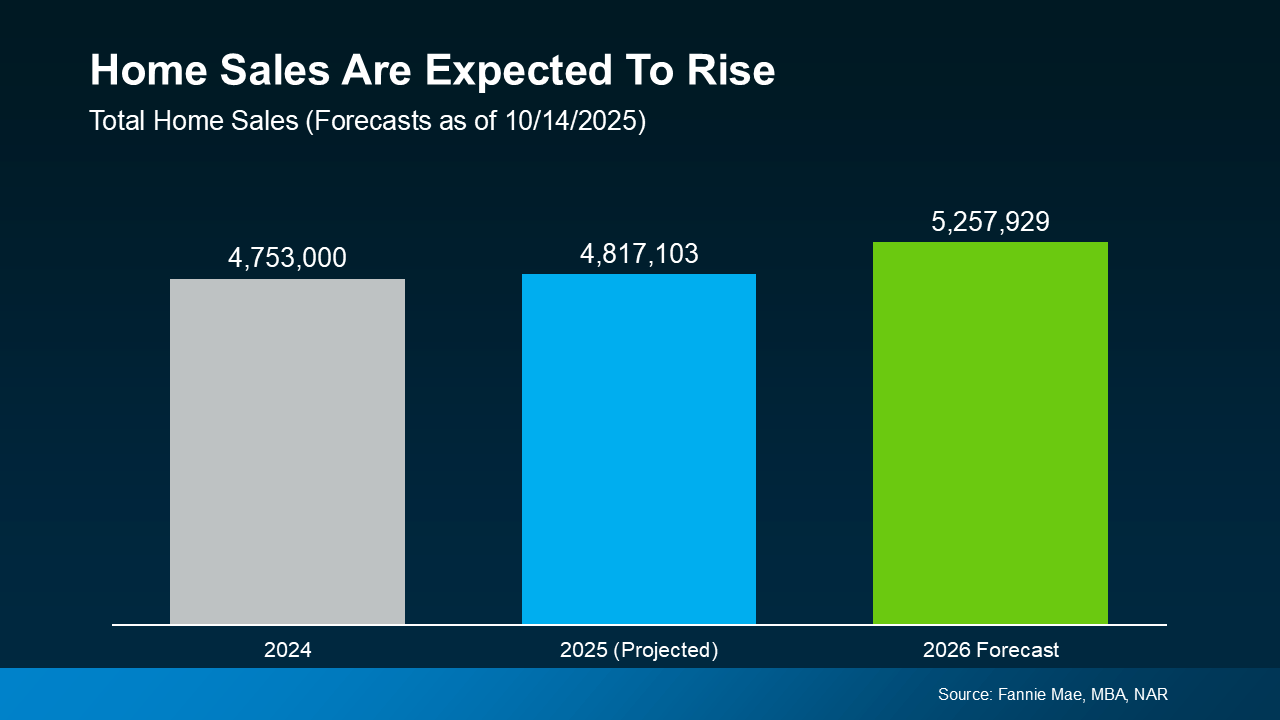

After a couple of years where the housing market felt stuck in neutral, 2026 may be the year things shift back into gear. Expert forecasts show more people are expected to move – and that could open the door for you to do the same.

More Homes Will Sell

With all of the affordability challenges at play over the past few years, many would-be movers pressed pause. But that pause button isn’t going to last forever. There are always people who need to move. And experts think more of them will start to act in 2026 (see graph below):

What’s behind the change? Two key factors: mortgage rates and home prices. Let’s dive into the latest expert forecasts for both, so you can see why more people are expected to move next year.

What’s behind the change? Two key factors: mortgage rates and home prices. Let’s dive into the latest expert forecasts for both, so you can see why more people are expected to move next year.

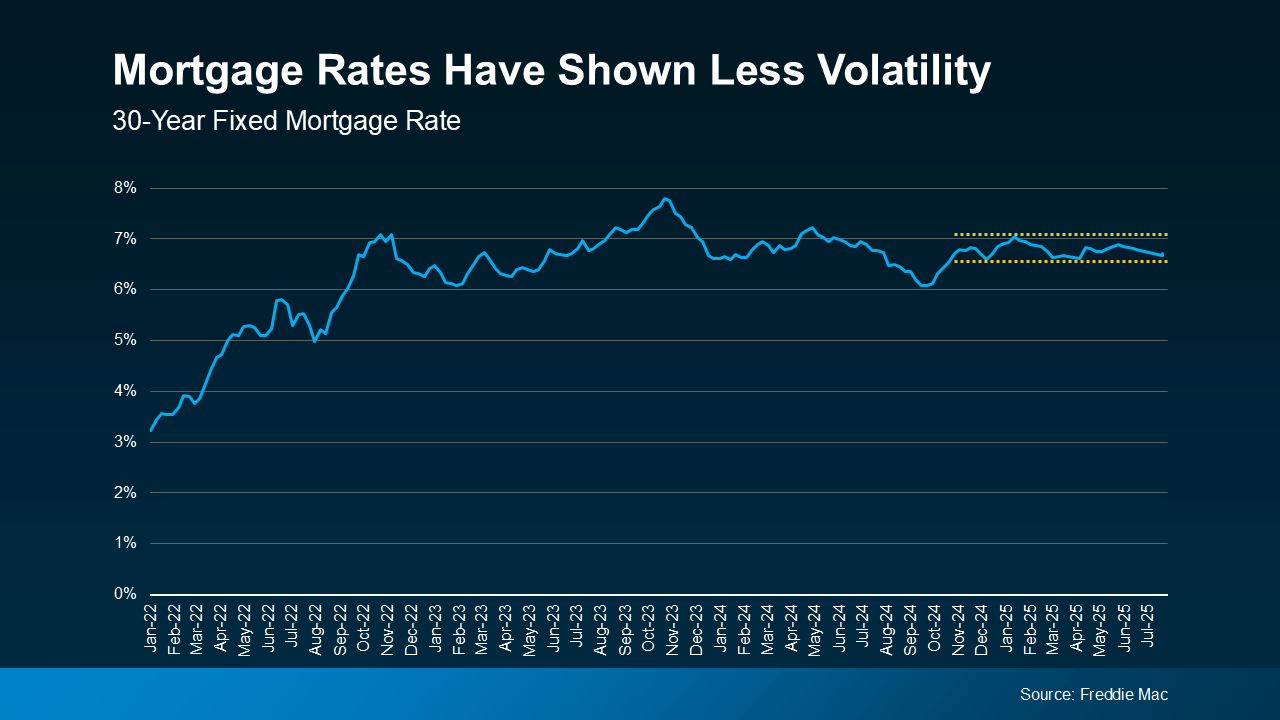

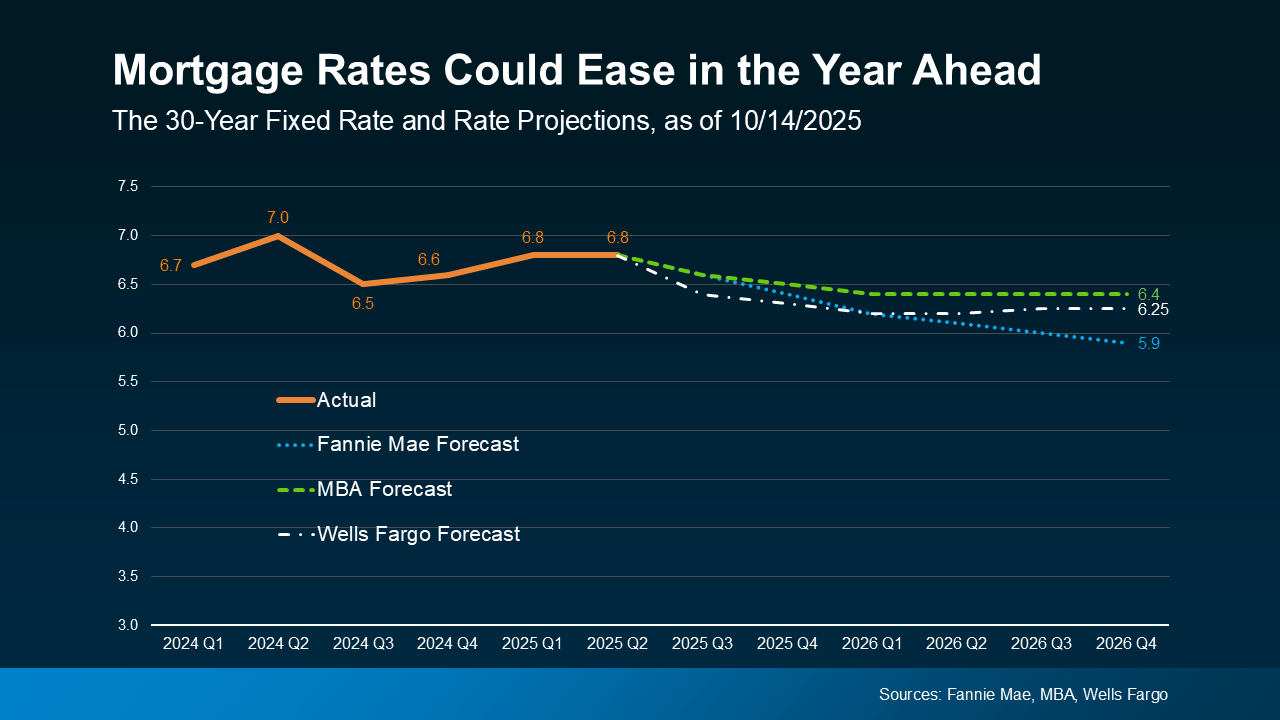

Mortgage Rates Could Continue To Ease

The #1 thing just about every buyer has been looking for is lower mortgage rates. And after peaking near 7% earlier this year, rates have started to ease.

The latest forecasts show that could continue throughout 2026, but it won’t be a straight line down (see graph below):

There’s a saying: when rates go up, they take the escalator. But when they come down, they take the stairs. And that’s an important thing to remember. It’ll be a slow and bumpy process.

There’s a saying: when rates go up, they take the escalator. But when they come down, they take the stairs. And that’s an important thing to remember. It’ll be a slow and bumpy process.

Expect modest improvement in mortgage rates over the next year but be ready for some volatility. There will be volatility along the way as new economic data comes out. Just don’t let it distract you from the bigger picture: the overall trend will be a slight decline. Forecasts say we could hit the low 6s, or maybe even the high 5s.

And remember, there doesn’t have to be a big drop for you to feel a change. Even a smaller dip helps your bottom line.

If you compare where rates are now to when they were at 7% earlier this year, you’re already saving hundreds on your future mortgage payment. And that’s a really good thing. It’s enough to make a real difference in affordability for some buyers.

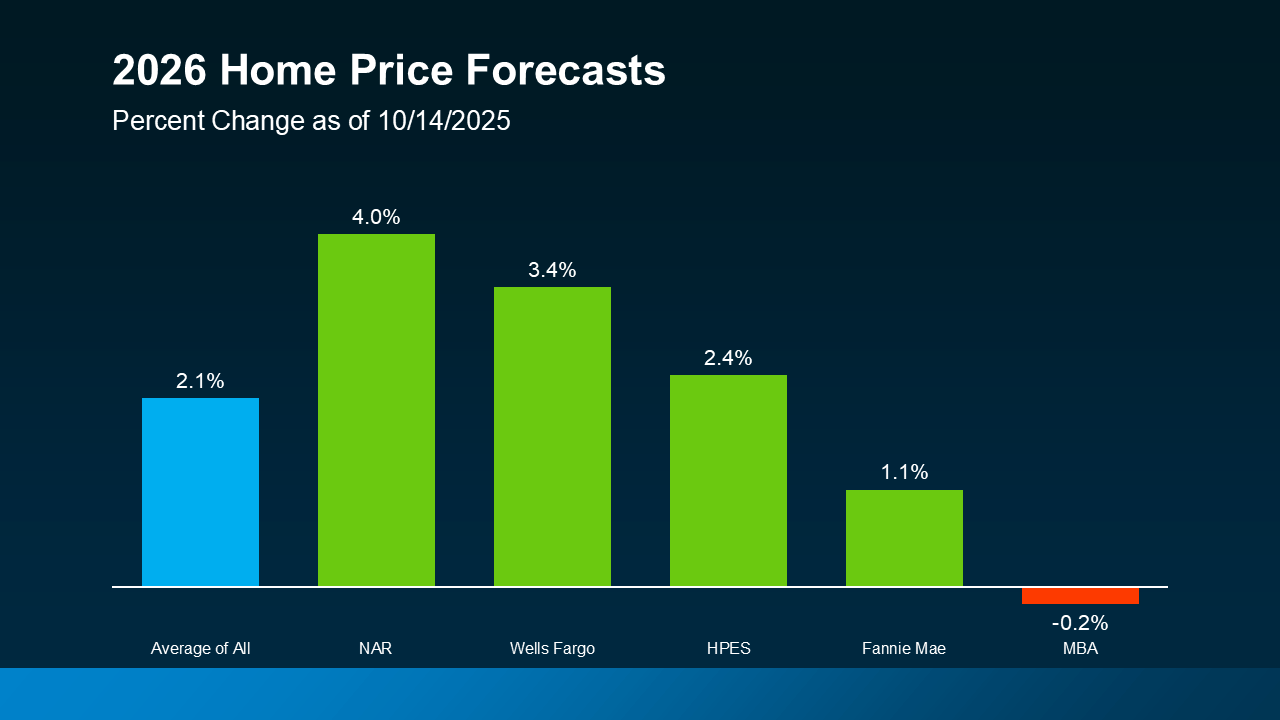

Home Price Growth Will Be Moderate

What about prices? On a national scale, forecasts say they’re still going to rise, just not by a lot. With rates down from their peak earlier this year, more buyers will re-enter the market. And that increased demand will keep some upward pressure on prices nationally – and prevent prices from tumbling down.

So, even though some markets are already seeing slight price declines, you can rest easy that a big crash just isn’t in the cards. Thanks to how much prices rose over the last 5 years, even the markets seeing declines right now are still up compared to just a few years ago.

Of course, price trends will depend on where you are and what’s happening in your local market. Inventory is a big driver in why some places are going to see varying levels of appreciation going forward. But experts agree we’ll see prices grow at the national level (see graph below):

This is yet another good sign for buyers and overall affordability. While prices will still go up nationally, it’ll be at a much more sustainable pace. And that predictability makes it easier to plan your budget. It also gives you peace of mind that prices won’t suddenly skyrocket overnight.

This is yet another good sign for buyers and overall affordability. While prices will still go up nationally, it’ll be at a much more sustainable pace. And that predictability makes it easier to plan your budget. It also gives you peace of mind that prices won’t suddenly skyrocket overnight.

Bottom Line

After a quieter couple of years, 2026 is expected to bring more movement – and more opportunity. With sales projected to rise, mortgage rates trending lower, and price growth slowing down, the stage is set for a healthier, more active market.

So, the big question: will you be one of the movers making 2026 your year?

Let’s connect if you want to get ready.

Read from source: “Click Me”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice