What Most Veterans Don’t Know About Their VA Home Loan Benefit in West Palm Beach, North Palm Beach, Wellington, Florida FL

For many Veterans, active-duty military members, and qualifying reservists, the dream of homeownership can feel farther away than ever. Rising home prices, increasing interest rates, and the misconception that buying a home requires a massive upfront investment have discouraged thousands of military families from taking the next step.

But here’s the truth: many Veterans in West Palm Beach, North Palm Beach, Wellington, and throughout Florida FL are far closer to owning a home than they realize.

According to a recent survey from NewDay USA, nearly half of all Veterans believe homeownership is currently out of reach. However, many of those same Veterans may already qualify for one of the most powerful mortgage benefits available in America — the VA home loan benefit.

The VA loan program, backed by the U.S. Department of Veterans Affairs, has helped millions of Veterans and military families purchase homes for more than 80 years. Yet despite its long history, many people still misunderstand what the benefit actually covers.

That misunderstanding could cost military families thousands of dollars and delay their path to becoming homeowners.

If you are a Veteran, active-duty service member, or military family living in West Palm Beach, North Palm Beach, Wellington, or nearby areas in Florida FL, this guide will help you understand how the VA home loan program really works and why it may be one of the best mortgage options available today.

Working with a trusted professional like Christian Penner, Mortgage Broker, Mortgage Lender, Real Estate Agent, and Real Estate Advisor at America’s Mortgage Solutions (AMS) can help simplify the process and uncover opportunities you may not even know exist.

The Biggest Misconceptions About VA Home Loans

Many Veterans incorrectly assume:

-

They need a large down payment

-

They need perfect credit

-

They cannot afford monthly mortgage costs

-

They must pay expensive mortgage insurance

-

The qualification process is too difficult

-

VA loans are only for first-time homebuyers

These misconceptions often prevent qualified Veterans from exploring their options.

In reality, the VA loan benefit was specifically designed to make homeownership easier and more affordable for military families.

For Veterans relocating to West Palm Beach, retiring in Wellington, purchasing a waterfront property near North Palm Beach, or investing in a permanent residence in Florida FL, understanding these benefits could completely change their financial future.

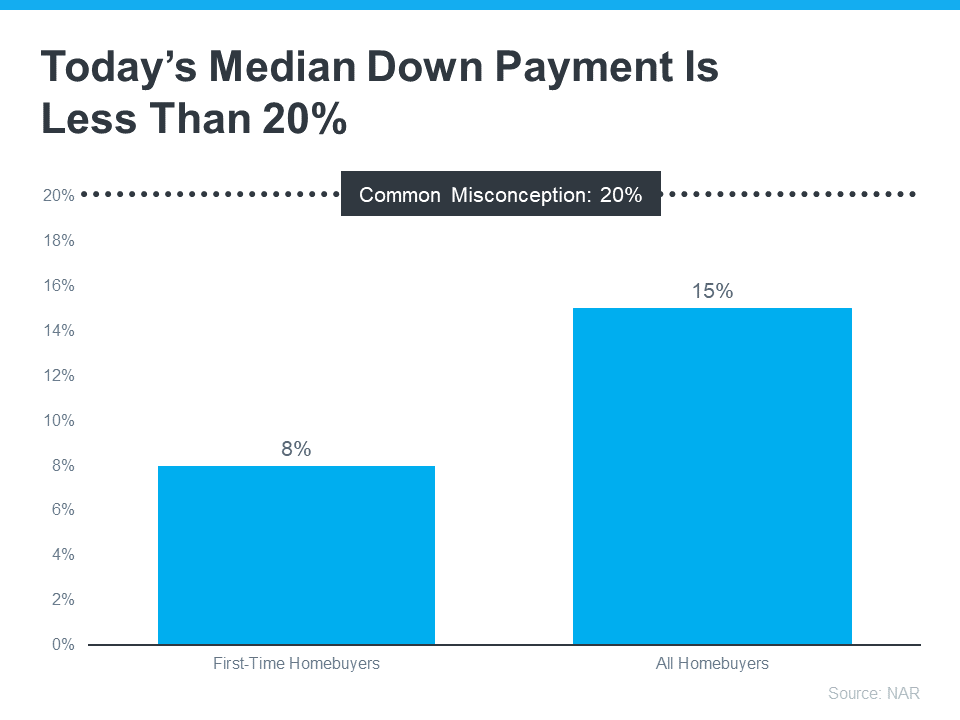

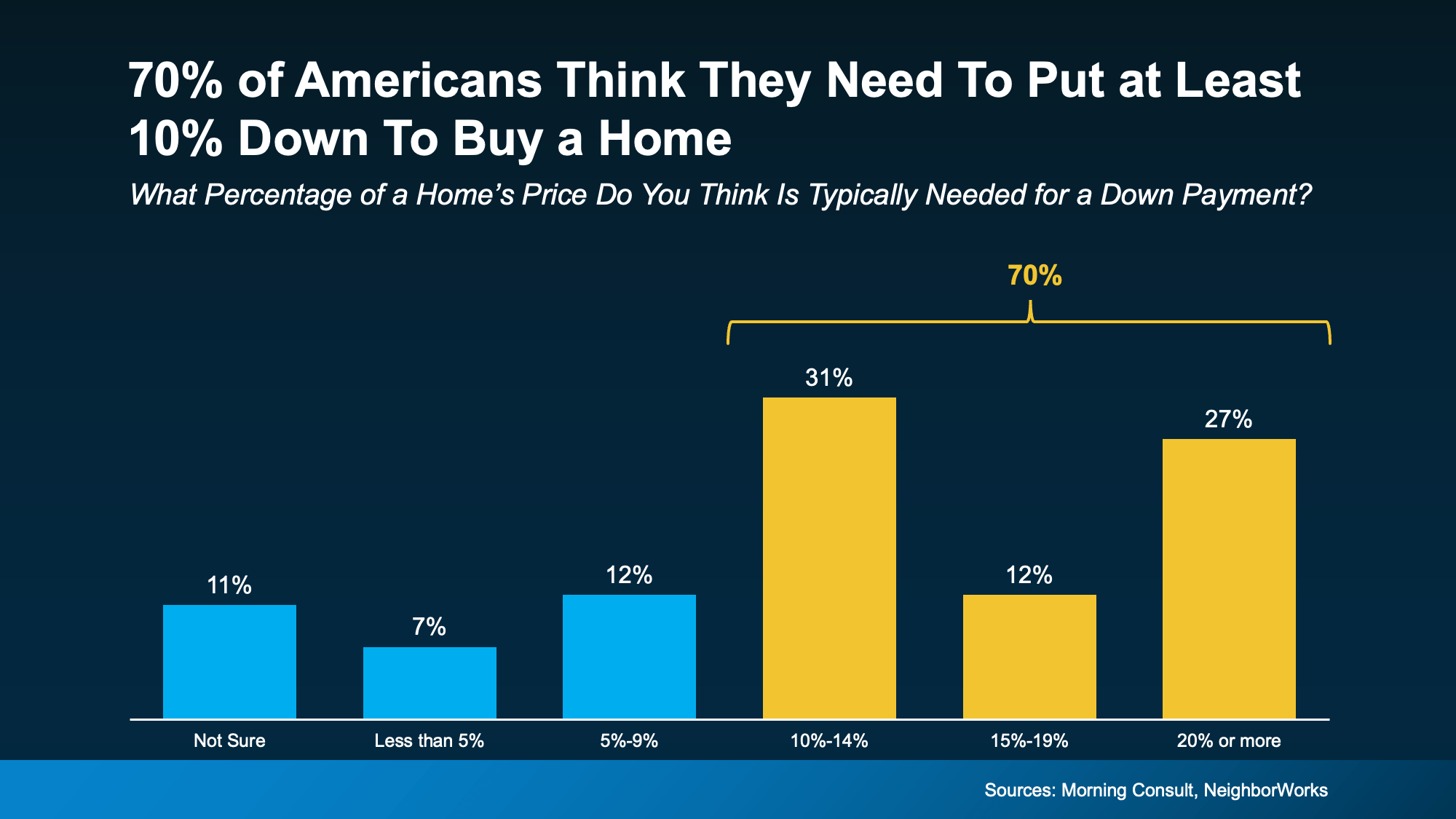

You May Not Need a Down Payment

One of the Biggest Advantages of a VA Home Loan

One of the most powerful benefits of a VA home loan is the ability to purchase a home with zero down payment.

That’s right.

Unlike many conventional mortgage programs that may require 5%, 10%, or even 20% down, qualified Veterans can often buy a home without putting any money down upfront.

For military families trying to save while balancing everyday expenses, childcare, relocation costs, and inflation, this benefit can be life-changing.

Why This Matters in Florida FL

In competitive housing markets like West Palm Beach, North Palm Beach, and Wellington, saving for a large down payment can take years.

For example:

-

A 10% down payment on a $500,000 home equals $50,000

-

A 20% down payment on the same home equals $100,000

That amount alone can prevent many families from entering the housing market.

However, with a VA loan, eligible buyers may be able to finance 100% of the home purchase price.

This means Veterans may be able to purchase a home sooner rather than waiting years to save enough money.

Local Housing Opportunities

Military families are increasingly moving to Florida FL because of:

-

No state income tax

-

Strong Veteran communities

-

Warm climate

-

Expanding job opportunities

-

Excellent schools

-

Retirement-friendly benefits

-

Coastal lifestyle opportunities

Areas like West Palm Beach, North Palm Beach, and Wellington continue to attract Veterans seeking a higher quality of life.

By using a VA mortgage, buyers may gain faster access to these communities without needing a large cash reserve.

VA Loans Often Have Lower Closing Costs

How Veterans Save More at Closing

Another major advantage of the VA home loan program is reduced closing costs.

Closing costs typically include:

-

Loan origination fees

-

Title charges

-

Appraisal fees

-

Recording fees

-

Underwriting costs

-

Inspection-related expenses

With conventional financing, these expenses can quickly add up.

The Department of Veterans Affairs places limits on certain fees lenders can charge Veterans. This protection helps reduce upfront costs and makes homeownership more affordable.

Why Lower Closing Costs Matter

Lower closing costs can help buyers:

-

Preserve emergency savings

-

Afford moving expenses

-

Buy furniture and appliances

-

Reduce financial stress after closing

-

Enter the housing market sooner

For Veterans purchasing homes in West Palm Beach, North Palm Beach, or Wellington, saving money upfront can make a major difference.

This is especially important in today’s competitive Florida FL real estate market, where affordability remains a concern for many buyers.

How Christian Penner Helps Veterans Navigate Costs

Working with a knowledgeable professional like Christian Penner at America’s Mortgage Solutions (AMS) helps Veterans better understand:

-

Estimated closing costs

-

VA loan limits

-

Available financing strategies

-

Monthly payment structures

-

Interest rate options

Having an experienced Mortgage Broker and Mortgage Lender can help eliminate confusion and reduce costly mistakes.

VA Loans Typically Do Not Require PMI

What Is PMI?

Private Mortgage Insurance (PMI) is an additional monthly fee many conventional loan borrowers must pay when they put down less than 20%.

PMI protects the lender — not the buyer.

Depending on the loan size, PMI can cost homeowners anywhere from $100 to $300 or more each month.

Over time, that adds up to thousands of dollars.

Why Veterans Benefit

One of the biggest financial advantages of a VA home loan is that qualified borrowers generally do not need to pay PMI.

Even with little or no down payment.

That means Veterans can often enjoy:

-

Increased purchasing power

-

More affordable long-term homeownership

-

Better monthly cash flow

Example of Monthly Savings

Imagine two buyers purchasing a home in Wellington, Florida FL.

-

Buyer A uses a conventional loan and pays PMI

-

Buyer B uses a VA loan with no PMI

Buyer B could potentially save hundreds every month.

Over five years, those savings could total thousands of dollars.

That extra money can be used toward:

-

Savings

-

Investments

-

Education expenses

-

Emergency funds

Your BAH and BAS May Help You Qualify for More

Understanding Military Income Benefits

If you are currently serving in the military or are a qualifying reservist, your:

-

Basic Allowance for Housing (BAH)

-

Basic Allowance for Subsistence (BAS)

may count toward your mortgage qualification.

This is one of the most overlooked benefits of the VA home loan program.

Many military families mistakenly calculate affordability using only their base salary.

However, because BAH and BAS are often considered stable, non-taxable income sources, they may increase your purchasing power.

Why This Matters in Florida FL

Home prices in areas like West Palm Beach and North Palm Beach may appear intimidating at first glance.

But once military allowances are factored into income calculations, many buyers discover they qualify for more than expected.

That expanded buying power may open opportunities for:

-

Larger homes

-

Better school districts

-

Waterfront communities

-

Investment opportunities

-

New construction homes

Expert Guidance Makes a Difference

A knowledgeable Mortgage Broker like Christian Penner at America’s Mortgage Solutions (AMS) can help military buyers understand how their full income profile affects loan qualification.

This guidance can significantly improve confidence during the buying process.

Why Veterans Are Choosing Florida FL

Florida Continues To Attract Military Families

Many Veterans are relocating to Florida FL for both financial and lifestyle reasons.

Some of the top benefits include:

-

No state income tax

-

Strong housing demand

-

Veteran-friendly communities

-

Excellent weather year-round

-

Beautiful beaches

-

Retirement advantages

-

Growing local economies

West Palm Beach

West Palm Beach offers:

-

Coastal living

-

Entertainment and dining

-

Boating opportunities

-

Strong job growth

-

Luxury housing options

-

Access to healthcare and Veteran resources

Veterans searching for a balance between urban convenience and beachside living often choose West Palm Beach.

North Palm Beach

North Palm Beach is known for:

-

Golf courses

-

Family-friendly neighborhoods

-

High-quality schools

-

Access to marinas and outdoor recreation

For Veterans seeking peaceful living near the coast, North Palm Beach remains highly desirable.

Wellington

Wellington, Florida FL continues to attract families because of:

-

Excellent schools

-

Spacious homes

-

Equestrian communities

-

Family-oriented neighborhoods

-

Parks and recreation

-

Safe suburban living

Military families looking for long-term stability and community often gravitate toward Wellington.

Why Working With a Local Mortgage Expert Matters

The Value of Personalized Guidance

Not every lender fully understands the complexities of the VA home loan process.

That’s why many Veterans choose to work with local professionals who specialize in helping military families.

Christian Penner, serving as a:

through America’s Mortgage Solutions (AMS), helps Veterans throughout West Palm Beach, North Palm Beach, Wellington, and surrounding Florida FL communities navigate the homebuying process.

Benefits of Working With a Local Expert

A local expert understands:

-

Neighborhood market conditions

-

School districts

-

HOA requirements

-

Flood zone considerations

-

Insurance costs

-

Veteran financing options

This local knowledge can help buyers make informed decisions and avoid unnecessary stress.

Common Questions About VA Home Loans

Can I Use a VA Loan More Than Once?

Yes. Many Veterans can reuse their VA loan benefit multiple times, depending on eligibility and entitlement restoration.

Do VA Loans Require Perfect Credit?

No. While lenders evaluate creditworthiness, VA loans are often more flexible than conventional mortgage programs.

Can I Buy a Condo With a VA Loan?

Yes, as long as the condominium community is approved for VA financing.

Can VA Loans Be Used for New Construction?

In many cases, yes.

Can I Refinance With a VA Loan?

Yes. Veterans may qualify for refinancing options, including Interest Rate Reduction Refinance Loans (IRRRL).

Can Active-Duty Military Members Apply?

Absolutely. Many active-duty service members qualify for VA financing.

Questions Veterans Are Asking

What Is the Main Benefit of a VA Home Loan?

The main benefit of a VA home loan is the ability for qualified Veterans to purchase a home with little or no down payment while avoiding PMI.

Can Veterans Buy a Home With No Money Down in Florida?

Yes. Eligible Veterans in Florida FL may qualify for zero-down VA home loans.

Do VA Loans Have Lower Monthly Payments?

In many cases, yes. The lack of PMI often lowers monthly housing costs.

Is a VA Loan Better Than a Conventional Loan?

For many Veterans, a VA loan offers advantages such as lower upfront costs, reduced monthly payments, and flexible qualification requirements.

Who Can Help Me Get a VA Loan in West Palm Beach?

Professionals like Christian Penner at America’s Mortgage Solutions (AMS) can help Veterans understand their eligibility and financing options.

The Financial Power of Homeownership for Veterans

Why Buying a Home Matters

Homeownership is about more than just having a place to live.

It can also help build:

-

Long-term equity

-

Financial security

-

Generational wealth

-

Stability for families

-

Retirement assets

For Veterans living in West Palm Beach, North Palm Beach, and Wellington, owning property in growing Florida FL communities may provide long-term financial opportunities.

Potential Long-Term Benefits

Over time, homeowners may benefit from:

-

Property appreciation

-

Stable monthly payments

-

Tax advantages

-

Increased net worth

-

Housing security during retirement

For military families transitioning into civilian life, purchasing a home can represent a major milestone.

Why Timing Matters in Today’s Housing Market

Waiting Could Cost More Later

Many Veterans delay purchasing because they believe they are not financially ready.

But rising home prices and future interest rate changes could make waiting more expensive.

Understanding your VA loan eligibility today allows you to make informed decisions about your future.

Even if you are not ready to buy immediately, speaking with a trusted professional can help you prepare strategically.

Preparation Steps Veterans Should Take

-

Review credit and finances

-

Understand VA eligibility requirements

-

Calculate affordability

-

Explore neighborhoods

-

Compare mortgage options

-

Build a long-term homeownership plan

How America’s Mortgage Solutions (AMS) Supports Veterans

Personalized Support Throughout the Process

At America’s Mortgage Solutions (AMS), Veterans receive guidance designed specifically for military homebuyers.

Whether purchasing a first home, relocating, refinancing, or upgrading to a larger property, personalized support can simplify the process.

Services Veterans May Explore

-

VA refinancing

-

Homebuyer consultations

-

Market analysis

-

Financial planning insights

By working with Christian Penner, Veterans gain access to a professional who understands both the mortgage and real estate sides of the transaction.

Bottom Line

Many Veterans in West Palm Beach, North Palm Beach, Wellington, and throughout Florida FL are far closer to homeownership than they think.

The VA home loan benefit offers powerful advantages, including:

-

Zero down payment opportunities

-

Lower closing costs

-

No PMI in most cases

-

Flexible qualification guidelines

-

Potential use of BAH and BAS income

Unfortunately, many military families never fully explore these benefits because of outdated assumptions or misinformation.

Understanding your options could open the door to buying a home much sooner than expected.

If you are a Veteran, active-duty military member, reservist, or military family considering buying a home in West Palm Beach, North Palm Beach, Wellington, or anywhere in Florida FL, speaking with an experienced professional can help you better understand your opportunities.

Christian Penner, Mortgage Broker, Mortgage Lender, Real Estate Agent, and Real Estate Advisor at America’s Mortgage Solutions (AMS) can help guide you through the process and answer questions about your eligibility, financing options, and next steps.

The path to homeownership may be closer than you think.

FAQ Section

What credit score do I need for a VA home loan?

While VA loans do not set a minimum credit score requirement, individual lenders may have their own guidelines.

Can I buy an investment property with a VA loan?

VA loans are generally intended for primary residences.

How long does VA loan approval take?

Approval timelines vary, but many VA loans close within 30 to 45 days.

Do Veterans pay mortgage insurance on VA loans?

Most VA loans do not require PMI.

Can surviving spouses qualify for VA loans?

Some surviving spouses may qualify depending on eligibility requirements.

Are VA interest rates competitive?

VA mortgage rates are often competitive compared to conventional financing.

Can I use my VA loan benefit after bankruptcy?

In some cases, yes. Eligibility depends on lender guidelines and financial recovery history.

Is Florida a good place for Veterans to buy a home?

Yes. Many Veterans choose Florida FL because of its tax advantages, climate, and Veteran-friendly communities.

Read from source: “America’s Mortgage Solutions (AMS)”

Questions, Comments or For more information you can call

Christian Penner Branch Manager at 561-316-6800 or email us at TheMortgageTeam@ChristianPenner.com

Approval Hotline: 561-316-6800

Helping You Achieve the American Dream of Home Ownership

Or You can click “Call Me” below to call Christian Penner directly using Google Voice

Legal & Compliance

Privacy Policy: https://AMS.Money/Privacy_Policy

Privacy Policy & Disclosures: https://AMS.Money/Privacy-Policy-Disclosures

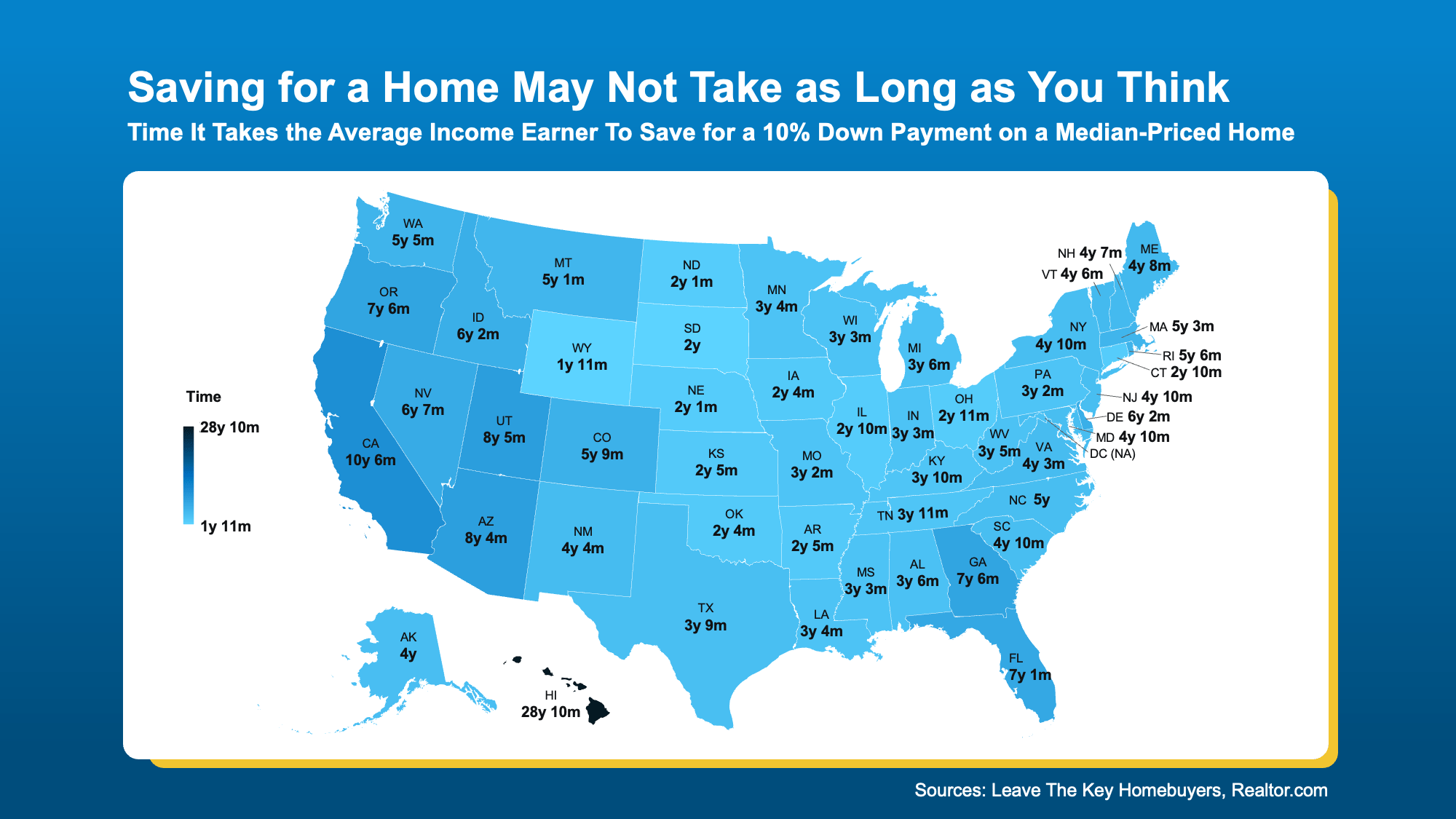

But remember, in most cases you won’t even need a down payment as large as 10%. Plus, no matter how much money you end up putting down, it won’t all have to come out of your pocket. Here’s why.

But remember, in most cases you won’t even need a down payment as large as 10%. Plus, no matter how much money you end up putting down, it won’t all have to come out of your pocket. Here’s why.

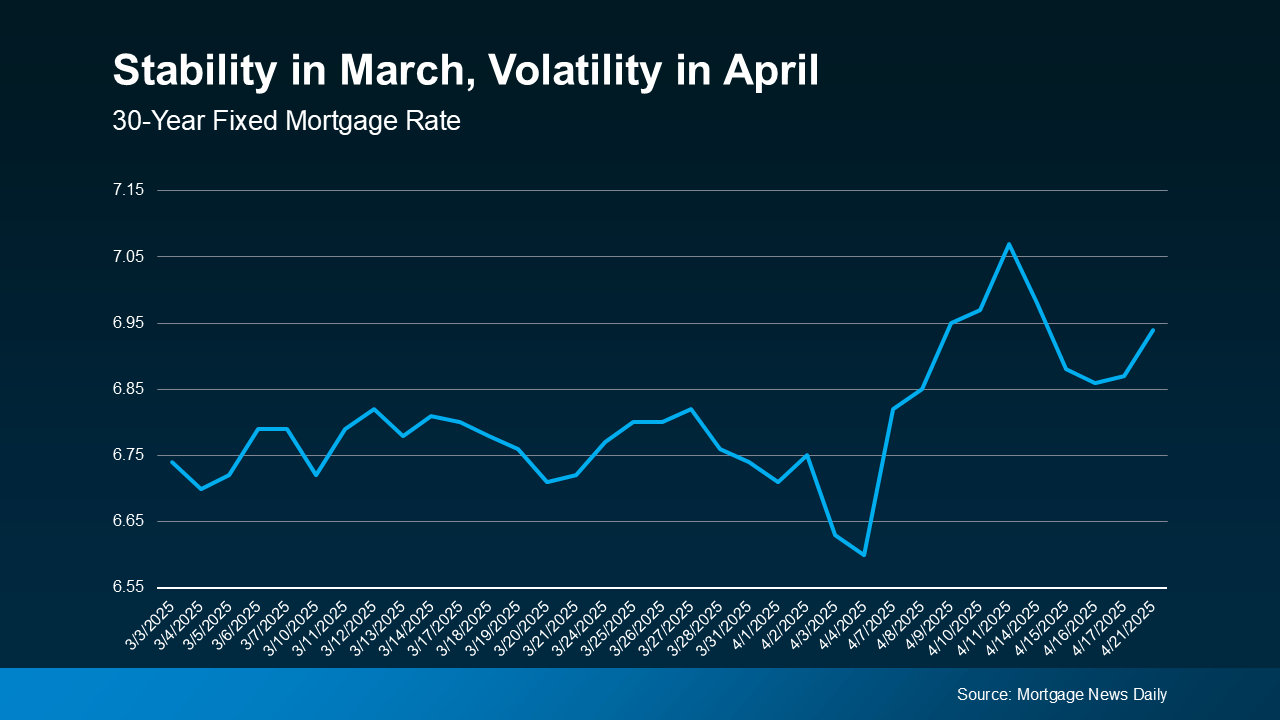

This kind of up-and-down volatility is expected when economic changes are happening.

This kind of up-and-down volatility is expected when economic changes are happening.